Investor’s Checklist: What You Need to Know Before Purchasing Real Estate Tokens

Thinking of clicking “Buy tokens” on a property deal? Use this calm, step-by-step checklist to understand what you’re really buying, how payouts work, where liquidity comes from, what fees hide in the fine print, and which red flags should stop you.

Last week, you might have seen it too: a nice photo of a building, a short video, and a button that says “Buy tokens.” It looks simple. Almost like buying a stock, but the story is about real estate. A friend messages you, “This is the future. You can own part of a property with $100.”

You feel curious. You also feel a little unsure. Real estate is usually slow and heavy. Papers, lawyers, bank transfers, long waiting. So how can it be “one click”?

This article is a calm walk from curiosity to a clear decision. We will keep it simple and practical. You will learn what real estate tokens really are, what good projects do well, and what you should check before you buy. Tokenization can bring real value—especially global investor reach and easier access—but only if the deal is built the right way.

Real estate tokens in simple words

Real estate tokenization means you take a real-world property (or the cash flow from it) and you represent investor rights with digital tokens on a blockchain. A token is not the building itself. A token is a digital proof of some right.

That “right” can look different from project to project. In many cases, the token gives you a claim on income (like rent profit) or a claim on value (like part of sale profit). Sometimes it is linked to shares in a company that owns the property. Sometimes it is linked to a contract that promises payments.

This is why words matter. Before you buy, you must understand what the token represents in legal terms, not only in marketing terms. If you want a simple view of how rules often work across different countries, you can read guide.

One more simple idea: tokenization is a bridge between two worlds. One world is the “off-chain” world: land registry, ownership papers, rental contracts, taxes, courts. The other world is the “on-chain” world: wallets, smart contracts, token transfers, and transparent records. A strong project connects these two worlds in a clear way. A weak project leaves a gap—and that gap is where investors get hurt.

Why tokenization can be good (and what it is not)

Many investors like tokenized real estate for a few positive reasons.

First, it can open the door to more people. Real estate is often expensive. Tokenization can split value into smaller pieces, so more investors can join. This is not only about “small tickets.” It is also about global reach. A project can speak to investors in different countries, and it can handle many small holders without a big, slow back office.

Second, tokenization can improve access and speed. Traditional real estate deals can take weeks. Token transfers can be faster. It may also be easier to track ownership changes and investor records.

Third, it can improve transparency. On-chain transactions can be easier to check. Investors can sometimes see token supply, transfers, and smart-contract rules. That does not replace legal documents, but it can reduce confusion and make reporting clearer.

The World Economic Forum describes tokenization as a way to enhance transparency, efficiency, and accessibility, with features like fractional ownership and programmability. If you want a high-level view from a trusted global institution, you can download report.

Now the honest part: tokenization is not magic. It does not remove risk. It does not guarantee liquidity. It does not replace good property management. And it does not make regulation disappear. If someone tells you “blockchain makes it safe,” you should slow down. Blockchain can record rules, but it cannot fix bad rules.

So the right mindset is balanced. Respect the positives—global investor outreach, lower entry points, faster settlement, clearer records—but treat each project like a real investment that needs real checking.

What makes a token “real estate” in practice

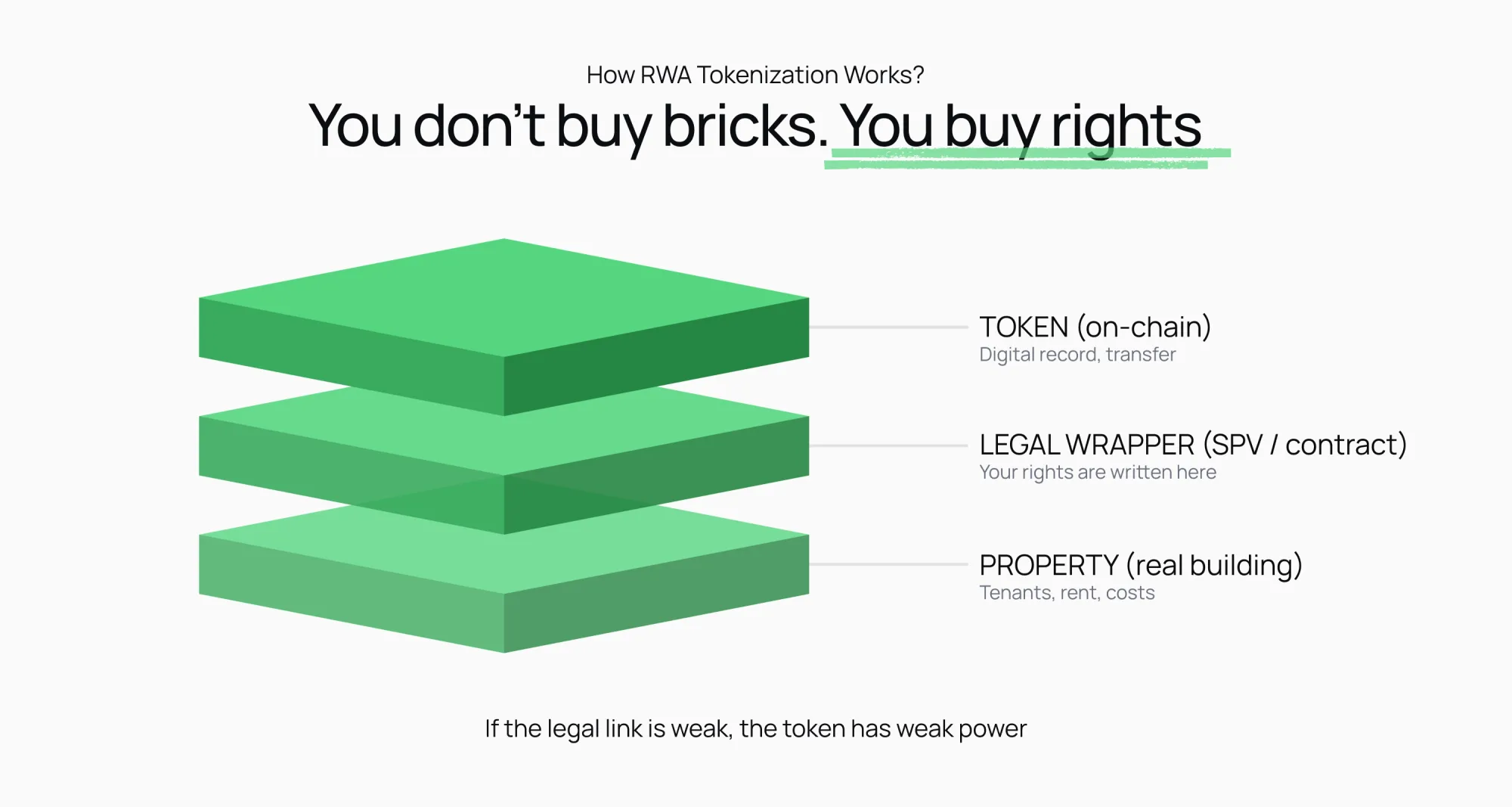

When you buy tokenized real estate, you are not buying bricks. You are buying a deal structure. That structure has three main parts.

One part is the property story. Where is the building? Who owns it today? Is it already rented? What is the plan: rent income, renovation, sale, or a mix?

The second part is the legal wrapper. Many projects use a company (often called an SPV—special purpose vehicle) that owns the property. Investors may hold tokens that link to shares, or tokens that link to a profit-sharing contract. The details matter because your rights in a dispute depend on them.

The third part is the tech layer. This includes the token standard, the blockchain used, and the smart contract logic (for example, how distributions are done, or how transfers are limited if rules require it).

If you want a simple, step-by-step view of how real estate tokenization is usually built — from valuation and legal setup to token sale and secondary trading — you can learn process.

This “three-part” view helps because it keeps you from focusing only on the shiny part (the token) and forgetting the heavy parts (the property and the law). A strong investment checks all three.

The checklist before you buy

The best checklist feels like a story. You start with the basic question: “What am I buying?” Then you move to: “How do I get paid?” Then: “Can I exit?” Then: “What can go wrong?”

Below are the key checks, explained in simple language. It is not legal or financial advice, but it is a practical way to think.

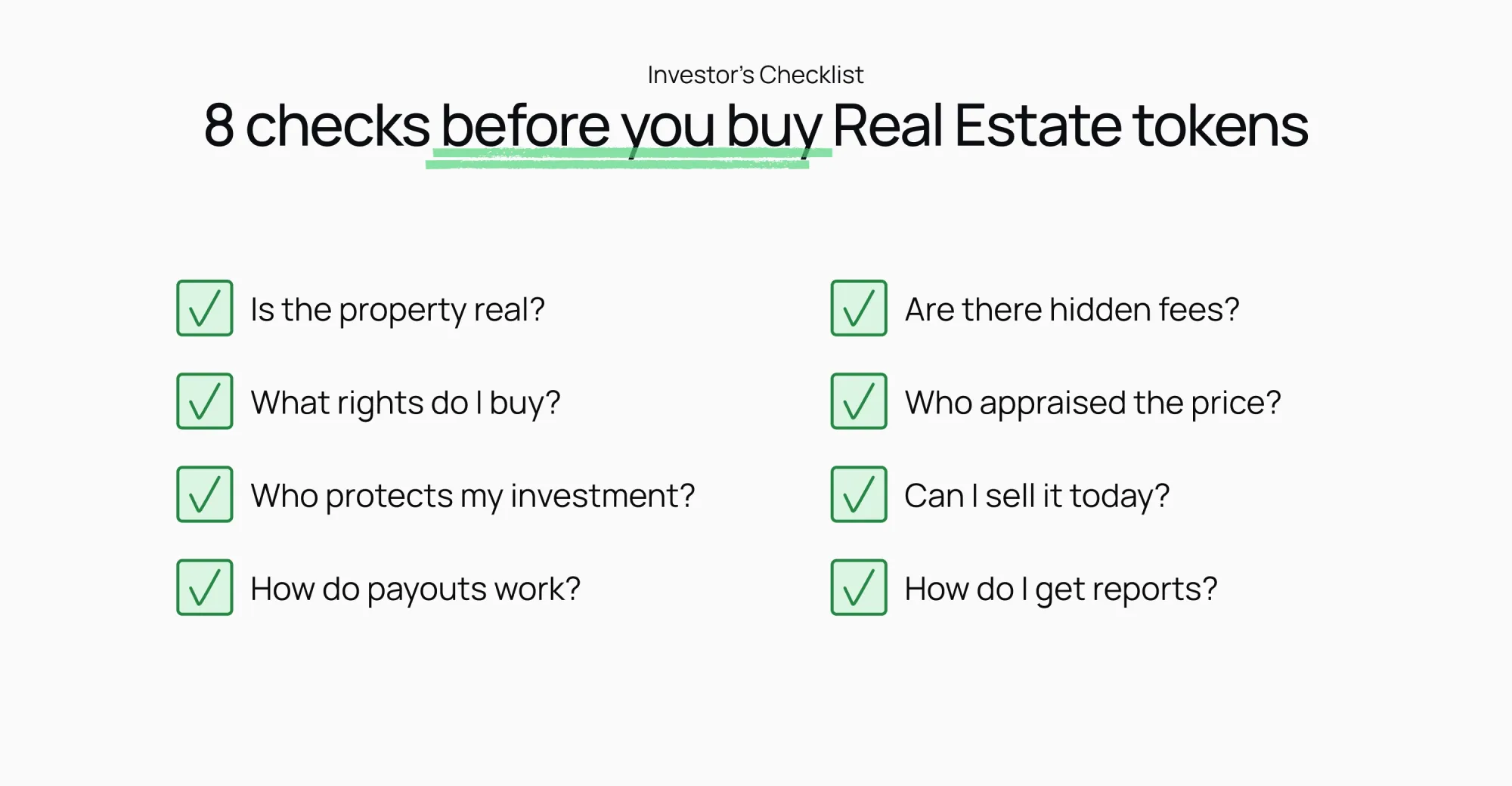

Start with the clearest point: the property must exist and the project must be able to prove it.

- Ask for the property address and basic details. Ask who owns it now. Ask if there are debts, liens, or other claims on it. In many countries, these checks are normal in real estate deals, so a serious project should not act offended when you ask.

- Next, ask what legal right the token gives you. Does it represent shares in a company? Does it represent a claim on profit? Does it represent a loan claim? The wording must be clear in official documents, not only in a website FAQ.

- Then, look at investor protections. What happens if the manager fails to pay, or if the platform stops working? Is there a clear process for disputes? Is there an independent party involved (like an administrator, trustee, or regulated service provider), or is everything controlled by one company?

Also check compliance basics. Many real estate token projects must follow securities rules and must do KYC/AML. If a project asks for no identity checks at all but still promises investment returns from real estate, that can be a warning sign in many jurisdictions.

If you want a sense of how regulation often treats property tokens, and why many are handled like securities, you can look again at that country overview and read guide as a reference point.

A simple rule: if you cannot explain your legal right in one or two clear sentences, do not invest yet. - Ask how returns are created. Is it rent income? Is it profit after a future sale? Is it interest from a loan to a developer? Each model has different risks. Rent income depends on tenants and costs. Sale profit depends on the market and timing. Loan interest depends on the borrower’s ability to pay.

- Then look at costs. Real estate has many costs: repairs, insurance, taxes, empty months, management fees. Token projects also have extra costs: platform fees, custody fees, legal costs, sometimes blockchain transaction costs. A serious project will show a simple breakdown, not hide behind a single “expected yield” number.

- Also check valuation logic. How was the price of the property decided? Is there an independent valuation, or only an internal estimate? Real estate prices can be subjective. You do not need perfect certainty, but you do need a reasonable method.

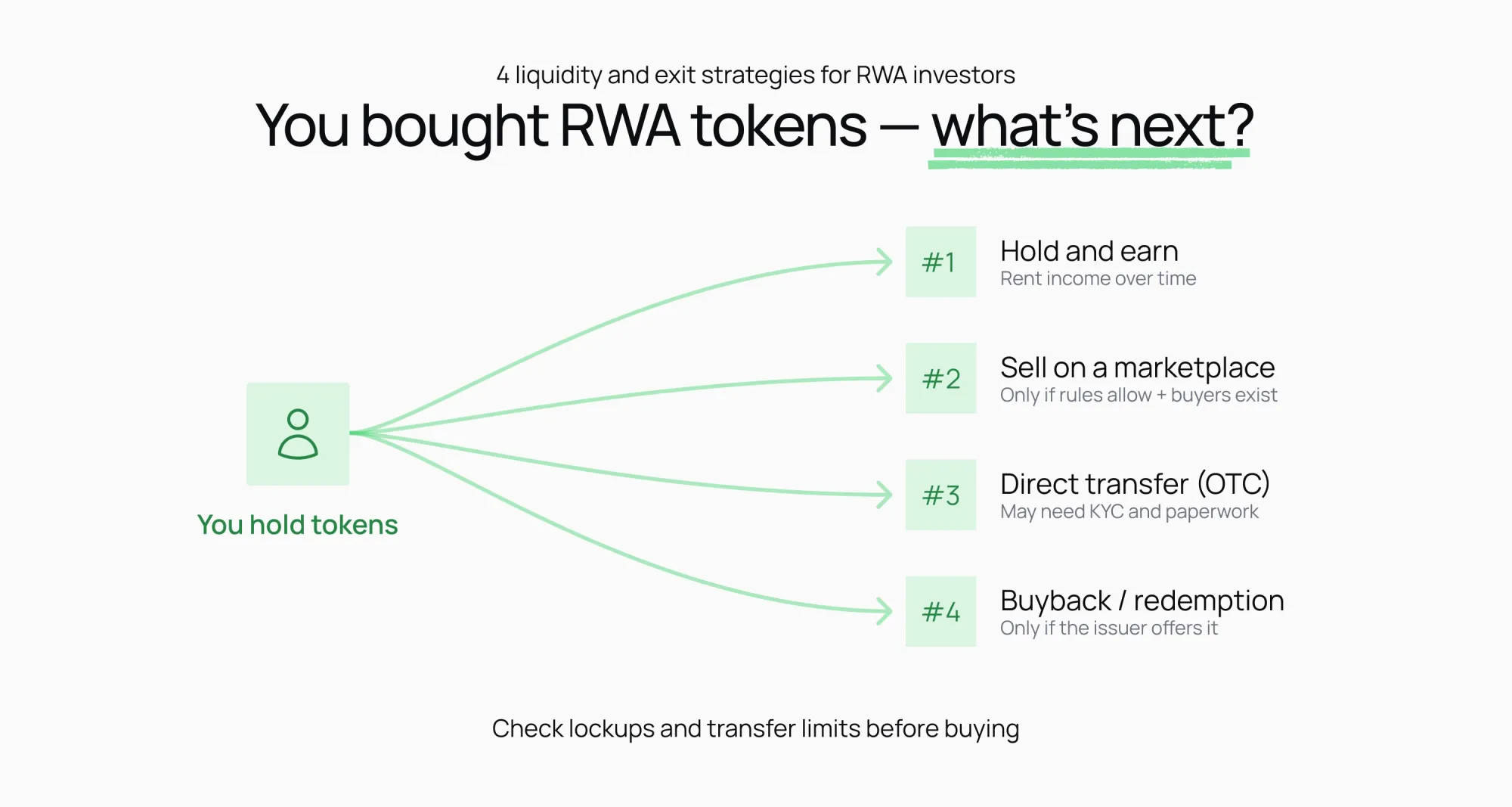

- Now check liquidity. Many people think tokens are “liquid” because crypto trades 24/7. But tokenized real estate may not trade easily. Sometimes there is a lock-up period. Sometimes transfers are restricted by law. Sometimes there is no active secondary market.

So ask directly: Where can I sell later? Is there a secondary market? Are there buyers? Is there a market maker? If the answer is “maybe later,” treat it as illiquid. - A final check in this part is reporting. How often will you get updates? Monthly rent reports? Quarterly statements? Will you see proofs of rent payments and expenses? Clear reporting is not just nice—it reduces the risk of ugly surprises.

Risks that still matter, and how good projects reduce them

Even with a good checklist, tokenized real estate has real risks. The goal is not to fear them. The goal is to see them early.

One risk is regulatory change. Rules for tokenized assets are still developing in many places. That can affect who can buy, how tokens can be traded, and what disclosures are needed. This is why projects that work with compliance and clear documents often age better than projects that “move fast and break things.”

A second risk is operational risk. Real estate returns depend on human work: finding tenants, fixing problems, paying bills on time, handling legal issues. Tokenization does not replace that. So you need to understand who manages the building and what experience they have.

A third risk is technology and smart-contract risk. Smart contracts can have bugs. Wallet security matters. Admin keys matter. Good projects do audits, explain custody choices, and have clear processes for emergencies.

A fourth risk is liquidity risk. If you might need your money back quickly, tokenized real estate can disappoint you. It is often closer to a private real estate deal than to a public stock.

International regulators also discuss these topics. IOSCO, a global body for securities regulators, has written about tokenization and the kinds of risks and challenges markets should consider. If you want a serious, policy-level view, you can review paper.

Now, the positive side again: the same tools that bring new risks can also reduce old problems. Tokenization can standardize investor records, automate parts of distribution, and make ownership tracking clearer. It can also help real estate issuers reach investors outside their local market, which can improve funding options and sometimes reduce reliance on one local buyer group. This “global investor outreach” is one of the most important benefits when it is done in a compliant way.

You can also see how tokenization is becoming a global topic, not a small niche. For a short global view of regional moves and what the market expects, you can follow highlights.

Conclusion

Let’s return to your original moment: you are looking at that “Buy tokens” button. You do not want to miss an opportunity. You also do not want to buy a promise that has no strong base.

A good decision path is simple.

First, write down what you want. Do you want stable income, long-term growth, or a mix? How long can you hold? How much liquidity do you need? Tokenized real estate can be great for patient capital. It is often not great for quick flips.

Next, confirm what you are actually buying. Say it out loud in one sentence: “I am buying tokens that give me X right, backed by Y legal structure, connected to Z property.” If you cannot say it, keep learning and asking.

Then, follow the checklist: property proof, legal rights, compliance, costs, income model, reporting, exit path, and risk controls. Do not rush. Real estate rewards calm thinking.

Also consider a small test. If the platform and legal process allow it, some investors start with a small amount. They watch one or two reporting cycles. They see how communication feels. They learn how transfers and custody work. This is not about fear. It is about learning with limited risk.

Finally, remember why tokenization is exciting in the first place. It can make real estate more open. It can help projects reach investors around the world. It can make ownership records easier to manage. It can bring more choice for investors who are priced out of traditional property markets. And it can do all of this without changing the basic truth: a real asset is still managed in the real world, under real laws.

If you keep that truth in mind, tokenization becomes less confusing. It becomes what it should be: a modern tool for an old asset class—useful, promising, and worth respect when done carefully.