How Tokenized Green Bonds Could Power Curitiba’s Rooftop-Solar Plan

In 2023 the Brazilian city of Curitiba turned an old landfill into a “Solar Pyramid” – a pioneering solar power plant with about 8,600 solar panels on its slopes. This pilot project feeds clean energy into the grid and saves the city roughly US…

In 2023 the Brazilian city of Curitiba turned an old landfill into a “Solar Pyramid” – a pioneering solar power plant with about 8,600 solar panels on its slopes. This pilot project feeds clean energy into the grid and saves the city roughly US $500,000 each year on electricity costs. The project was made possible with support from the C40 Cities Finance Facility (CFF), which recognises that access to finance is one of the biggest barriers cities face in launching climate projects. By helping Curitiba prepare the Solar Pyramid deal, the CFF showed how technical assistance and innovative funding can unlock real climate action. Now, City Hall wants to go much further – installing 15 MW of new rooftop solar panels on 2,600 public buildings such as schools, markets and bus stations. The price tag is around €90 million, and the solar technology is ready. The only question is: where will the city get that much money?

Curitiba can no longer rely on grants alone, and local banks still charge high interest rates on big loans. In other words, the key problem is financing, not engineering. “We asked for this international financing because we need capital to build phase II of the Solar Pyramid and 27 more solar units,” explained Rafael Greca, the Mayor of Curitiba. Mayor Greca sought help from abroad – for example, a low-interest loan from the German bank KfW – to scale up the city’s successful solar program. His words highlight the reality that even a well-run city often lacks affordable capital for green infrastructure. This is where an emerging idea, tokenized green bonds, could make a big difference.

Traditional Financing Is Not Enough

Until now, Curitiba has leaned on traditional financing tools like soft loans from KfW (Germany’s development bank), credit lines from Brazil’s national development bank BNDES, and the city’s own municipal bonds. Each of these comes with limitations. Negotiating big loans can take months of talks and paperwork. Foreign loans introduce currency exchange risks. And the city has legal debt limits that cap how much it can borrow in total.

The C40 Cities Finance Facility helped connect Curitiba with funders for the pilot project and noted that its role is to help cities access finance to deliver climate projects – yet CFF itself cannot fund every megawatt a city wants to install. Even BNDES, the national bank, has only issued green bonds a handful of times since launching its Green Bond Framework, so it can’t bankroll rooftop solar across all Brazilian cities on its own. The result is a financing gap: many public building rooftops are sunny and ready for solar panels, but the upfront investment is waiting in line, while the city continues to pay rising electricity bills.

Many ordinary citizens or climate-conscious investors would gladly help fund solar projects if the “entry ticket” were small and the investment easy to trade. In a traditional bond or infrastructure fund, the minimum investment might be tens of thousands of dollars, which shuts out most households. But what if Curitiba could tokenise its solar project into bite-sized pieces that anyone can buy? These tokenized green bonds could fill the gap by tapping a much broader pool of investors – from local families to eco-funds around the world – and by turning the city’s energy savings into an income stream for those investors.

What Is a Tokenized Green Bond?

A tokenized bond is essentially a digital version of a standard bond recorded on a blockchain network. In practical terms, the city (or a special project company it sets up) would issue a bond as usual, but instead of investors buying one big bond certificate, the bond is broken into many small digital tokens. Each token might be worth say $50 or $100, representing a tiny slice of the total bond value. Investors can buy as many tokens as they want, even just one, which makes the bond far more accessible than a traditional bond that might require a $100,000 minimum purchase.

Each token comes with the same rights as a normal bond: the owner is entitled to periodic interest payments (the coupon) and the return of principal at maturity. However, the use of blockchain and smart contracts automates much of this process. Smart contracts (basically self-executing code on the blockchain) can be programmed to send interest payments straight to investors’ digital wallets on schedule, without banks or middlemen doing manual processing. Transactions are recorded on a public ledger, so anyone can verify the transactions and ownership at any time. This transparency means audits and reporting can be faster and cheaper, and it helps build trust that the funds are used as promised (important for a green bond intended to deliver environmental benefits).

Another feature is that tokenized bonds can potentially be linked with real-world data. For a solar project, this means the bond’s performance could be tied to the project’s energy production. For example, the city could choose to make the coupon (interest rate) partly dependent on actual solar output, using data from solar inverters that report production to the blockchain in real time. In this way, investors get paid based on real kilowatt-hours generated, aligning their returns with the project’s success. (Even if the bond’s coupon is fixed, live production data can still be published on-chain to prove the solar panels are working.) This kind of real-time data integration is a new innovation – it offers proof of green impact in real time, not just in an annual report. Overall, a tokenized green bond works like a normal bond in terms of finance, but it is chopped into tiny, tradeable units and powered by digital technology for efficiency.

How Tokenisation Could Fund Curitiba’s Solar Expansion

Imagine how this could work for Curitiba’s ambitious rooftop solar plan. First, the city could set up a Special Purpose Vehicle (SPV) – essentially a dedicated project company – to own and manage the new solar installations. This SPV would likely be co-owned by the city and perhaps the state utility (as was done in the first Solar Pyramid project, where the city held 51% and the utility company Copel 49%. The SPV would sign a contract to supply solar power to city buildings for a long period (for example, 10 years). This contract guarantees that the solar electricity will have a buyer (the city itself), creating a steady revenue stream from the energy cost savings.

Next, the SPV would issue the tokenized green bond to raise the upfront funds (around €90 million). For instance, it could mint 900,000 digital tokens at $100 each, using a secure blockchain platform. Investors who purchase these tokens are effectively lending money to the project, and in return the SPV promises to pay them, say, a 6% annual interest. The beauty of using tokens is that local residents could buy one or two tokens if they want, while larger investors could buy thousands – the bond financing scales to whoever is interested. The interest (coupon) could be paid in a stable digital currency (for example, a USD-pegged stablecoin) to avoid exposing investors to Brazil’s inflation or currency fluctuations. Every month, as the solar panels generate power, the city saves money by not buying as much electricity from the grid. Those savings (in Brazilian reais) can be converted to the chosen stablecoin and automatically distributed to token holders as interest. The records of energy production and payments would all be logged on the blockchain for transparency.

To make the tokenized bond appealing and fully compliant, Curitiba would register it under Brazilian financial regulations – for example, as a Certificado de Recebíveis Verdes (Green Receivables Certificate), which is a format for sustainable investment securities. The tokens could then be listed on a regulated digital exchange or trading platform, so that investors can freely buy or sell them. This means the bond is not locked away in a drawer – it can be traded 24/7, giving investors liquidity if they need to exit early.

Because this concept is new, the city might also seek credit enhancement to reduce risk for investors. One idea is to bring in a development bank as a guarantor for part of the bond. For instance, the Asian Infrastructure Investment Bank (AIIB) recently partnered with Brazil’s cooperative bank Sicredi to support US $100 million for small-scale solar energy loans across the country. Curitiba could invite an institution like AIIB or the World Bank to provide a “first-loss” guarantee – meaning if the project had any losses or shortfalls, that institution would cover the first portion. This kind of guarantee can give the bond an investment-grade profile.

In practical terms, credit rating agencies could then rate the bond BBB or higher, which would lower the interest rate the city has to pay because the investment is seen as safer. With such backing in place, the city’s finance team could confidently say they are locking in a cost of capital (interest rate) that is much lower than typical local bank loans. In effect, Curitiba would secure cheap, stable financing and lock in cheaper power prices for its facilities, freeing up future city budget funds that would otherwise go into paying energy bills. The tokenized bond turns the city’s sunny rooftops into an asset that attracts global capital.

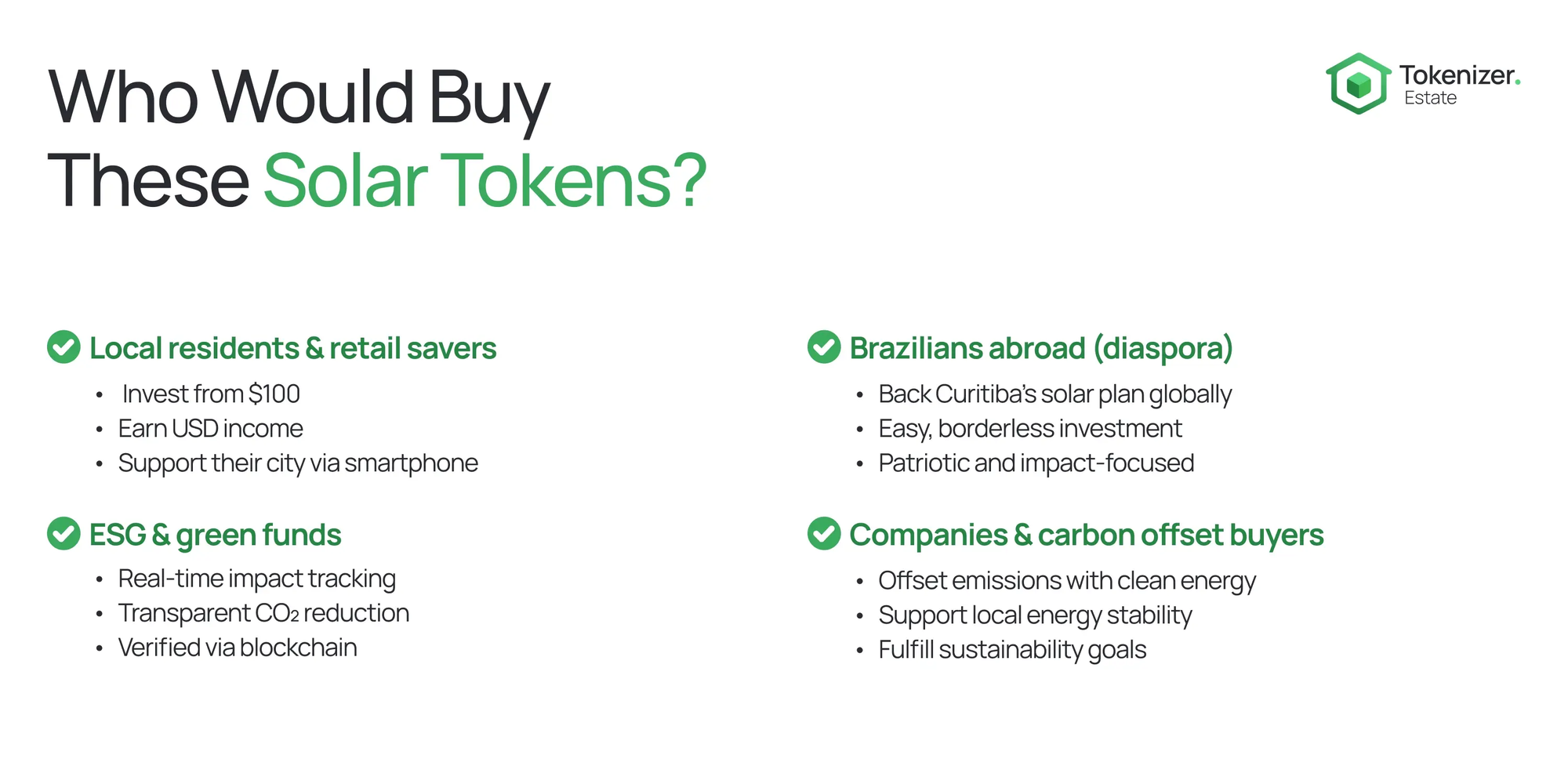

Who Would Buy These Solar Tokens?

One of the strengths of tokenisation is that it opens the door to a wide range of investors that traditional city bonds might not reach. Here are some likely buyers:

- Local residents and retail savers: Curitiba’s own citizens might want to invest in the solar program if they can afford the entry amount. With tokenized bonds, a family could invest even $100 or $500 and directly earn a steady income in USD from the city’s solar savings. It’s a way for residents to put their savings into improving their city and get a better return than a savings account. Because it’s a digital token, the process could be as simple as using a smartphone app – much more accessible than buying a conventional bond from a broker.

- Brazilians abroad (the diaspora): There are many people from Paraná and Brazil living overseas who still care about their hometown. These tokens would give them a chance to support Curitiba’s green projects from anywhere in the world, without complicated bank transfers. If the tokens are listed on a global platform, a Brazilian engineer working in Europe or the US could easily buy some to back the solar plan. This taps into patriotic and impact-focused investment that currently has no easy channel.

- ESG and green funds: Investment funds that specialize in Environment, Social, and Governance (ESG) criteria would be very interested in a transparent, impact-driven bond like this. A tokenized bond can offer real-time tracking of the environmental impact. In fact, blockchain transparency makes it easier to track and report carbon emission reductions from the project, as UN climate experts note. An ESG fund manager could see live data on how much solar energy is produced and how many tons of CO₂ are avoided, giving them confidence that the bond’s green claims are genuine. This verifiable impact could attract climate-focused investors who might not usually invest in a mid-sized Brazilian city, but would do so because the project’s outcomes are clear and accountable.

- Companies and carbon offset buyers: Businesses that need to offset their electricity use or carbon footprint might buy these tokens as a form of offset. For example, a company could purchase a portion of the tokens and retire the interest they earn in exchange for claiming the underlying clean energy or carbon savings. Alternatively, large power users in Curitiba (like malls or factories) might invest to support the city’s grid with more renewable energy, which in turn improves local energy stability. Some companies also have sustainability mandates to invest in green projects, and a tokenized bond is an easy, trackable way to do that.

Importantly, the tokens would be tradeable at any time on the approved exchange. If a local investor suddenly needs cash for an emergency, they could sell their tokens to someone else – there will always be a market price. This 24/7 liquidity is a huge improvement over traditional bonds that might only trade infrequently or require waiting until maturity. With more participants and continuous trading, the market can self-regulate the price of the tokens and attract even more buyers. In addition, a broader investor base increases scrutiny and reduces the chance of any wrongdoing, because thousands of eyes are watching the project’s performance data on the blockchain. All of these factors make the tokenized bond a very flexible and inclusive financing tool compared to the status quo.

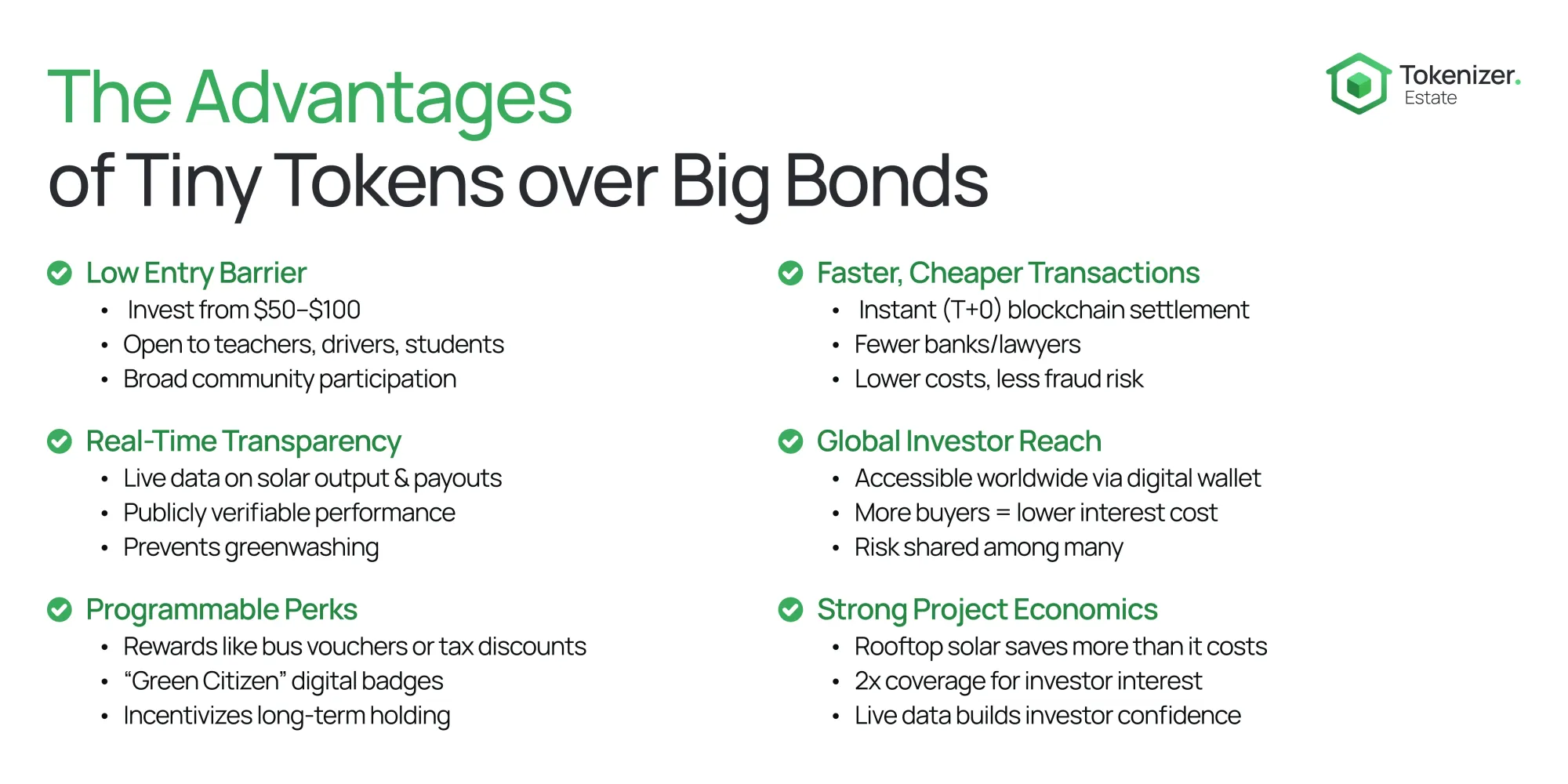

The Advantages of Tiny Tokens over Big Bonds

Why go through the trouble of tokenisation instead of a normal city bond or bank loan? In summary, tokenising Curitiba’s solar bonds could bring several key advantages:

- Lower entry barrier: By breaking the bond into micro units, the city allows anyone to invest with a small amount. Traditional bonds often require large minimum investments (thousands or millions of dollars). In contrast, a token could be priced at $50 or $100, democratising the investment and enabling broad community participation. This means teachers, taxi drivers or students in Curitiba could all own a piece of the solar parks, aligning the public with the city’s climate goals.

- Faster, cheaper transactions: Token trades and transfers settle almost instantly on the blockchain, whereas normal bond trades might take T+2 days to clear. This speed (T+0 settlement) cuts down on administrative delays and reduces middleman fees. For the city, issuing a bond on-chain could also be faster and involve fewer intermediaries (like fewer banks and lawyers), thus reducing issuance costs. One industry analysis noted that tokenized bonds eliminate much of the paperwork and can automate compliance, which lowers the risk of fraud or error in managing the bond.

- Real-time transparency and trust: With a tokenized solar bond, any interested party can monitor the project’s performance in real time. The blockchain ledger might show, for example, that X megawatt-hours were produced this week and interest payouts of Y dollars were made this month, all verifiable by the public. This level of transparency builds trust that the project is doing what it promised. It also helps ensure that only authentic green projects receive funding, because the data (like solar output or CO₂ reduction) is out in the open for due diligence. An investor in London or Tokyo can verify Curitiba’s solar output online, which is far more convincing than a brochure or single annual report. This real-time proof of performance makes the bond more credible. “Anyone can verify the energy output on the blockchain,” as one R&D report on green finance noted, preventing any chance of greenwashing.

- Global reach of investors: Normally, a bond issued by a city in Brazil might only be bought by local banks or a few big investors due to market and currency barriers. Tokenisation, however, means a buyer in Asia, Europe or Africa can participate easily with a compatible digital wallet. The bond no longer stays in a silo; it becomes a globally accessible investment. This wider demand can potentially lower the interest rate required (because more buyers competing drives the price up and yield down), benefiting the city. It also spreads the risk among many holders instead of a few large creditors, which is healthier for the city’s finances.

- Programmable perks and community benefits: Because tokens are digital, the city can program additional features. For example, Curitiba could decide that anyone holding, say, 10 or more tokens for a full year gets a bonus voucher for free bus tickets or a property tax discount. Or the city could gamify climate action by giving token holders a special “green citizen” badge in a municipal app, recognizing their contribution. These kinds of perks can incentivize local uptake and reward people for keeping their investment long-term. While not necessary for the bond to function, such creative options are only possible because of the flexibility of digital tokens.

Beyond these advantages, it’s worth noting that the solar projects themselves are financially sound on a small scale, which tokenisation can showcase. For instance, consider a typical public building roof: a 100 kW solar array might cost about US $85,000 to install. It can save roughly $12,000 per year on electricity bills for that building. Even after paying for maintenance (say ~$1,000/year), the net saving is about $11,000. If the bond investors need to be paid 6% interest on that $85,000 (around $5,100 per year), the solar panels generate more than twice the cash needed to cover the interest – a comfortable margin of safety. Even if a year is less sunny than expected and output drops 10%, there would still be more than enough savings to pay investors. This kind of robust cash flow is why financiers are increasingly confident in small-scale solar. “Small solar is now bankable when revenue data is live and open to all,” says Jin-Hong Kim, Director of Energy at AIIB, underscoring that real-time data transparency makes even modest solar projects credible to backers. In other words, when everyone can see the sunlight turning into money, they are more willing to invest in these projects.

A Model Other Cities Can Follow

Curitiba’s experience highlights that the obstacle to more rooftop solar is not a lack of sunshine or technology – it’s access to capital. By embracing tokenized green bonds, cities can tap into thousands of small investors worldwide who are eager to fund clean energy. This approach essentially crowdsources climate finance in a regulated, efficient way. The concept may be new, but it is already catching attention. For example, Curitiba’s success with the Solar Pyramid inspired other cities: Rio de Janeiro is working on a similar solar project called the “Carioca Solarium,” using a public-private partnership model developed with CFF support. In that case, a disused landfill in Rio’s Santa Cruz area will be turned into a solar farm to power thousands of homes. While Rio’s project isn’t tokenized, it shows the strong interest in innovative finance for urban solar. Elsewhere, city leaders in places from Mumbai to Cape Town are exploring ways to scale up solar on bus depots and public lands, often learning from each other’s examples.

We can easily imagine that if Curitiba launches a successful tokenized solar bond, other cities – Bogotá, Dakar, Jakarta, you name it – could quickly replicate the model. Good ideas in city governance tend to travel fast, especially when they solve a common problem. Every city has schools, libraries or hospitals that could have solar panels; many of those cities also have residents or alumni around the world who would invest in a hometown project if given the chance. Tokenisation provides the platform for that connection. It turns climate action into a participatory investment. When data on outputs and impacts is transparent, as with blockchain, it builds trust across borders. Thus, Curitiba could not only fund its own green transition but also pioneer a template for municipal green financing that others follow. In essence, a successful issuance in Curitiba would be a proof of concept showing that raising millions through tokenized micro-investments is not only possible but efficient.

Conclusion: Small Investments, Big Impact

Rooftop solar has the power to light up schools, clinics, and public transit with clean energy. The thing that often stops cities from covering every roof with panels is not a lack of sunlight – it’s the lack of upfront financing. Tokenising a green bond is a clever way to cut that big financing into tiny pieces and invite the whole world to help, all while providing full transparency on where the money goes and what the project achieves. This means a city like Curitiba can raise the cash it needs in weeks, not years, and do so on favorable terms. As Mayor Greca is fond of reminding people, “We move a little bit at a time, and in the end we achieve what once looked impossible,” invoking the wisdom of St. Francis that great things are done by **many small efforts added together. Tokenized green bonds offer that next “little step” – enabling thousands of modest contributions to build a solar future. With such innovation, any sunny city can take a confident step today toward a cleaner and more self-sufficient energy future, one token at a time.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo