Real Estate Tokenization Regulation: A Country-by-Country Guide

Around the globe, businesses want to digitize property but the first question is almost always legal: “Is it allowed here?” Issuers and investors need clarity on compliance before minting any property token. In this country-by-country guide we…

Around the globe, businesses want to digitize property but the first question is almost always legal: “Is it allowed here?” Issuers and investors need clarity on compliance before minting any property token. In this country-by-country guide we cut through the jargon. We explain how regulators define a “security” for tokenized real estate, then survey key jurisdictions and best‐practice checklists. By the end, you’ll see why regulation is the number-one question for anyone planning a property token offering.

What counts as a “security” in tokenized property

Most jurisdictions treat a token that represents an ownership stake or profit-share in real estate as a regulated security. In the U.S., the SEC says tokenized real estate “are still securities” under existing law. In practice that means if investors pay money in a common project and expect profits (the Howey Test), registration or an exemption is needed. Europe takes a similar view: under EU rules MiCA (Markets in Crypto-Assets, effective 2024) explicitly excludes regulated assets like securities, so tokenized shares or bonds fall under traditional securities rules (MiFID/MiFIR). In other words, most countries apply “same activity, same risk” – if a token looks and acts like an investment contract, it’s treated as one. Emerging markets (China, India, Brazil) are generally even more cautious, often banning unregulated crypto products altogether. In short, any real-estate token carrying equity or revenue rights will usually be classified and regulated as a security.

UAE (Dubai)

Dubai is among the most proactive regulators for property tokens. The Dubai Land Department (DLD) launched a government-backed pilot (REES initiative) to tokenize real estate and enable fractional ownership. This made DLD “the first real estate registration entity in the Middle East to adopt blockchain-based tokenization”. Meanwhile, Dubai’s Virtual Assets Regulatory Authority (VARA) in May 2025 formally updated its Rulebook to cover tokenized real-world assets (including property) under a new Asset-Referenced Virtual Assets (ARVA) category. Together, DLD’s pilot and VARA’s rules mean Dubai now has a clear license framework: issuers must partner with a VARA-licensed token platform and comply with KYC/AML, while property titles remain registered on-chain via DLD. (See our article on Dubai real-estate token rules for details.)

United States

The US treats property tokens as securities governed by the 1933 Securities Act and 1934 Exchange Act. Absent specific crypto guidance, token issuers follow standard exemptions. In practice most real-estate token deals are structured under Regulation D or A. For example, a Regulation D §506(c) private placement lets issuers broadly market to accredited investors only. Issuers must verify investor accreditation but face no limit on amount raised. For larger or public deals, Regulation A+ (“mini-IPO”) permits raising up to $75 million from anyone; tokens can be freely traded from day one on regulated Alternative Trading Systems. (There’s also Reg S for offshore non-US investors, and Reg CF for small $5m crowdsales.) In all cases, issuers must file the proper SEC notices and meet state/federal securities laws. In short, U.S. property token offerings require classic securities compliance (e.g. accredited investor checks, disclosures, issuer registration or exemption filings). (See Tokenizer Estate’s U.S. guide on Reg D/A+ and KYC for more.)

European Union

In the EU, the new MiCA regime (2024–25) regulates crypto-assets but explicitly carves out assets that qualify as “financial instruments”. Tokenized equity or debt in real estate will generally fall under MiFID II/MiFIR rather than MiCA. In other words, EU member-states treat property tokens as securities and apply existing securities laws. Some national regulators are clarifying the picture: e.g. Germany’s BaFin has confirmed that tokenized participations or bonds count as securities subject to the EU Prospectus Regulation, allowing issuers to passport a prospectus across the EU. France has an optional “visa” scheme (via the AMF) for token offers, and a licensing regime for virtual asset service providers. Many EU countries also run sandboxes for blockchain pilots (Germany’s BaFin sandbox, AMF and ACPR sandboxes in France, Luxembourg’s CSSF sandbox). In practice, a token issuer in the EU usually needs either a licensed securities distributor or a crypto-asset services license (CASP) under MiCA, plus full KYC/AML, and to publish a prospectus if selling to the public. (See our discussion of the Portugal tiny-home case for a European example.)

To navigate this complex patchwork of EU-wide and national rules, legally sound models are emerging in specific jurisdictions, marking a significant step toward global adoption..

For example, the company Blocksquare in Luxembourg has developed a framework that fully complies with the new European legislation, MiCAR. Their model is based not on the tokenization of direct property rights, but on economic rights to the income from a property.

This structure includes integration with the state land registry and the notarization of transactions, which provides investors with legally secured rights to a share of the income from the object. Furthermore, the fact that Blocksquare is a participant in the EU Blockchain Sandbox demonstrates a high level of commitment to compliance and the reliability of their approach.

United Kingdom

The UK follows a hybrid approach. FCA guidance (PS19/22) makes clear that tokens granting rights/obligations like shares or bonds will be regulated as securities. Wallets, exchanges or platforms handling such tokens must therefore be authorized under UK financial laws. The UK has set up a Digital Securities Sandbox (DSS) with the Bank of England (opened Sept 2024) to let firms test token issuance and trading under draft rules. Until new laws arrive (post-Brexit crypto regulation is expected in 2025), real-estate tokens are typically launched through regulated entities (e.g. licensed brokers or platforms) and must comply with UK AML and securities rules. In short, like the EU, Britain treats security tokens as investments; what’s new is FCA’s active encouragement of blockchain trials in safe regulatory playgrounds.

Singapore

Singapore treats tokenized assets firmly as securities under its Securities and Futures Act (SFA). The Monetary Authority of Singapore (MAS) has clarified that any token representing ownership or profit from real estate is a capital markets product. MAS licenses exist to handle issuance and trading: for example, the InvestaX platform is MAS-licensed as a Capital Markets Services (CMS) dealer in securities and as a Recognized Market Operator (RMO). Singapore also runs high-profile sandboxes (Project Guardian, since 2022) and recently announced moving from sandbox to full commercialization of asset tokenization. Locally domiciled vehicles help, too: the Variable Capital Company (VCC) structure and eVCC projects allow Singapore funds to issue tokenized shares onchain. In sum, issuers in Singapore must partner with MAS-licensed intermediaries and meet all CMS licensing, KYC/AML and disclosure requirements.

Hong Kong

Hong Kong is building a tokenized real-world asset regime aimed at professional investors. In 2023 the SFC created a special licensing framework for tokenized funds and securities. Today there are live tokenized private funds in Hong Kong – managed by licensed fund managers – available only to professional (accredited) investors. The SFC has also issued guidance on tokenizing authorized investment products and on crypto asset licensing. Retail offerings are highly restricted. Meanwhile Hong Kong’s overall crypto rules tighten access to exchanges (it recently licensed additional trading platforms). In practice, a real estate token project in Hong Kong would need a licensed manager and trustee, investor accreditation, and full compliance with SFC disclosure rules. In short, Hong Kong lets institutional issuers tokenize, but under strict supervision – “tokenized RWA have a stable regulatory regime”.

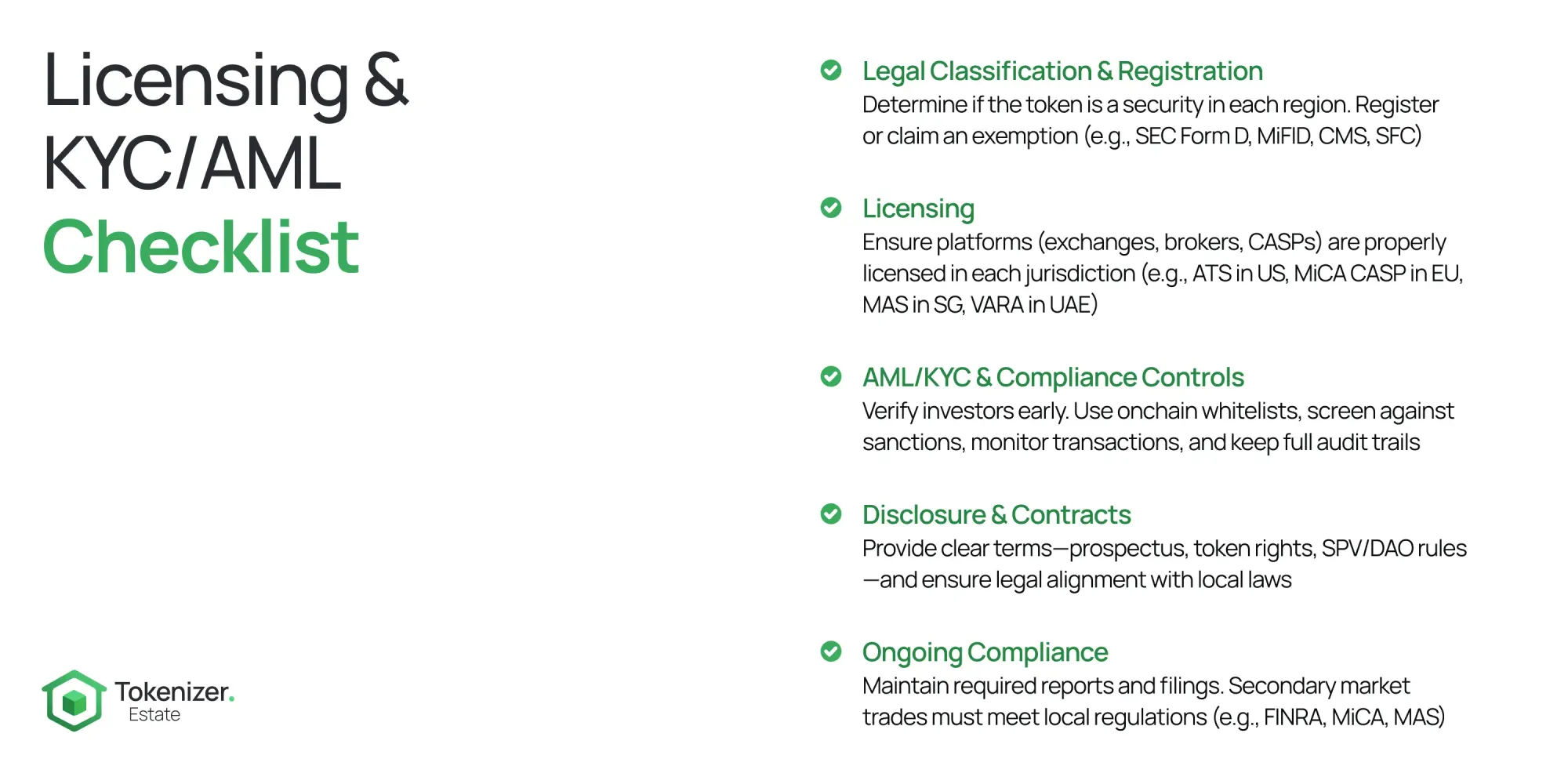

Licensing & KYC/AML Checklist

Regardless of location, token issuers should follow these best practices:

- Legal Classification & Registration: First determine if the token is a security in each target jurisdiction. Register with the securities regulator or use an exemption (for example, SEC Form D filing for a Reg D issue, MiFID prospectus in Europe, CMS license in Singapore, SFC license in HK).

- Licensing: Ensure any exchange, broker, fund manager or CASP handling the tokens is fully licensed locally. For instance, US issuers might use a broker-dealer or ATS; EU issuers might use a MiFID firm or MiCA-licensed CASP; Singapore issuers use MAS-licensed CMS/RMO; UAE issuers use a VARA-licensed platform.

- AML/KYC & Compliance Controls: Implement rigorous investor verification. Good practice is to perform “KYC diligence up front” and whitelist approved investors in the token smart contract. Screen all purchasers against sanctions lists and continuously monitor transactions for red flags. Use permissioned token standards (e.g. ERC-3643) or onchain whitelists so that unverified investors are automatically blocked. Maintain audit trails and filings (e.g. SEC’s Form D or regular reports) as required.

- Disclosure & Contracts: Provide clear offering documents. In many places a prospectus or offering circular will be needed (especially for public sales). All contracts (DAO rules, SPV agreements, transfer restrictions) must align with the jurisdiction’s property and securities laws.

- Ongoing Compliance: After launch, keep up with regulatory filings, reporting and security rules. If tokens trade on secondary markets, ensure the platform is compliant (e.g. CFTC/FINRA rules in US, CASP license in EU, MAS licensing in Singapore). In sum, follow the mantra: know your investor, keep your licensure, and encode compliance in the token.

Future Trends

Global regulators are racing to set common standards. The G20’s Financial Stability Board and IMF have urged member countries to adopt the FSB’s 2023 crypto framework, and in fact 93% of G20 regulators already have crypto-token rules or plans in place. A majority aim to fully align with the FSB’s high-level recommendations by 2025. Likewise, IOSCO (the international securities regulators’ body) has drafted 18 “policy recommendations” in late 2023 to harmonize crypto-asset oversight across borders. Even more broadly, regulators are eyeing tokenization infrastructure: central banks (CBDCs), BIS reports on tokenized cash, and the UK’s new Digital Securities Sandbox all signal token-asset markets are coming under mainstream supervision. In short, expect increasing international coordination (especially via G20/FSB and IOSCO) on asset token standards. Tokenization is moving from an “innovation sandbox” into the regulatory spotlight.

Stay informed.

Subscribe to blog.tokenizer.estate for expert insights, real-world case studies, and the latest updates in real estate tokenization 🏠

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo