KYC/AML for tokenized securities: what issuers must know in 2026

When you tokenize a building, the bank is no longer in the middle. You become responsible for KYC/AML on every investor. In 2026, regulators are handing out nine-figure fines. This guide covers four jurisdictions, on-chain compliance.

In late 2025, the US Department of Justice fined OKX over $500 million. The reason: weak KYC checks and billions in suspicious transactions that nobody flagged. A few weeks later, the Central Bank of Ireland fined Coinbase Europe €21.5 million for failing to monitor transactions properly. And FinCEN hit Paxful with a $3.5 million penalty for letting $500 million in illicit activity flow through its platform.

These are crypto exchanges. But the lesson applies directly to anyone issuing tokenized securities, including tokenized real estate. If you tokenize a building and sell tokens to 200 investors across 14 countries, you are issuing securities. You are a financial services provider. And you are subject to KYC/AML rules in every jurisdiction where your investors live.

Most asset owners who consider tokenization think about legal structure, smart contracts, and investor onboarding. KYC/AML compliance is often treated as a checkbox. It is not. In 2026, it is the layer that determines whether institutional money can enter your deal, whether your tokens can trade on secondary markets, and whether you stay on the right side of regulators who are handing out nine-figure fines.

This article explains what KYC and AML mean for tokenized securities issuers, what the rules are in the four jurisdictions that matter most, how on-chain compliance actually works, and what you need to build into your deal from day one.

What KYC and AML actually mean for token issuers

KYC stands for Know Your Customer. It means verifying the identity of every person who buys your token. Name, address, date of birth, government-issued ID, proof of residence. For accredited investors, it also means verifying their income or net worth.

AML stands for Anti-Money Laundering. It means monitoring transactions for suspicious patterns: unusually large purchases, rapid buying and selling, funds coming from sanctioned countries or known illicit addresses. If something looks wrong, you must file a Suspicious Activity Report (SAR) with the relevant authority.

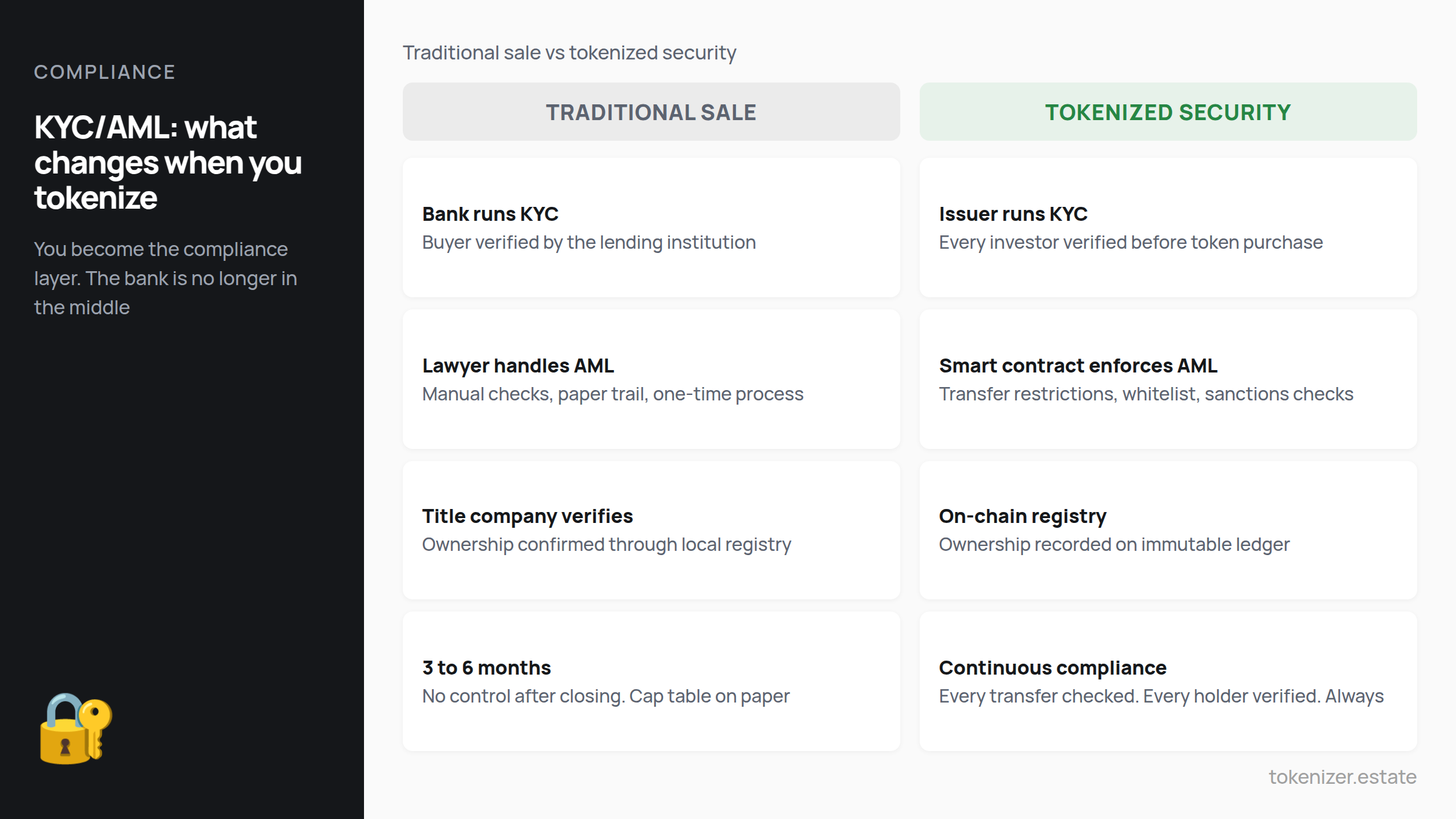

For traditional real estate, these rules are handled by banks, lawyers, and title companies. When you sell a building, the bank runs KYC on the buyer. When you tokenize a building, you become the one responsible for running KYC on every investor. The bank is no longer in the middle.

This is the critical difference. Tokenization removes intermediaries. That is one of its biggest advantages. But it also means the issuer picks up compliance responsibilities that banks used to handle. If you skip this step or do it poorly, the consequences are real: fines, criminal liability, and the inability to operate in regulated markets.

The four jurisdictions that matter in 2026

KYC/AML rules are not global. They vary by country. But four jurisdictions cover the vast majority of tokenized real estate deals, and each has made significant moves in the last 18 months.

United States. The GENIUS Act, signed in July 2025, created the first federal framework for stablecoins and brought payment rails for tokenized assets under clear regulation. FinCEN requires all financial institutions, including digital asset service providers, to maintain AML programs with customer identification, transaction monitoring, and suspicious activity reporting. From 2026, registered investment advisers are also required to implement AML programs for the first time. The SEC continues to treat most tokenized real estate offerings as securities under Reg D (accredited investors) or Reg S (non-US investors). Every investor must be verified before they can buy a token.

European Union. MiCA (Markets in Crypto-Assets Regulation) is fully live across all 27 member states. Crypto-asset service providers must obtain licenses, implement KYC/AML controls, and comply with the FATF Travel Rule. The new EU Anti-Money Laundering Authority (AMLA) begins direct supervision in 2026, creating a "single rulebook" for the entire bloc. For tokenized securities specifically, MiFID II still applies. The combination of MiCA + MiFID II + AMLA makes Europe the most heavily regulated market for tokenized assets in the world.

UAE. VARA (Virtual Assets Regulatory Authority) in Dubai licenses and supervises virtual asset service providers. The Abu Dhabi Global Market's FSRA adopted the FATF Travel Rule in 2023 and issued updated guidance in 2025 requiring firms to avoid anonymous counterparties. The UAE Central Bank leads AML enforcement nationally. For tokenized real estate issuers operating out of Dubai or ADGM, full KYC/AML compliance is mandatory from day one.

Singapore. The Monetary Authority of Singapore (MAS) enforces AML Notice 626, which requires strong KYC, transaction monitoring, and suspicious activity reporting. Singapore has been running Project Guardian, a multi-year initiative testing tokenized assets with institutional participants. The regulatory framework is clear, the enforcement is real, and Singapore-based family offices are increasingly active in tokenized real estate.

The bottom line: there is no jurisdiction where you can skip KYC/AML. The rules exist everywhere. The question is which set of rules applies to your deal.

How on-chain KYC actually works

This is where tokenization turns from a compliance burden into a compliance advantage. In traditional finance, KYC is a one-time paper check. You verify the investor at the start, and then you have no control over what happens after. Shares can be resold informally. Cap tables get messy. Compliance breaks down over time.

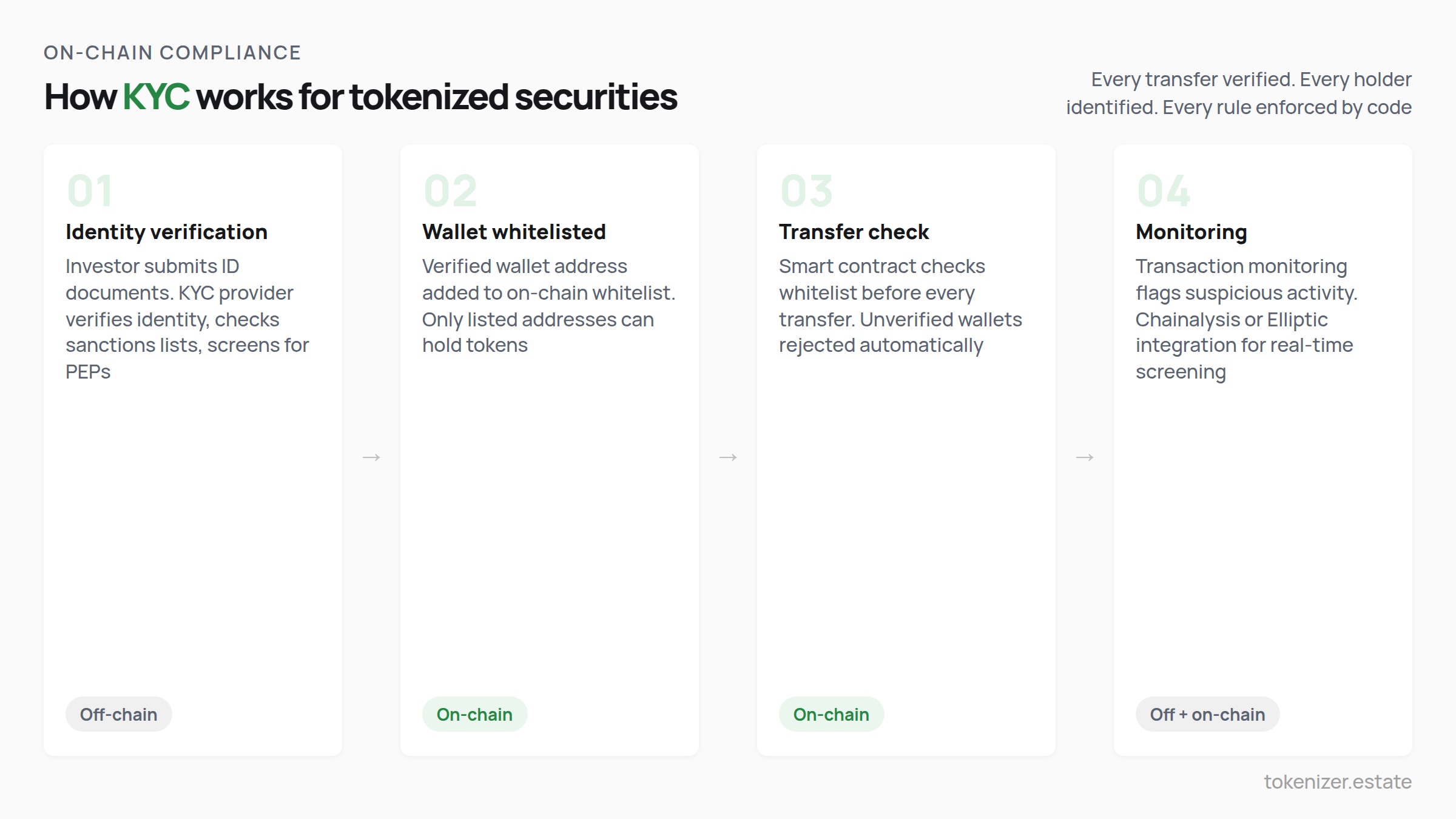

With tokenized securities, KYC is built into the token itself. Here is how it works in practice.

Whitelisting. Before an investor can buy or receive a token, their wallet address must be added to a whitelist. The whitelist is a list of verified addresses stored on the blockchain. Only whitelisted addresses can hold or transfer the token. If an investor tries to send tokens to an unverified wallet, the transaction fails automatically.

Identity registries. Standards like ERC-3643 (used by Tokeny and adopted across European tokenized securities) include an on-chain Identity Registry. Every token holder is linked to a verified identity. The smart contract checks the registry before every transfer. This means compliance is enforced at the protocol level, not by manual checks.

Transfer restrictions. The smart contract can enforce lock-up periods (no selling for 12 months), jurisdictional restrictions (tokens cannot be transferred to wallets in sanctioned countries), and investor limits (maximum 99 non-accredited holders under Reg D). These rules execute automatically. No human intervention required.

Ongoing monitoring. Transaction monitoring tools scan on-chain activity for suspicious patterns. Unusual transfer volumes, rapid buying and selling, or interactions with flagged addresses trigger alerts. Some platforms integrate directly with blockchain analytics providers like Chainalysis or Elliptic for real-time screening.

The result: compliance is continuous, automated, and auditable. Every transfer is recorded on an immutable ledger. Every holder is verified. Every restriction is enforced by code. This is the opposite of the paper-based system where compliance degrades over time.

For a deeper look at how ERC-3643 and other token standards handle compliance, our smart contracts guide covers the five layers that run behind every token.

The Travel Rule and why it matters for secondary trading

The FATF Travel Rule is one of the least understood but most important compliance requirements for tokenized securities. It requires Virtual Asset Service Providers (VASPs) to share sender and receiver information for every transaction above a certain threshold (typically $1,000 to $3,000 depending on jurisdiction).

In practice, this means: when an investor sells their token on a secondary marketplace, the marketplace must collect and transmit the identity information of both the seller and the buyer. This applies to every regulated marketplace in the US, EU, UAE, and Singapore.

Why does this matter for issuers? Because if your tokens trade on a marketplace that does not comply with the Travel Rule, your tokens become toxic. Institutional investors will not touch them. Regulated platforms will not list them. And regulators will trace the compliance failure back to the issuer who allowed non-compliant trading.

The solution: work with platforms and marketplaces that have Travel Rule compliance built in. Ensure your token standard supports the required data fields. And include Travel Rule compliance as a requirement in your offering documents.

What issuers need to build into their deal from day one

KYC/AML is not something you add after the token is created. It must be designed into the deal structure from the beginning. Here is the practical checklist.

Choose a KYC provider before you design the token. Providers like Sumsub, Jumio, Onfido, or Synaps handle identity verification, document checks, sanctions screening, and PEP (Politically Exposed Persons) checks. The provider must support the jurisdictions where your investors will be located.

Select a token standard with built-in compliance. ERC-3643 is the leading standard for regulated tokens. It includes identity registries, transfer restrictions, and compliance modules at the protocol level. Other options include ERC-1400 and ERC-7518. The standard you choose determines how compliance is enforced on-chain.

Define your investor eligibility rules. US accredited investors only (Reg D)? International investors (Reg S)? European qualified investors (MiFID II)? Each category has different KYC requirements. Define these rules before you write the smart contract.

Budget for ongoing compliance. KYC is not a one-time cost. You need ongoing transaction monitoring, annual re-verification of investors, sanctions list updates, and SAR filing capability. Budget $15,000 to $40,000 per year for compliance operations on a mid-size tokenized deal.

Document everything. Regulators want more than confirmation that you ran KYC. They want to see the records: when each investor was verified, what documents were checked, what screening was performed, and how you handle ongoing monitoring. The blockchain gives you the transaction record. But the KYC documentation must be stored off-chain in a compliant, auditable format.

Plan for re-KYC. Investor information changes. People move. Companies restructure. Sanctions lists update. Most jurisdictions require periodic re-verification of investors, typically every 12 to 24 months. Build this into your operations budget and investor communications.

What happens when you get it wrong

The fines are real and they are growing. OKX paid $500 million. Coinbase Europe paid €21.5 million. Starling Bank in the UK paid £29 million for AML failures. These are established companies with large compliance teams.

For a tokenized real estate issuer, the risks go beyond fines. A KYC/AML failure can result in the freezing of your token contract, the forced delisting from secondary markets, criminal liability for directors, and the inability to raise capital in regulated markets in the future. One compliance failure can end a tokenization program permanently.

The positive side: issuers who get compliance right have a competitive advantage. Institutional investors, family offices, and regulated funds can only invest in deals with proper KYC/AML. A well-structured compliance program is not a cost center. It is the gateway to institutional capital.

For the full ecosystem of how compliance connects to legal structure, issuance, custody, and secondary markets, the market map on the Tokenizer blog covers all four layers.

Stay current with regulatory developments at Tokenizer.Estate News.

This article is for informational purposes only and does not constitute legal or compliance advice. KYC/AML requirements vary by jurisdiction, asset type, and investor category. Always consult qualified legal and compliance professionals before structuring tokenized offerings.