Real Estate Tokenization Companies 2026 — Market Map

A developer owns a €40M logistics park. Banks want 40% equity. Tokenization lets 180 investors from 14 countries participate at €5,000 minimum. Here is how the four-layer ecosystem makes it work in 2026.

Let's start with a real situation.

A developer owns a €40 million logistics park outside Lisbon. The asset is good — long-term tenants, stable rental income, strong location. But all the capital is locked inside. To refinance through a bank takes six months and means losing control. To find a co-investor takes even longer. The developer knows there are hundreds of people who would love to put €20,000 into exactly this type of asset — but there is no clean way to let them in.

This is the problem that real estate tokenization solves. And in 2026, the ecosystem to solve it is finally mature enough to trust.

This article is a market map — a clear guide to who does what, how the pieces connect, and what to look for if you are a decision-maker considering tokenizing your asset. Whether it's a commercial building, a resort, a yacht, a factory, or a portfolio of properties — the map is largely the same.

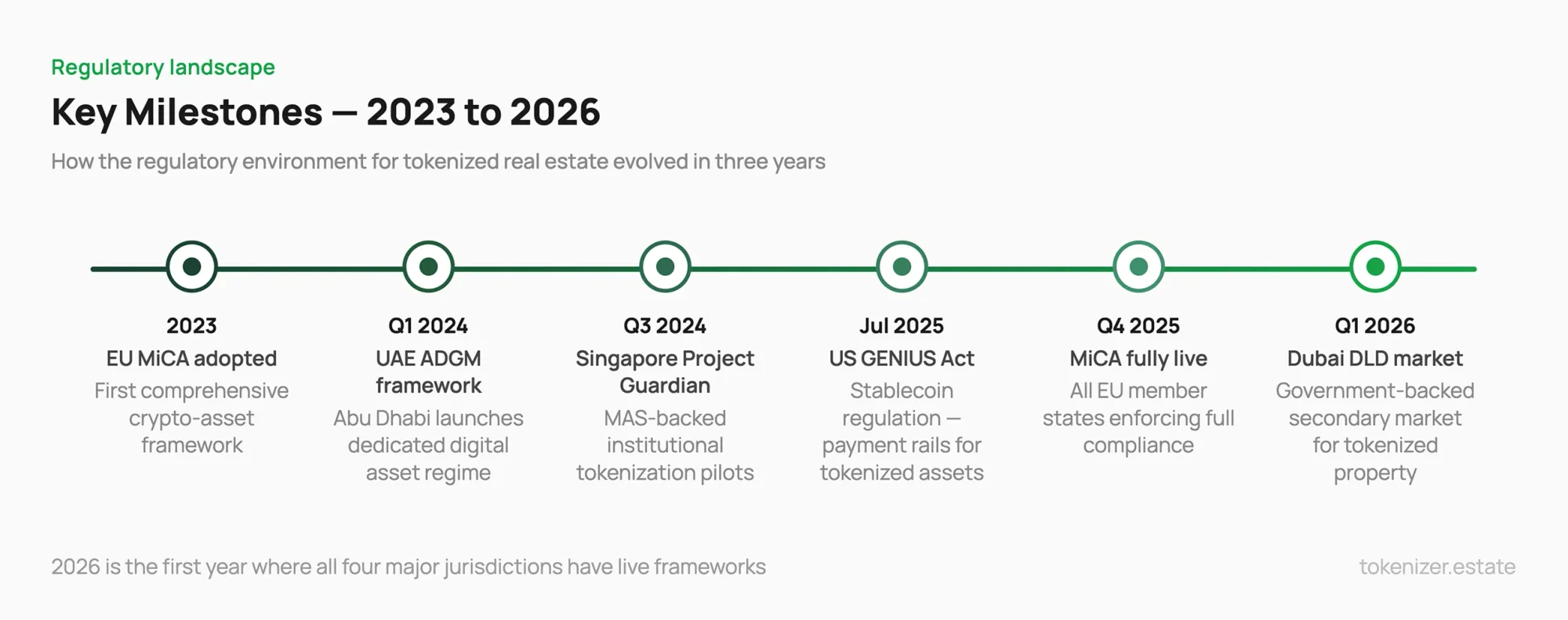

Why 2026 is different from 2021

Real estate tokenization is not new. The first experiments started around 2018. But for years, the technology moved faster than the rules. Projects launched without proper legal structure. Investors couldn't exit. Regulators didn't know what to do.

That has changed. According to Deloitte, tokenized real estate is expected to grow from less than $0.3 trillion in 2024 to over $4 trillion by 2035 — a compound annual growth rate of 27%. But more importantly than the forecast numbers, the infrastructure is now real: regulatory frameworks, compliant custody, secondary markets, and professional issuance platforms all exist and work together.

The US passed the GENIUS Act in July 2025 — a stablecoin regulation that brought clarity to the payment rails tokenized assets depend on. Europe's MiCA regulation is fully live across all member states. The UAE, Singapore, and Saudi Arabia all have working licensing frameworks. The regulatory question is no longer "is this legal?" — it's "which framework fits my deal?"

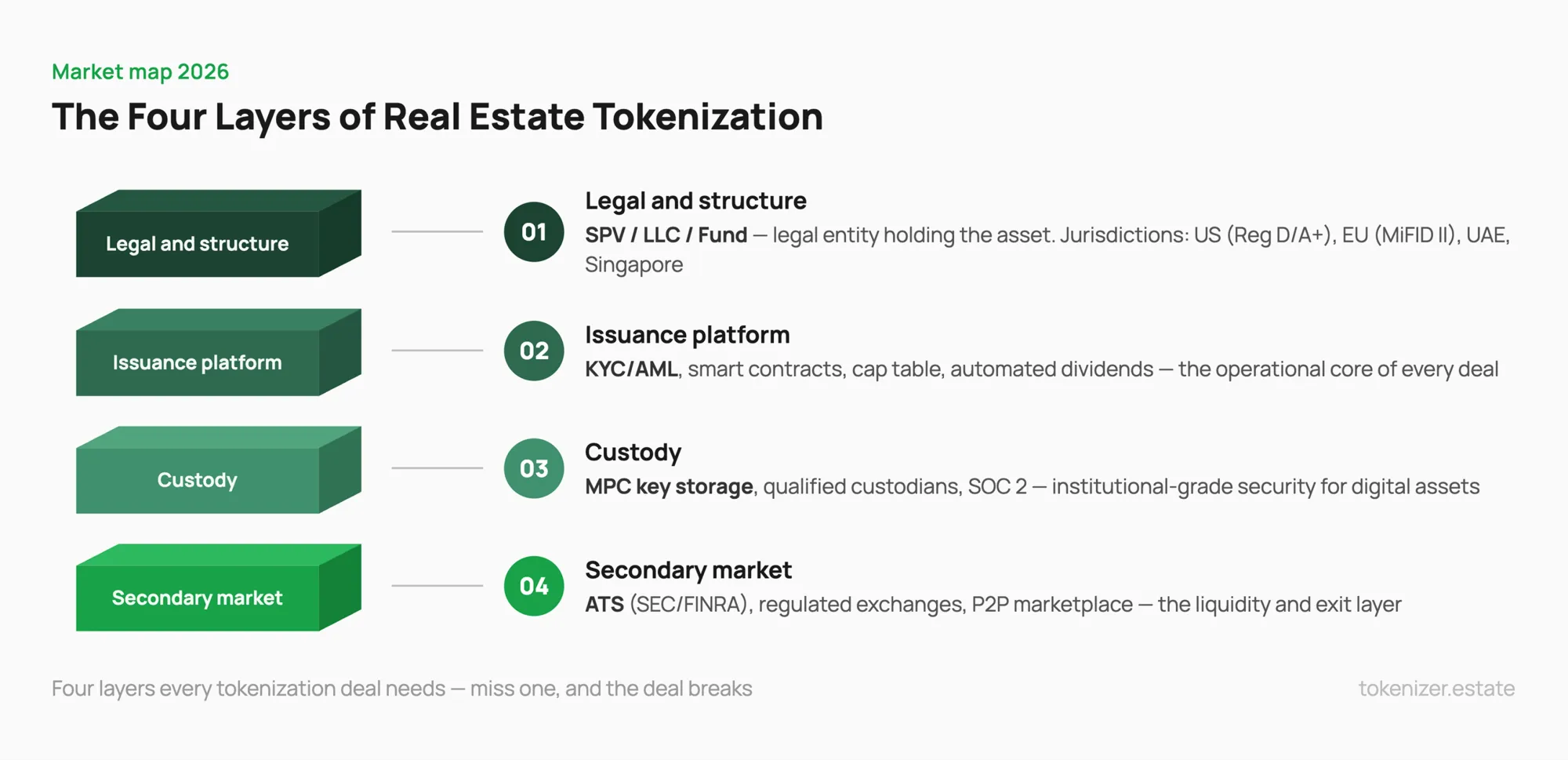

The four layers every tokenization deal needs

When someone says "I want to tokenize my property," they are actually describing a need for four separate types of expertise working together. Miss one layer, and the deal breaks — either legally, technically, or practically.

Here is how the layers work.

Layer 1 — Legal structure: the foundation everything rests on

This is always the first conversation, and it is almost always underestimated.

A token on a blockchain is only as strong as the legal right it represents. If a token represents nothing — no ownership stake, no revenue share, no enforceable claim — then it is just a database entry. The real work happens before any code is written: structuring the asset inside a legal entity that investors can hold a piece of.

In most cases, this means creating a Special Purpose Vehicle (SPV) — a separate company that owns the asset. Investors buy tokens that represent shares or membership interests in that SPV. The SPV collects rental income or sales proceeds and distributes them to token holders automatically via smart contract. The property itself stays in the SPV. The tokens travel on the blockchain.

The jurisdiction you choose determines everything else: which investors you can reach, what disclosures you need, how tokens can be traded, and how quickly you can close.

United States: The most common structures use Reg D (accredited investors only, fast to close, limited secondary trading in the first year) or Reg A+ (open to retail investors, more paperwork, but broader reach). Both are well-understood by the market.

European Union: MiCA covers crypto-assets, but security tokens — which most real estate tokens are — fall under MiFID II. You need an issuer with proper EU licensing, and the offering document requirements are real. Luxembourg and Germany are the most active hubs.

UAE / Dubai: The DIFC and ADGM free zones have built some of the cleanest frameworks for tokenized real estate in the world. Dubai's Land Department (DLD) now runs a government-backed secondary market for tokenized properties — the first of its kind. If you are targeting Gulf investors, UAE is often the easiest path.

Singapore: Project Guardian (run by MAS, the central bank) has validated tokenized real estate structures through live pilots with major banks. The Payment Services Act gives a clear licensing path.

The jurisdiction question is not "where is it easiest?" — it is "where is my target investor, and what structure lets me reach them compliantly?" A good issuance platform answers this question before touching the technology.

Layer 2 — The issuance platform: where the token is born

The issuance platform is the operational core of any tokenization deal. It handles everything from investor onboarding to smart contract deployment to dividend distribution and cap table management.

Think of it as the infrastructure that makes the deal run — before the offering, during it, and for the entire lifetime of the asset.

What to look for in a platform:

Legal and tech in one place. The biggest mistake asset owners make is treating legal structure and technology as separate conversations. They are not. The smart contract has to reflect the legal structure, or the two will conflict the moment something goes wrong. Platforms like Tokenizer.Estate, Securitize, or Tokeny combine legal framework design and smart contract deployment in a single workflow — this approach removes the risk of legal and technical layers conflicting.

Compliance built in, not bolted on. KYC and AML checks are not optional. Every investor who buys a token must be verified — their identity, their residency, their eligibility under the applicable securities law. A good platform automates this for hundreds or thousands of investors across multiple jurisdictions without creating manual work for your team. Look for platforms that integrate with established KYC providers and support multi-jurisdictional verification out of the box.

Your brand, not theirs. If you are a developer or fund manager, your investors should see your name — not a third-party platform's. White-label capability matters for deal credibility and long-term investor relationships.

Audited smart contracts. The code that handles your investors' money must be independently audited. This is non-negotiable. Look for platforms that maintain ongoing security audit partnerships with recognized firms — Hacken, CertiK, OpenZeppelin — not just a one-time check.

No Solidity developers required. A no-code smart contract generator means you don't need to hire blockchain developers or wait months for custom code. You configure the token sale, set distribution rules, and deploy — the platform handles the technical layer. This is table stakes in 2026.

The issuance platform is where most of the day-to-day work lives: onboarding investors, managing token distribution, processing dividends, running the investor dashboard, handling reporting. It is worth spending time choosing correctly here, because switching platforms mid-deal is expensive and disruptive.

Layer 3 — Custody: the trust layer

Custody is the layer that institutional investors look for first — before they even read the offering documents.

When a token represents real value, someone needs to hold the cryptographic keys that prove ownership. If those keys are lost or stolen, the tokens — and the value they represent — are gone. This is not theoretical. It is why serious deals require institutional-grade custody.

The custody layer uses Multi-Party Computation (MPC) — a technology that splits the cryptographic key across multiple secure servers so the complete key never exists in one place. This removes both hacking risk and the single point of failure that comes from any one employee holding full access.

In the US, a "qualified custodian" designation (held by companies with trust charters or federal banking licenses) is required for institutional investors — pension funds, endowments, insurance companies — to legally hold tokenized securities. In Europe and the UAE, equivalent licensing regimes exist.

The custody layer is often invisible to investors — it runs in the background. But its presence (or absence) determines whether institutional money can enter the deal at all. For asset owners raising from family offices, funds, or banks, custody documentation is often the first due diligence request.

Layer 4 — Secondary markets: the exit question

Here is the honest answer to the question every asset owner eventually asks: "Can my investors actually sell their tokens when they want to?"

In 2026, the answer is: yes — but it depends on your structure and jurisdiction.

The secondary market layer is still the most complex part of the ecosystem. A token transfer on a blockchain is fast. But a legal transfer of a security — with proper investor eligibility checks, transfer restrictions, settlement, and record-keeping — requires a compliant trading venue.

Tokenized marketplaces and exchanges are increasingly providing real-time visibility into asset performance, but the liquidity profile of tokenized real estate varies enormously depending on the asset type, investor base, and trading venue.

For US deals, Alternative Trading Systems (ATS) registered with the SEC and FINRA provide the primary venue for secondary trading of tokenized securities. After the initial lock-up period (typically 12 months for Reg D deals), tokens can trade on these venues with proper compliance checks at each transfer.

Dubai's DLD secondary market — launched in early 2026 — is the first government-backed trading platform where tokenized property trades are directly synced to the official land registry. That means a token transfer actually updates the legal ownership record. This is the model the rest of the world is watching closely.

For smaller or newer deals, secondary trading often happens through platform-native marketplaces — peer-to-peer trading within the platform's verified investor network. Less liquid than a regulated exchange, but more accessible and faster to launch.

The honest advice: design for liquidity from day one. Choose the jurisdiction and structure that aligns with your target trading venue. Don't issue tokens and then figure out where they trade — that is backwards, and it is the most common reason tokenization projects stall.

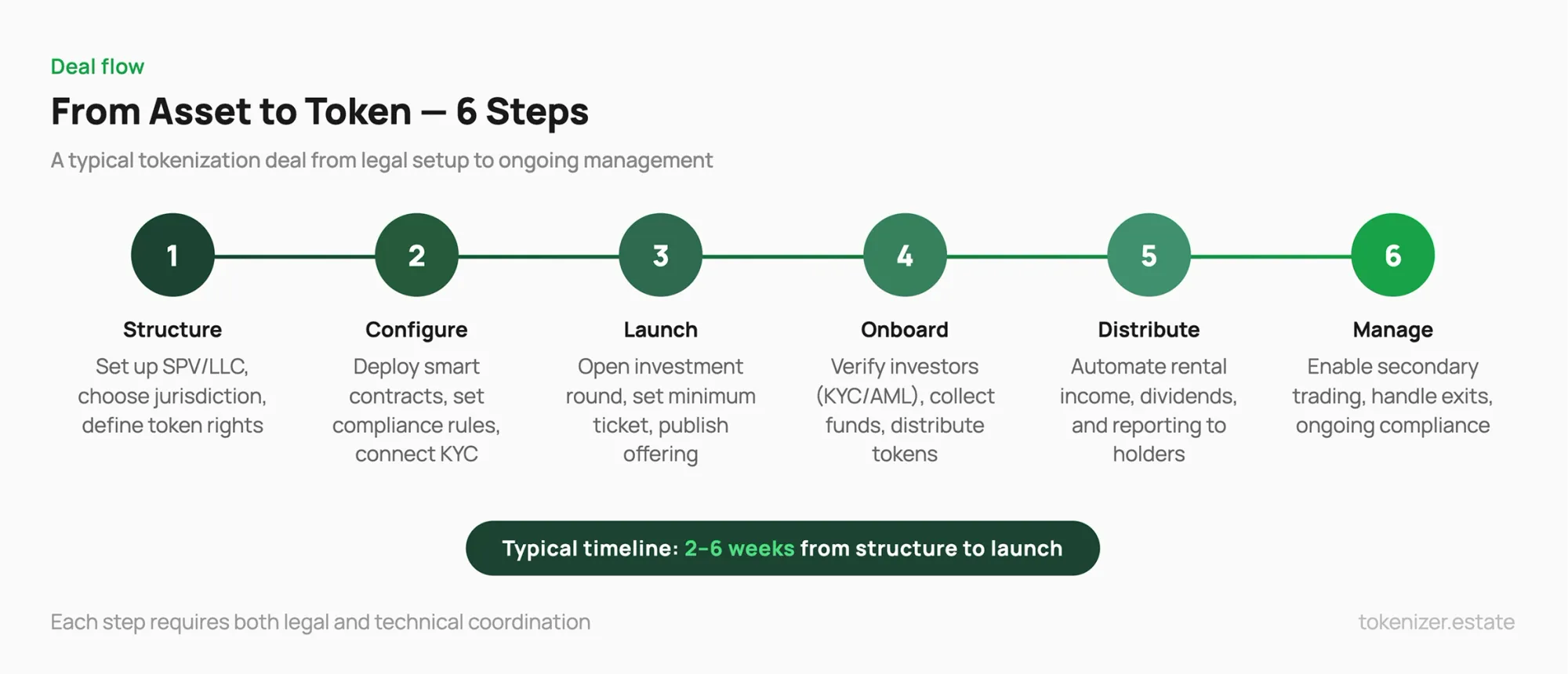

What this looks like in practice

Back to our developer in Lisbon.

He structures the logistics park inside a Portuguese SPV. A tokenization platform handles the legal setup, creates the smart contract, and builds a branded investor portal under his company name. KYC runs automatically for each incoming investor. He sets two phases: a private round for larger investors, then a public offering starting at €5,000 per investor.

Within six weeks of starting the process, 180 verified investors from 14 countries have purchased tokens. The smart contract distributes quarterly rental income automatically in euros, direct to each investor's account. After 12 months, token holders can trade on a compliant ATS or through the platform's P2P marketplace.

The developer raised €6 million without a bank, without giving up equity in his main operating company, and without flying to twelve countries to meet potential investors. His cap table lives on a blockchain, updates automatically, and can be audited by anyone he gives access to.

This is not a future scenario. This is what good tokenization looks like in 2026.

The things that still go wrong

No market map is honest without a section on failure modes. These are the most common ones in 2026:

Skipping the legal layer. Some platforms let you mint a token in 48 hours. That's impressive technically and dangerous commercially. A token without a properly structured legal entity behind it is unenforceable. The legal structure is not a formality — it is the product.

Underestimating compliance. KYC and AML are not one-time checkboxes. They require ongoing monitoring, transfer restrictions, and re-verification for certain events. Platforms that treat compliance as a feature to enable rather than infrastructure to build around cause problems six months into the deal.

No secondary market plan. Investors ask about exit before they invest. If your answer is "we'll figure it out later," you will lose credible investors and attract the wrong ones.

Poor investor communication. A smart contract distributes dividends automatically, but investors still want human updates, reporting, and a clear dashboard. The operational layer of investor relations is often underbuilt in tokenization deals.

The deals that fail are almost always the ones where the legal layer was treated as an afterthought — where the team minted a token and assumed liquidity would follow.

Who is this market actually for in 2026?

The original narrative around tokenization was retail investors getting access to big properties for small tickets. That's real — and it matters. But the bigger story in 2026 is on the asset owner side.

If you own any large illiquid asset — commercial real estate, a resort, a logistics portfolio, a yacht, a factory, even a private credit position — tokenization is now a serious capital strategy. Not an experiment, not a marketing exercise. A real way to access global investor capital, reduce dependence on banks, accelerate deal timelines, and build a more transparent capital structure.

The decision-makers who will benefit most from understanding this market are the ones reading articles like this one: developers, fund managers, family office principals, portfolio owners, executives at asset-heavy companies. Not because tokenization will solve every problem — it won't — but because in 2026, ignoring it means leaving a real tool unused.

The ecosystem is moving fast. Regulatory updates, new deals closing, and infrastructure improvements happen weekly across all four major jurisdictions. Staying current is not optional for anyone entering this market.

Frequently asked questions

What types of assets can be tokenized?

Almost any real asset with a clear legal title: commercial real estate, residential portfolios, logistics parks, hotels, resorts, agricultural land. The common factor is a definable legal structure (usually an SPV) and enough deal size to justify the setup — typically €3–5M minimum.

How much does it cost to tokenize a property?

Setup costs vary by jurisdiction and complexity, but expect €30,000–€80,000 for legal structuring, smart contract deployment, and platform configuration. Ongoing costs include custody fees, compliance monitoring, and investor servicing — typically 0.5–1.5% of assets under management annually.

How long does the process take?

From initial legal structuring to token launch: 2–6 weeks for a straightforward deal with a single jurisdiction. Cross-border structures or complex ownership can take 2–3 months. The technology is not the bottleneck — legal and regulatory approvals are.

Do investors need to understand blockchain?

No. For most tokenized offerings, the investor experience looks like a standard online investment platform: sign up, verify identity, transfer funds, receive ownership confirmation. The blockchain runs in the background — investors interact with a dashboard, not a wallet.

What happens if the platform shuts down?

This is why legal structure matters more than technology. The SPV holds the asset independently of the platform. Token records exist on a public blockchain. A qualified custodian holds the keys. If a platform closes, the legal ownership and token records survive — the asset can be transferred to another service provider.

The practical next step

Understanding the market map is step one. Step two is applying it to a specific asset.

That means asking: What is the asset? Where are the target investors? What legal structure fits the jurisdiction? What platform handles legal, issuance, and compliance in one place? What is the plan for secondary liquidity?

These are answerable questions. The technology is no longer the bottleneck. The strategy — and the right partners — are.

If you own a real asset worth tokenizing, the practical next step is a structured conversation with a platform that understands all four layers. Tokenizer.Estate offers free consultations for asset owners exploring tokenization — no commitment required.

The market is built. The map is readable. The next move is yours.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo