Real Estate Tokenization in Belgium (2026): How a Small Country Is Making Big Moves

Belgium is quietly building Europe's most serious enterprise blockchain ecosystem. Real estate tokenization is moving from theory to practice — with a clearer regulatory framework than most EU countries. Learn how €15M property deals can close in 5 days with 80 global investors.

Imagine you own a €15 million office building in Brussels. To bring in a co-investor, you need a notary, a lawyer, six weeks, and a buyer who is local enough to care. Now imagine doing the same deal in five days, with 80 investors from Germany, the Netherlands, and Singapore — all through a digital token on a blockchain.

This is not a pitch. This is where Belgium is heading in 2026 — and faster than most people in the real estate industry realize.

Belgium is not the loudest voice in the blockchain conversation. But it has quietly built one of the most serious enterprise blockchain ecosystems in Europe. Its biggest bank has already issued a euro token. Its companies power tokenization infrastructure across three continents. And now, this infrastructure is starting to move into real estate — with a regulatory framework that is clearer than in most EU countries.

If you want to understand what tokenization means for Belgian property — what is already legal, what actually works, and where the real opportunity is — read on.

What Is Tokenization

Let's keep this simple. Real estate tokenization means converting ownership rights over a property — or a share in it — into digital tokens on a blockchain. Each token represents a piece of the asset. These tokens can be issued, sold, and traded digitally, with automatic settlement and no paper contracts changing hands.

Why does this matter for serious real estate players? Because it solves three old problems at once.

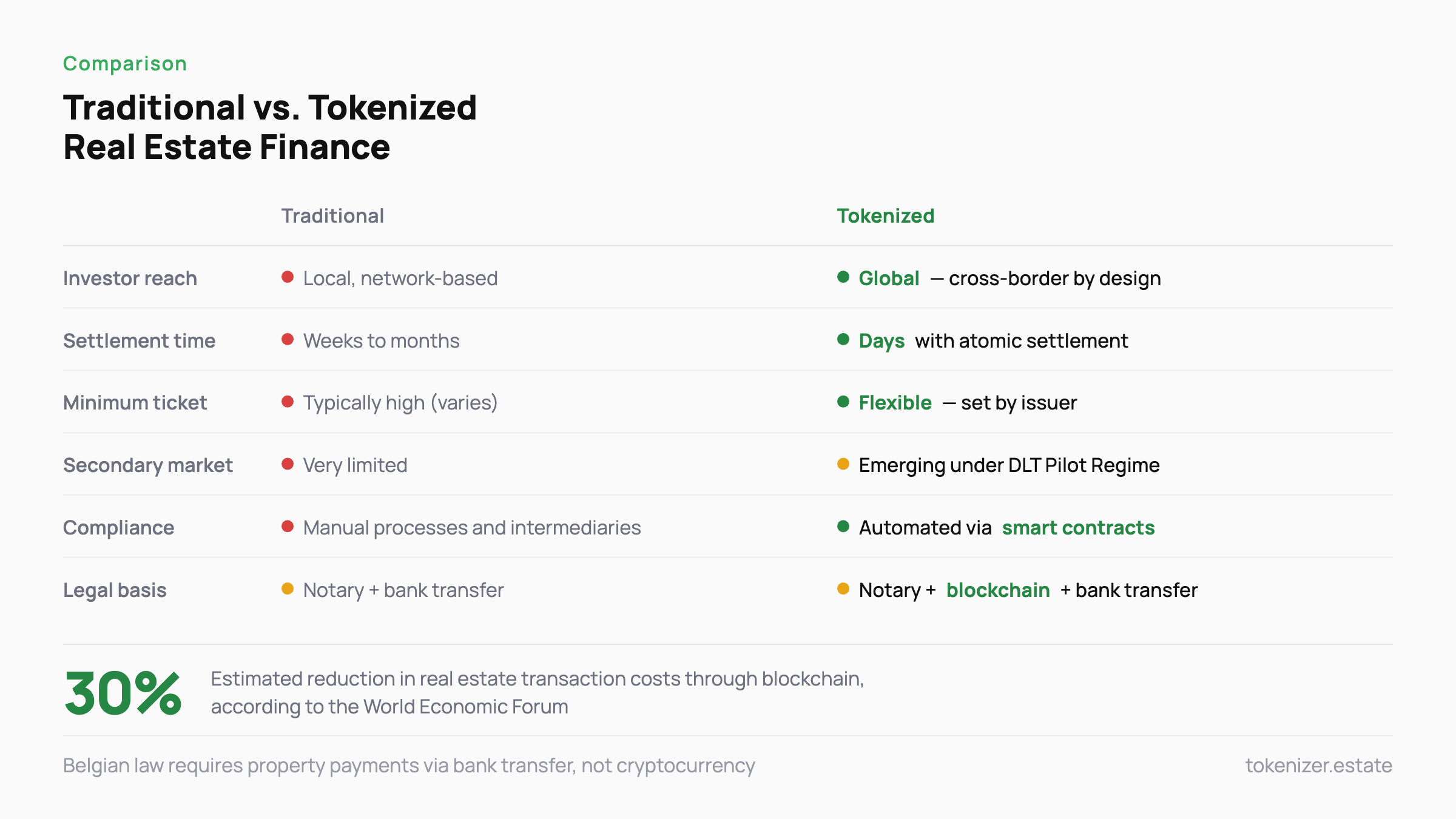

First, liquidity. Real estate is the world's largest asset class — but it is famously illiquid. Selling a building takes months. Tokenization makes it possible to sell a share of a property in days, or even hours, on a secondary market.

Second, access to capital. A tokenized asset can be offered to investors across the world, not just the handful of buyers who happen to be in your city or know your bank manager. This opens up a completely different capital base.

Third, operational efficiency. Smart contracts handle dividend distribution, investor reporting, and compliance automatically. Less paperwork. Fewer intermediaries. Lower costs — the World Economic Forum estimates blockchain can reduce transaction costs in real estate by up to 30%.

None of this is theory anymore. As of 2025, the global tokenized real estate market has surpassed $10 billion in value, and Deloitte projects it will reach $4 trillion by 2035. The question is not whether this is happening. The question is whether you will be in position when it does.

Why Belgium

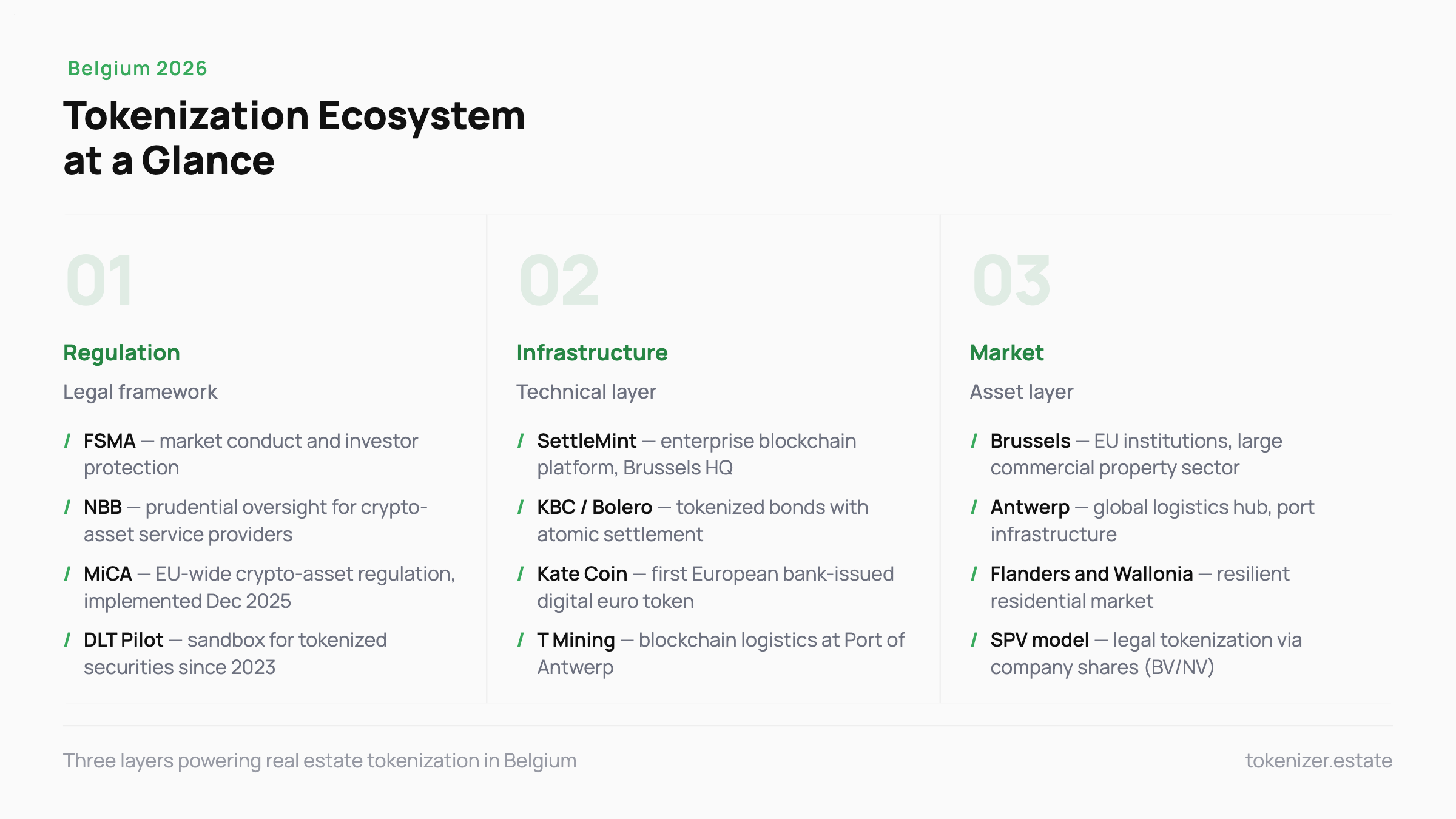

Belgium has a stable and mature real estate market. Brussels is a major European capital with a large commercial property sector driven by EU institutions and multinational corporations. Antwerp is a global logistics hub. The residential market across Flanders and Wallonia has remained resilient even as interest rates moved higher in 2022–2024.

But the more interesting story is on the infrastructure side.

Belgium punches above its weight in the enterprise blockchain space. Belgian banks and companies have already delivered notable firsts: the first European bank-issued digital coin, tokenized SME bonds, and port logistics tracked on blockchain. These are not startup experiments — they are live, production systems at major institutions.

SettleMint, a Belgian blockchain company, has become a key player in enterprise tokenization across Europe, powering infrastructure for banks and governments on multiple continents. T Mining, another Belgian firm, manages container logistics at the Port of Antwerp using blockchain. These companies show that Belgium has real technical depth in this space — not just regulatory ambition.

This combination — a large, liquid property market plus an active blockchain ecosystem — creates the right conditions for real estate tokenization to take hold.

Belgian Regulations

Regulation is always the first question. And in Belgium, the picture has become noticeably clearer in the past 12 months.

Belgium operates on a "Twin Peaks" model for financial supervision. The Financial Services and Markets Authority (FSMA) is responsible for market conduct and investor protection, while the National Bank of Belgium (NBB) handles prudential oversight. For tokenized assets, both institutions are relevant depending on what the token represents.

The most important development came at the end of 2025. Belgium passed the Law of 11 December 2025, which implements the EU's MiCA Regulation (Markets in Crypto-Assets) into Belgian national law. This law formally divides supervisory responsibilities between the FSMA and the NBB for crypto-asset service providers.

MiCA matters a lot for anyone issuing or dealing in tokenized real estate. Under MiCA, if your token qualifies as a crypto-asset, you need to follow specific rules on issuance, investor disclosure, and custody. If your token qualifies as a financial instrument — which security tokens typically do — then MiFID II rules apply instead.

For most real estate tokenization structures, this means your token will be treated as a security. That requires FSMA involvement, a proper prospectus or exemption, and a licensed intermediary to handle distribution.

Any Virtual Asset Service Provider (VASP) operating in Belgium must register with the FSMA. Providers from outside the European Economic Area are not allowed to offer these services in the country.

The EU's DLT Pilot Regime, which has been active since March 2023, adds another layer. It allows regulated financial institutions to issue, trade, and settle tokenized securities on blockchain infrastructure under temporary exemptions from traditional rules. Belgium participates in this regime, giving institutional players a legal path to test tokenized securities in a live environment.

One important Belgium-specific rule that everyone involved in real estate should know: under Belgian law, the price of acquired real estate must always be fully paid in scriptural money (bank transfers), not in cryptocurrency. This means that even if a property is tokenized and ownership changes hands on blockchain, the actual payment must still go through traditional banking channels. Tokens can represent the ownership, but the cash settlement stays off-chain.

This is not a dealbreaker — it is simply a design constraint that good legal structuring can handle. But it is essential to understand upfront.

Token Structures

This is the most practical question, and the answer shapes everything about how you structure a deal.

In Belgium, as in most EU jurisdictions, you cannot directly put a property title on a blockchain. The notarial system and the land register (Kadaster/Conservation des hypothèques) remain the legal source of truth for property ownership. A blockchain record does not override or replace those registries.

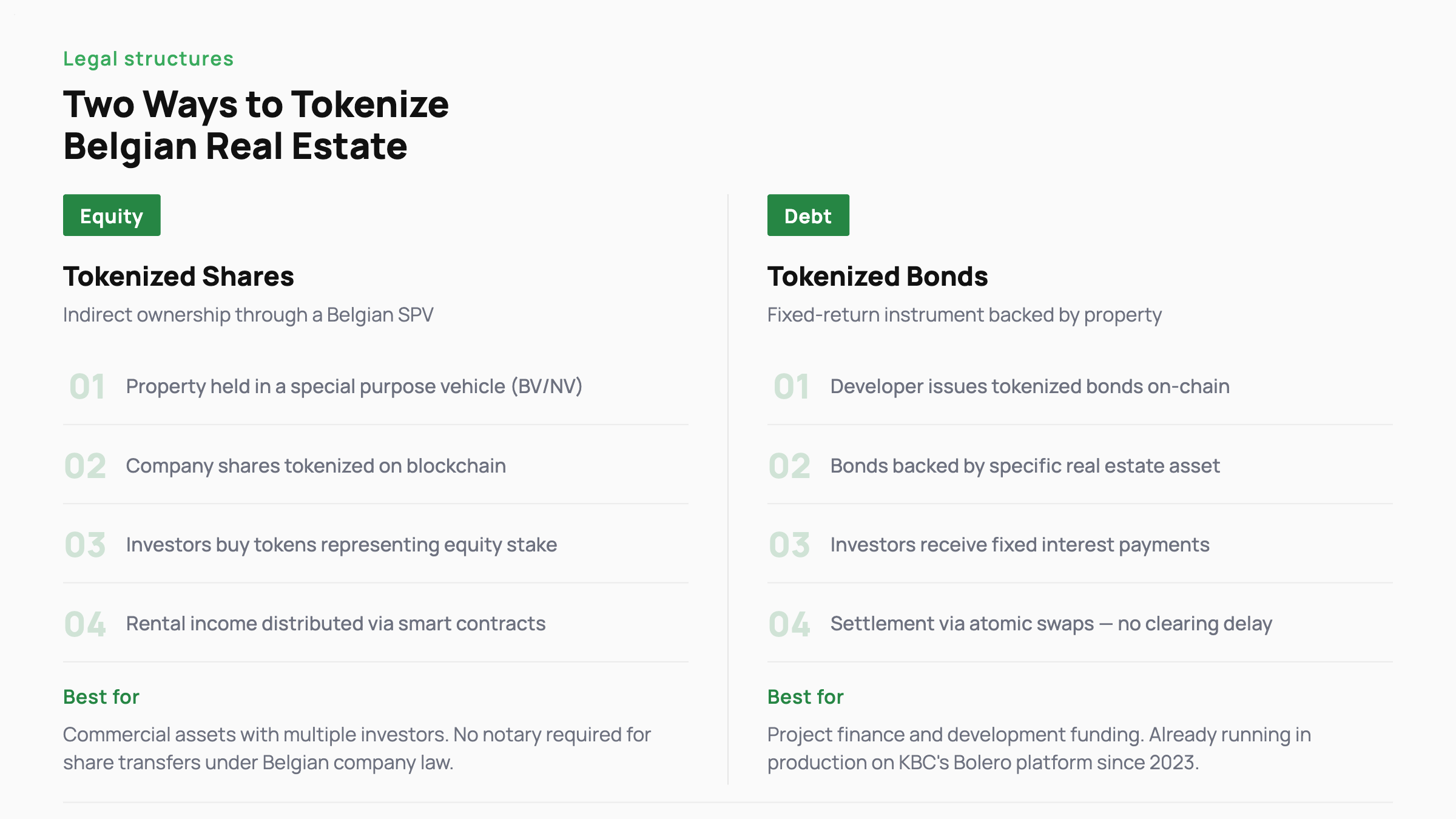

So what can a token represent? In practice, there are two main approaches:

Company shares (SPV model). A property is held inside a special purpose vehicle — typically a Belgian SRL/BV or NV. The shares of that company are tokenized. Token holders become indirect co-owners of the property through their equity stake. This is the most commonly used structure in Europe, and it works cleanly under Belgian company law. Transfers of shares do not require a notary.

Debt instruments / bonds. A developer issues tokenized bonds backed by the property. Investors receive fixed returns (interest), not equity. This is simpler from a regulatory perspective and does not involve any change in property ownership. KBC's Bolero Crowdfunding platform — powered by SettleMint — has already done exactly this for SME financing.

Both models have real use cases in Belgian real estate. The SPV model works well for commercial assets with multiple investors. The bond model works well for project finance and development funding.

Who Is Moving Now

Several Belgian institutions are laying the groundwork — even if none have announced a flagship real estate tokenization deal yet.

KBC Group is the clearest example of what institutional tokenization looks like in practice.

In November 2023, KBC Securities launched tokenized fixed-income products for SMEs through its Bolero Crowdfunding platform — built on SettleMint's infrastructure. The structure used atomic swaps: both the securities leg and the cash leg settled on-chain simultaneously, with no clearing delay and no manual reconciliation. Multiple issuances have run in production since then, with individual bond offerings in the range of €500,000 to €2 million, accessible to retail investors on the Bolero platform with a minimum ticket that fit normal crowdfunding thresholds.

KBC also launched Kate Coin — a euro-denominated digital token integrated directly into retail banking, one of the first bank-issued digital coins in Europe. The token is held in customers' regular KBC app, not a separate crypto wallet. This matters because it shows that Belgian banking infrastructure can deliver tokenized instruments to mainstream users without requiring them to understand blockchain at all.

This is the kind of end-to-end settlement that makes tokenization genuinely efficient, not just cosmetically digital. And it is the same infrastructure that can be applied to property-backed instruments. The bank already has the plumbing. What comes next is the asset class.

SettleMint, headquartered in Brussels, is a global blockchain infrastructure company that has worked with banks, governments, and regulators across Europe, the Middle East, and Asia. They provide the technical layer that many institutions use to build tokenized products. Their presence in Belgium means local developers and fund managers can access enterprise-grade tokenization technology without going abroad.

Blockchain4Belgium is an industry coalition that has worked with both the private sector and government to create a favorable environment for blockchain adoption. Through initiatives like Blockchain4Belgium, the country has engaged regulators and fine-tuned rules to encourage compliant blockchain projects.

The FSMA also operates a FinTech Contact Point — a dedicated channel where startups and established firms can ask questions about regulation before launching a product. This is a practical signal that Belgium is open to innovation, not just enforcement.

You can follow new Belgian and European tokenization developments as they happen at news.tokenizer.estate — the feed covers deals, regulation changes, and platform launches across the continent on a weekly basis.

What Works & What Doesn't

It would be dishonest to make this sound like a solved problem. Let's be direct about where Belgium is strong and where friction still exists.

What works:

Tokenizing shares in a Belgian real estate SPV is legally clean today. You create a company, it holds the property, and you issue digital tokens representing shares. Belgian company law supports digital share registers. Investors can transfer tokens peer-to-peer without a notary. Dividend and rental income distribution can be automated via smart contracts.

Tokenizing real estate debt (bonds) is also well-supported, especially under the MiCA framework for crypto-assets or under MiFID II for securities. KBC's Bolero platform is proof that Belgian institutions can do this at scale.

What is still difficult:

Secondary market liquidity remains limited. Most tokenized real estate products in Europe are still traded within the platform that issued them, not on open exchanges. This limits the liquidity benefit that makes tokenization attractive in the first place. This is a European-wide issue, not specific to Belgium — but it is something to plan for when designing a tokenized structure.

AML and KYC requirements are serious. Every investor must be identified, verified, and checked against sanctions lists. Smart contracts can help automate some of this, but the compliance burden is real and ongoing. For Belgian structures under FSMA oversight, this is non-negotiable.

Notary and registry integration remains off-chain. As mentioned earlier, Belgian property law does not yet recognize blockchain as a legal property register. All on-chain ownership changes must align with off-chain legal records. This creates operational complexity that legal counsel must address at the outset.

For Real Estate Professionals

If you develop, own, or finance real estate in Belgium, tokenization is not something to watch from a distance. It is becoming a tool for competitive advantage.

For developers: Tokenization opens access to a much wider pool of capital. Instead of going to one bank or a small group of institutional investors, you can reach hundreds or thousands of investors across Europe through a compliant digital offering. This can speed up project financing and reduce dependence on any single lender.

For owners of commercial assets: Large commercial properties — office buildings, logistics warehouses, retail portfolios — are well-suited for tokenization. They generate stable cash flows, they are large enough to justify the setup costs, and they attract the kind of institutional and semi-institutional investors who are already comfortable with digital assets.

For investors: Tokenized real estate offers exposure to Belgian property without the liquidity lock-up of traditional co-ownership. If secondary market infrastructure continues to develop — which it is, across Europe — you will eventually be able to exit a position without waiting for a buyer of the entire building.

To understand how other EU jurisdictions have already structured these deals — and which models are worth copying — the Tokenizer.Estate blog covers country-by-country breakdowns on legal structure, regulatory pathways, and real examples from the Netherlands, Estonia, Luxembourg, and beyond.

Frequently Asked Questions

Is real estate tokenization legal in Belgium? Yes. Tokenizing shares in a Belgian SPV that owns property is legal today under existing company law. Tokenizing debt instruments (bonds) backed by property is also legal under MiCA or MiFID II depending on the structure. What is not possible yet is putting a property title directly on a blockchain — the land register remains the legal record, and it is still off-chain.

What regulation applies to tokenized real estate in Belgium? It depends on what your token represents. If it behaves like a security (equity or bond), MiFID II applies and FSMA oversight is required. If it is structured as a crypto-asset under MiCA, then the Law of 11 December 2025 governs it, with shared FSMA and NBB supervision. Most real estate tokens fall under the MiFID II category.

Can foreign investors buy tokenized Belgian real estate? Yes, in principle. EU investors can participate in tokenized offerings that are properly registered or exempt under EU prospectus rules. Non-EU investors can participate if the issuer has structured the offering to comply with applicable laws in the investor's home jurisdiction. The technical infrastructure to handle cross-border investor onboarding — including KYC/AML — already exists in Belgium.

What is the minimum deal size that makes tokenization worth it in Belgium? There is no legal minimum, but in practice the setup costs — legal structure, FSMA engagement, smart contract development, and investor onboarding — make it hard to justify for assets below €3–5 million. For commercial properties, logistics assets, or development projects above €5 million, the economics work clearly. Below that, tokenized bond structures are often a simpler and cheaper entry point.

Conclusion

The next 12 to 24 months will be important for Belgium specifically.

Under the MiCA transitional regime, crypto-asset service providers that operated before December 2024 can continue until July 2026 while applying for full authorisation from the FSMA. After that date, only fully licensed CASPs will be allowed to operate. This deadline is pushing players in the market to get properly authorized — which means more institutional-grade infrastructure coming online.

The EU's DLT Pilot Regime is also up for review by the European Commission in 2026. The decision on whether to make it permanent will significantly affect how banks and asset managers approach tokenized securities across the continent — including in Belgium.

Meanwhile, the Belgian property market itself is going through real change in 2026. New EPC (energy performance) obligations, regional tax shifts, and interest rate normalization are all reshaping investment calculations. Tokenization adds another tool to the kit for developers and owners who want more flexible capital structures in a more complex environment.

The institutions that build their tokenization capability now — legal structure, technical infrastructure, FSMA relationship, investor base — will be in a very different position when the market reaches full scale than those who wait.

Belgium has the banking infrastructure, the regulatory framework, and the technical ecosystem to become a real hub for European property tokenization. The groundwork is already in place. What remains is for the real estate industry to pick it up and use it.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo