Real estate tokenization in Mexico 2026: the $169 billion market that is still waiting

Mexico has a $169 billion real estate market, a fintech law from 2018, and blockchain land registry pilots in Tulum. But dedicated real estate tokenization rules have not arrived yet. This is the practical picture — regulation, projects, tax, and what asset owners should prepare for now.

Mexico has a $169 billion real estate market, 130 million people, a coastline that draws millions of tourists every year, and a nearshoring boom that is filling industrial parks faster than developers can build them. More than 500,000 Americans already own property here. The Riviera Maya alone generates billions in vacation rental income annually.

And yet — Mexico has zero tokenized real estate deals at institutional scale.

That is not because the country lacks interest. It is because Mexico sits in an unusual position: it has a fintech law that is more advanced than most of Latin America, blockchain pilots that work, and a real estate market that badly needs better capital access. But the specific rules for tokenizing property have not arrived yet. In 2025, public consultations on real estate tokenization frameworks began. The pieces are moving.

This article maps where Mexico stands right now — what the law allows, what it does not, where projects are happening anyway, and why this market is worth watching if you own, develop, or invest in real assets anywhere in the Americas.

Why Mexico is different from every other LATAM market

Brazil has COFECI Resolution 1.551 — the first dedicated real estate tokenization regulation in Latin America. Argentina issued Resolution 1081 to set rules for tokenized financial assets. Colombia approved a bill regulating crypto exchanges.

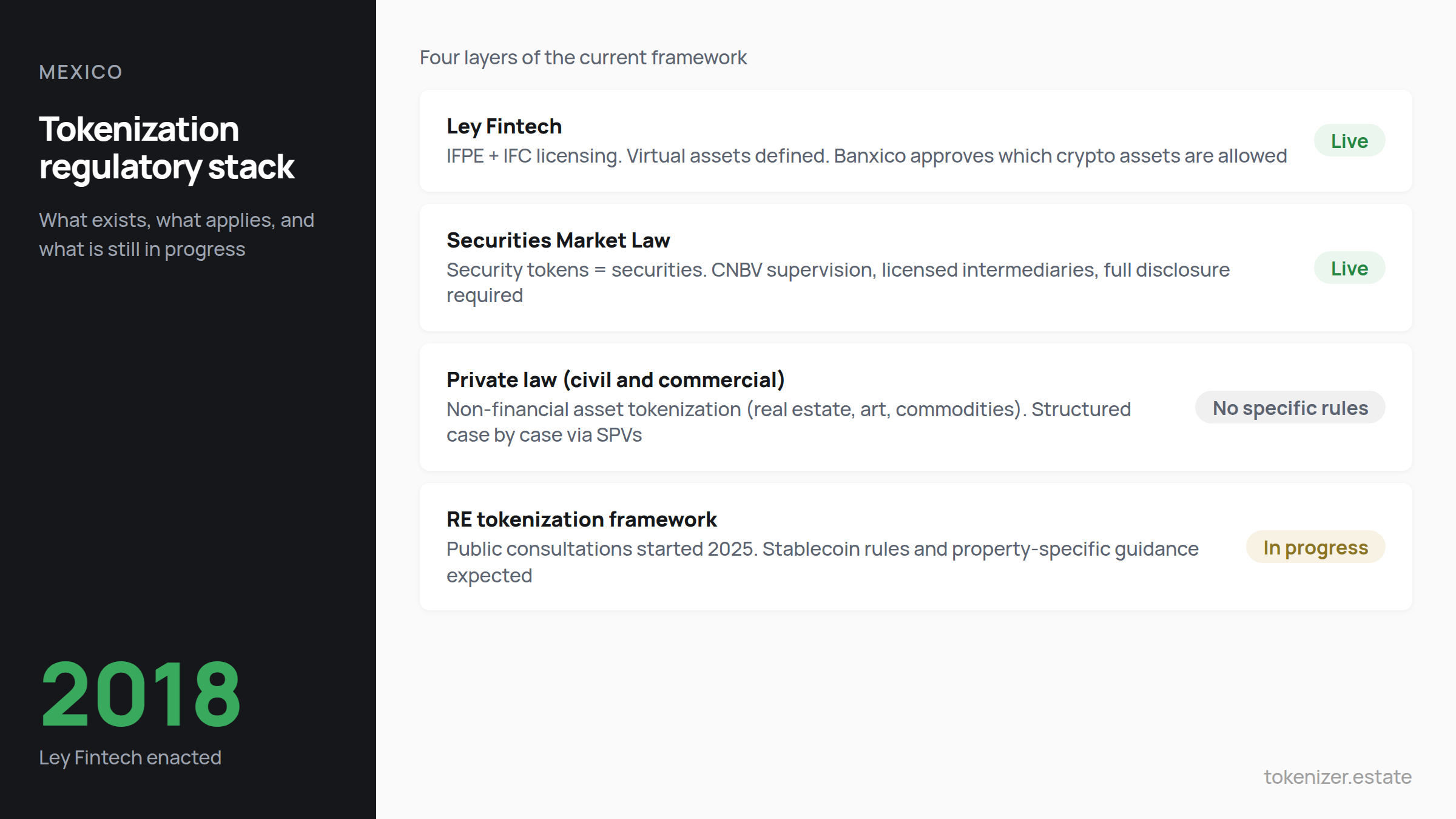

Mexico took a different path. In 2018, it passed the Ley Fintech — the Law to Regulate Financial Technology Institutions. At the time, this was one of the most advanced fintech regulations in the world. It defined virtual assets, created a licensing framework for fintech companies, and gave the central bank (Banxico) authority to decide which crypto assets could be used in the financial system.

But the Fintech Law was built for payments and lending, not for tokenized property. It creates two types of licensed entities: electronic payment institutions (IFPE) and crowdfunding institutions (IFC). Neither category was designed with security tokens or fractional real estate in mind.

The result is a framework that is permissive but conservative. Non-financial companies can operate with crypto assets — but banks and fintech firms face heavy restrictions on offering virtual asset services to the public. Banxico explicitly maintains a "healthy distance" between virtual assets and the traditional financial system.

For real estate tokenization specifically, Chambers & Partners notes in its 2025 guide that security tokens representing equity or debt are fully subject to the Securities Market Law. Their issuance and trading require licensed intermediaries, CNBV supervision, and standard disclosure requirements. For non-financial asset tokenization — like real estate, art, or commodities — there is still no specific regulation. These projects are structured under Mexican private law and must follow civil, tax, and commercial rules.

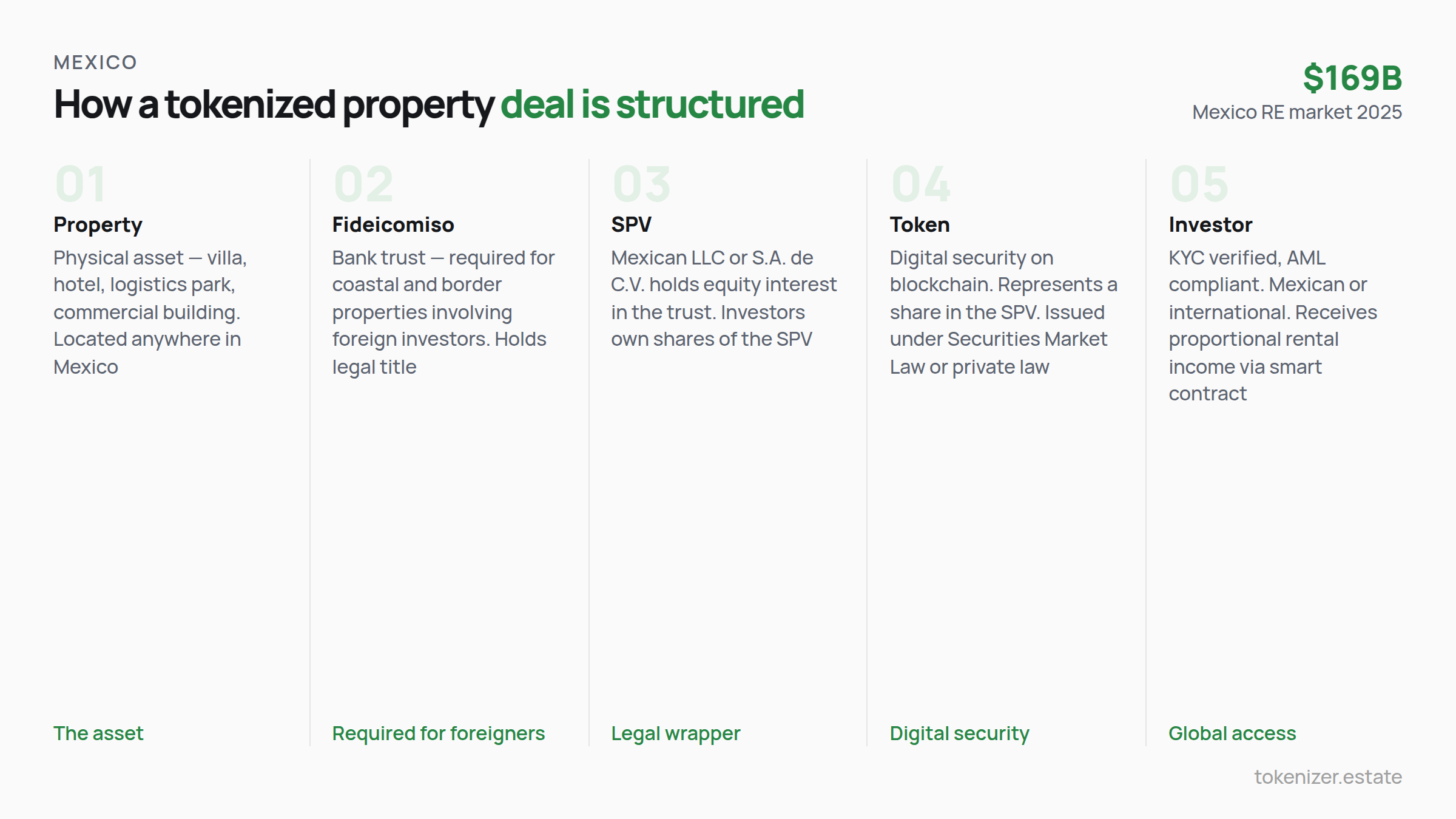

This creates a gap. The law does not prohibit real estate tokenization. But it does not provide a clear, dedicated path either. Developers and asset owners who want to tokenize must work with lawyers to structure deals under existing law — typically through SPVs, fideicomisos (trusts), or crowdfunding structures that comply with CVM Resolution 88 equivalents.

The real estate market — why it matters for tokenization

Mexico's real estate market reached $169 billion in 2025 and is projected to grow to $239 billion by 2034. The residential segment alone is expected to hit $21 billion by 2033. But these numbers only tell part of the story.

The market has structural features that make tokenization particularly relevant.

Nearshoring is driving demand at a speed Mexico has not seen before. US and multinational companies are relocating manufacturing to Mexico at a pace not seen in decades. Cities like Monterrey, Tijuana, and Ciudad Juárez are seeing industrial parks fill up and residential demand surge. Developers need capital to build fast. Traditional bank financing — already slow in Mexico — cannot keep up.

Foreign ownership has a built-in complexity layer. Mexico's constitution restricts direct foreign ownership of property within 50 kilometers of the coast and 100 kilometers of the border. Foreign buyers must use a fideicomiso — a bank trust that holds the property on their behalf. This adds cost, time, and intermediary fees. Tokenization through SPVs could simplify this structure while maintaining legal compliance.

Tourism drives rental yields but locks up capital. Tulum, Cancún, Playa del Carmen, Puerto Vallarta, Cabo San Lucas — these markets generate strong vacation rental income. A villa in Tulum can fetch $1,000 per night. But the capital to build or buy these properties is locked once invested. There is no liquid secondary market. If you want to exit, you sell the whole property — a process that takes months and involves brokers, notaries, and tax complexity.

Land tenure is messy. Roughly half of Mexico's land is classified as ejido — communal land with complex ownership rules that can delay or kill real estate projects. Blockchain-based land registries could bring transparency to a system that badly needs it. Medici Land Governance already launched a pilot in Tulum, creating a digital record of land ownership on blockchain. RE/MAX partnered with XYO Network for decentralized location verification in property transactions.

These are not theoretical problems. They are daily operational pain for anyone building, buying, or selling real estate in Mexico. Tokenization addresses several of them directly — particularly capital access, fractional ownership, and cross-border investment.

For a broader view of how tokenization is developing across Latin America — including Brazil's dedicated regulation — the Brazil country case on the Tokenizer blog covers the most advanced LATAM market.

What is actually happening on the ground

Mexico does not have a live tokenized real estate exchange like Brazil's Netspaces. But projects are running — mostly structured by international platforms that include Mexican properties in their portfolios.

Reental, a Spanish tokenization platform, has tokenized vacation properties in Tulum and San Miguel de Allende. Both are tourist-use properties where investors buy tokens and receive a share of rental income. The Tulum property — a villa with a private cenote in the jungle — sold out through token sales to an international investor base. Reental structures these deals as participative loans under Spanish and EU crowdfunding regulations, which sidesteps the need for Mexican-specific tokenization rules.

The Landmark in Monterrey was one of the early tokenized real estate projects in Mexico — a commercial development that issued digital securities to investors. While details on its current status are limited, it demonstrated that Mexican developers are willing to explore this model.

Nectar Tulum raised capital through Republic, a US-based investment platform, using Reg CF (crowdfunding regulation). While not pure blockchain tokenization, it showed that Mexican resort properties can attract global micro-investors through digital securities — a close cousin of tokenization.

Project Agora is perhaps the most significant signal. This is a Bank for International Settlements initiative exploring tokenized bank deposits and cross-border settlement. Mexico's consortium — which includes Solana, Stellar, Bitso, and Etherfuse — is participating. Bitso, Mexico's largest crypto exchange, is deeply involved. The project does not tokenize real estate directly, but it builds the settlement infrastructure that tokenized property deals will eventually run on.

These projects are scattered and early. None of them represent institutional-scale real estate tokenization within Mexico's domestic regulatory framework. But they prove that the demand exists, the technology works, and Mexican assets are attractive to global tokenized capital.

The tax and legal picture — what you need to know

If you are considering tokenizing a Mexican property or investing in one, here is what the current rules look like.

Security tokens are securities. If your token represents equity, debt, or a profit-sharing right, it falls under the Securities Market Law. You need a licensed intermediary, CNBV authorization, and standard disclosure. This is the same process as a traditional securities offering — the token is just the format.

Non-security tokens sit in a gray zone. If your token represents access rights, utility, or a contractual claim that does not qualify as a security, the Fintech Law and general private law apply. There is no specific registration or licensing requirement, but you must comply with AML/KYC obligations, consumer protection rules, and standard tax reporting.

Tax treatment. Mexico taxes capital gains from the sale of digital assets. The tax rate depends on the type of income and the taxpayer's residency. Mexican residents pay income tax on worldwide income, with rates up to 35%. Non-residents face a 25% withholding tax on Mexican-source income. Rental income from tokenized properties would be taxed as regular rental income under Mexican tax law.

The fideicomiso question. For coastal and border properties involving foreign investors, the fideicomiso trust structure remains necessary. Tokenization does not eliminate this requirement — but it can sit on top of it. The token represents a beneficial interest in the trust, while the trust holds the property. This layered structure adds legal complexity but is workable.

Blockchain as evidence. A 2023 law gave blockchain records legal recognition as documentary evidence in Mexican courts. This is a small but meaningful step — it means that on-chain records of token ownership, transfers, and distributions can be used in legal proceedings.

What is missing — and when it might arrive

Mexico's tokenization story in 2026 is a story of almost. Almost ready. Almost there. The building blocks exist, but the specific framework does not.

No dedicated RE tokenization regulation. Unlike Brazil (COFECI 1.551) or the UAE (VARA), Mexico has not issued rules that specifically address how to tokenize property, who can do it, and what investor protections apply. The 2025 public consultations are a start, but no timeline for final rules has been announced.

Banxico remains cautious. The central bank's stance — maintaining a "healthy distance" between virtual assets and the financial system — means that banks cannot easily participate in tokenized real estate deals. This limits the liquidity and institutional credibility that the market needs to scale.

No CBDC for settlement. Brazil has Drex. Mexico's CBDC plans remain in early research. Banxico announced a retail digital currency around 2025, but the project has faced delays. Without a blockchain-native settlement layer, tokenized property transactions still rely on traditional banking rails for the peso side of the deal.

Secondary markets do not exist domestically. There is no Mexican platform where tokenized real estate can be traded. Deals structured through international platforms (Reental, Republic) use those platforms' own marketplaces. A domestic secondary market requires regulatory clarity that does not yet exist.

But the direction is clear. The public consultations, Project Agora participation, blockchain evidence laws, and fintech ecosystem growth all point the same way. Mexico is not opposed to real estate tokenization — it is cautiously building toward it.

Stay current with regulatory developments across LATAM and other markets at Tokenizer.Estate News.

Who should be watching this market

Mexico is not a market where you can tokenize a building tomorrow. But it is a market where preparation matters.

Mexican developers and asset owners in tourism hotspots — Tulum, Cancún, Puerto Vallarta, Cabo, San Miguel de Allende — are sitting on assets that international investors want access to. When regulation arrives, the first movers who have already structured their SPVs, cleaned up their land titles, and prepared their legal wrappers will close deals while competitors are still hiring lawyers.

Industrial and logistics operators in the nearshoring corridor — Monterrey, Tijuana, Ciudad Juárez, Querétaro — need capital faster than banks can provide it. Tokenization offers a path to raise from hundreds of investors globally without giving up control. The industrial assets are strong: long-term leases, corporate tenants, growing demand. When the framework is ready, these will be the first to move.

International investors looking at LATAM real estate should understand Mexico's position. The market is larger than Brazil's in total value. The tourism yields are strong. The nearshoring story is real. And the fact that tokenization is still early means pricing has not adjusted for the liquidity premium that tokenization will eventually bring.

Family offices and asset-heavy operators — whether your assets are commercial buildings, hotels, marinas, or industrial facilities — the question is not whether Mexico will enable tokenized capital raising, but when. The legal infrastructure (Fintech Law, Securities Market Law, blockchain evidence recognition) is already in place. The specific rules are what is missing.

For a comparison of how different jurisdictions handle tokenized real estate — including countries where the framework is already live — the platform comparison on the Tokenizer blog covers the full picture.

Mexico is a $169 billion real estate market with structural demand, international investor appetite, and a government that is — slowly, cautiously — building the regulatory path. The question for anyone holding real assets here is not whether to pay attention, but how early to start preparing.

This article is for informational purposes only and does not constitute legal, tax, or investment advice. Mexican regulations are evolving. Always consult qualified local legal and tax professionals before making structuring decisions.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo