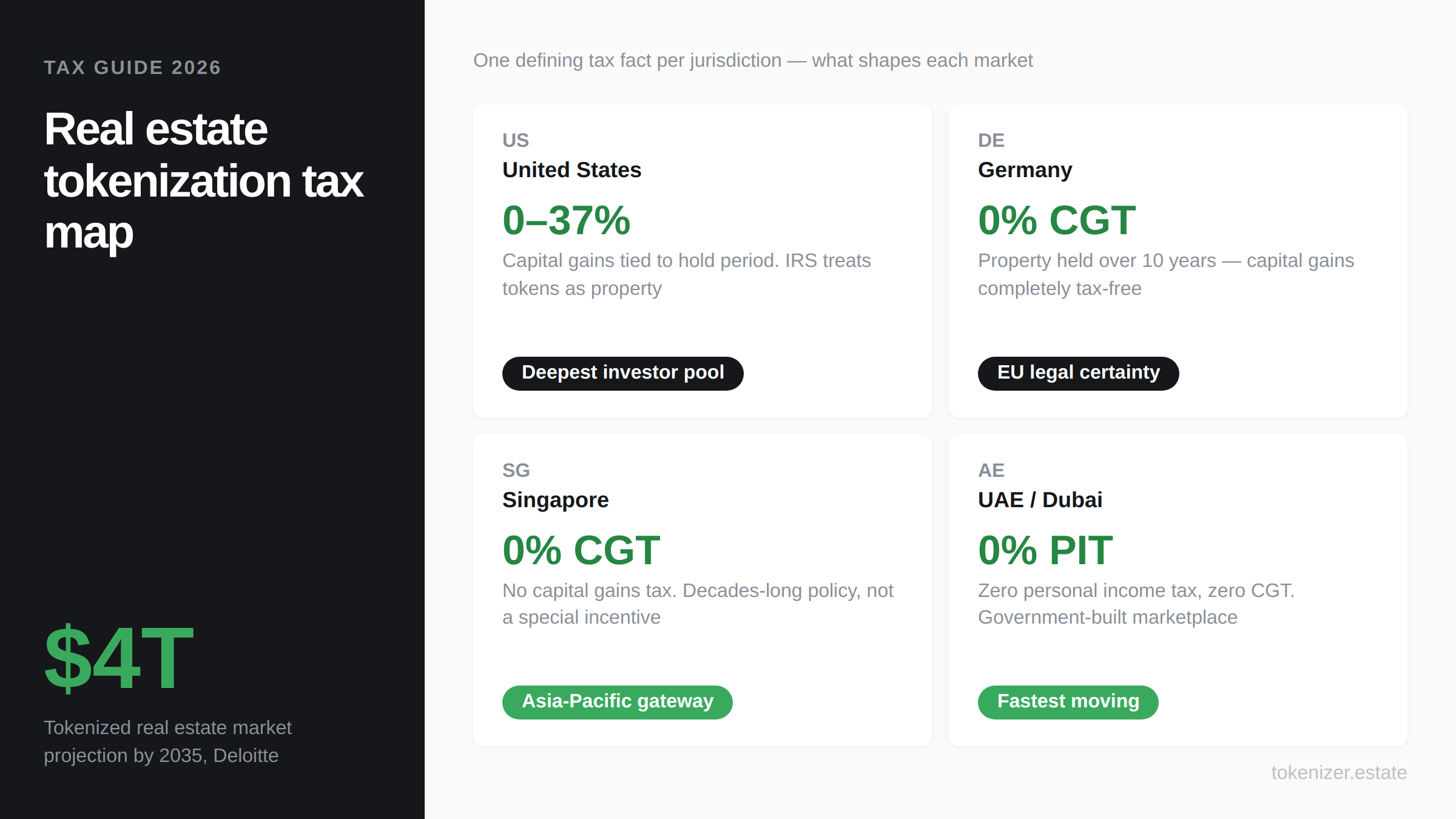

Real Estate Tokenization Tax Guide: US, Germany, Singapore, UAE

You're planning to tokenize a property. Before you move forward, your accountant needs answers: how will this be taxed, and where? This guide covers the US, Germany, Singapore, and UAE — how tokens are classified, how income and gains are taxed, and what the structure actually looks like

Most conversations about real estate tokenization focus on the exciting parts — fractional ownership, global investors, smart contracts, 24/7 liquidity. That stuff is real and it matters. But the question that separates deals that work from deals that fall apart is quieter and less glamorous: how is this taxed, and where?

We cover the four jurisdictions where most of the real action is happening right now: the United States, Germany, Singapore, and the UAE. For each one, we answer the same practical questions: how are tokens classified? How is income taxed? How are gains taxed? What does the structure actually look like?

Why Tax Is the First Conversation, Not the Last

Here is something that happens more often than people admit. A developer tokenizes a €40M logistics park in Hamburg. He raises capital from investors in the Netherlands, Hong Kong, and the US. Rental income flows through a smart contract every month. Eighteen months in, a Dutch investor sells his tokens at a profit on a secondary platform.

And then someone asks: does that gain trigger German real estate transfer tax? Is the Dutch investor liable in Germany, the Netherlands, or both? Was the rental income properly withheld?

None of these are hypothetical questions. They are the exact questions that German tax authorities — and their counterparts in every other jurisdiction — will eventually ask. The structure that worked beautifully in the pitch deck starts to show cracks.

Whether the asset is a commercial building, a resort, a yacht, a factory, or a portfolio of properties — the tokenization map is largely the same. The technology does not change the underlying tax reality. It just adds new layers of complexity on top of it.

The good news: all four jurisdictions covered here have developed clear enough frameworks that you can structure properly — if you do it at the beginning. Deloitte predicts that tokenized real estate will grow from under $0.3 trillion in 2024 to over $4 trillion by 2035, a CAGR of 27%. That kind of growth does not happen without tax and legal clarity. The infrastructure is forming. And the early movers who structure correctly are the ones capturing the best deals.

United States: The Deepest Market, the Most Layers

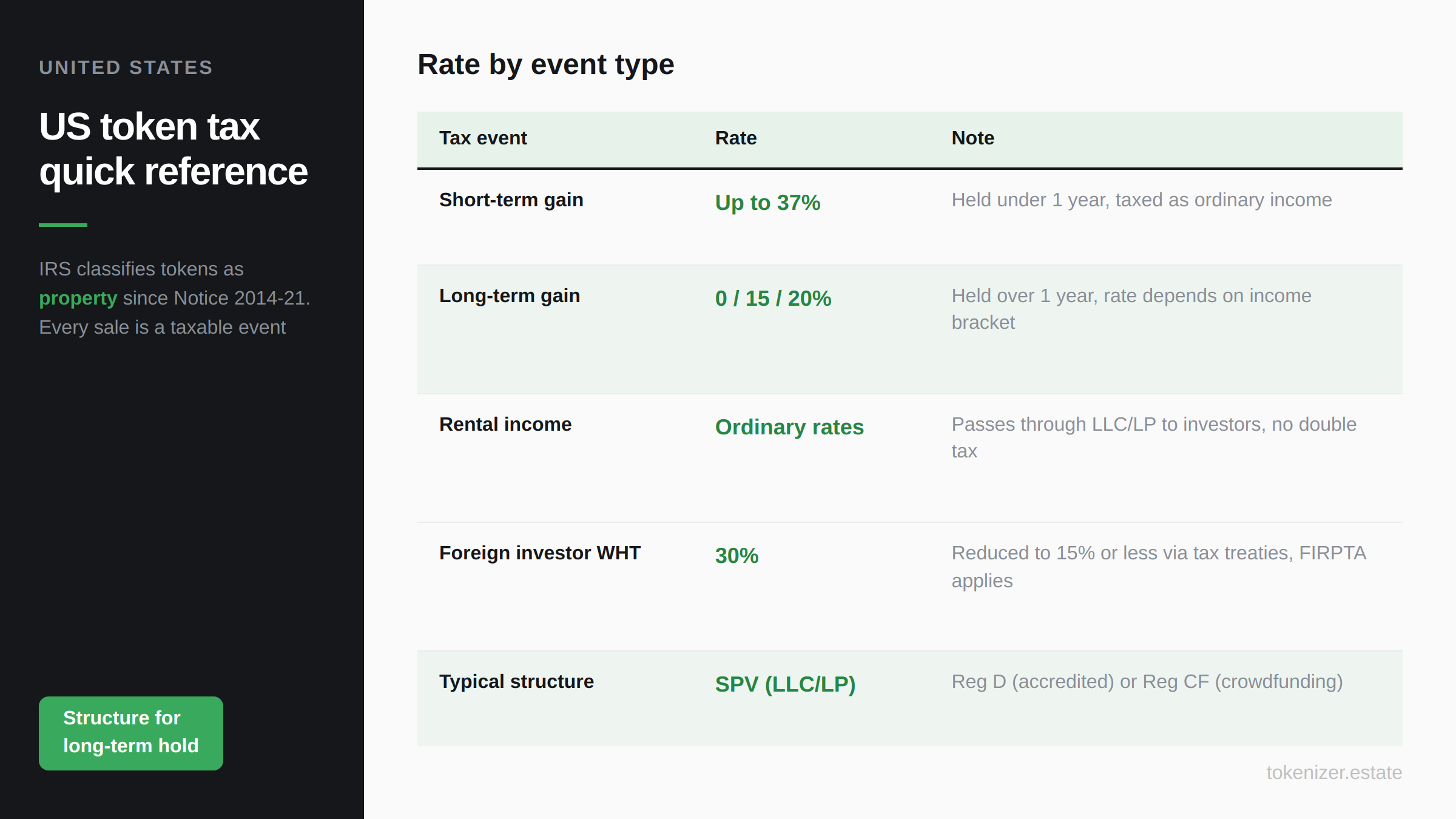

How does the IRS classify real estate tokens?

The IRS made its position clear in 2014 and has not moved from it since: digital assets are property. Not currency, not securities in the traditional sense — property. That one classification has enormous practical consequences for anyone issuing or holding tokenized real estate in the US.

When you sell a token, you are selling property. Capital gains tax applies. Short-term (held under one year) — taxed at ordinary income rates, up to 37% for high earners. Long-term (held over one year) — taxed at 0%, 15%, or 20%, depending on the investor's income level. Most serious real estate tokenization projects in the US are structured specifically to optimize for long-term capital gains treatment.

Rental income distributed through smart contracts is ordinary income. If the deal is structured as an LLC or LP — which is the standard approach — that income passes through to investors and is taxed at the individual level. No corporate double-taxation. This is the main reason US tokenization deals almost universally use an SPV.

What does a real structure actually look like?

Think of the Aspen Digital deal — one of the first landmark US tokenizations. A $18M luxury resort in Colorado, tokenized as a US REIT. Each token represented a share in that REIT, which owned 18.9% of the property. The structure married traditional real estate tax benefits (depreciation, pass-through income) with blockchain delivery. Investors got the familiar tax wrapper. The developer got global capital access.

Most US deals follow this logic: put the asset into an SPV (LLC or LP), issue tokens as membership interests or limited partnership interests, stay within SEC Regulation D (accredited investors) or Regulation CF (crowdfunding). Each path has different investor caps and reporting requirements, but the tax logic is consistent.

What about non-US investors?

This is where it gets genuinely complicated. A German or Singapore-based investor receiving rental income from a US property typically faces 30% withholding tax — reduced by tax treaty to 15% or less in many cases, but still a real cost. Cross-border transactions in tokenized real estate require careful navigation of withholding obligations, treaty benefits, and FIRPTA rules (which govern foreign investment in US real property).

For developers targeting international capital, this means the offering documents need to account for investor tax treatment from day one. It is not a back-office issue — it affects who buys and at what price.

The US offers the largest investor pool in the world. That advantage is real and hard to replicate. But the legal and tax overhead is also the highest of any jurisdiction here. You need a securities attorney, a tax advisor familiar with digital assets, and a compliance team. The deals that work in the US are structured, not improvised.

Germany: Strict on the Surface, Surprisingly Smart Underneath

Why does Germany actually matter for tokenization?

Germany is not the first name people mention when they think of innovation. But for tokenized real estate specifically, it is one of the most structurally sound jurisdictions in Europe — and for long-term asset owners, the tax outcomes are better than almost anywhere else.

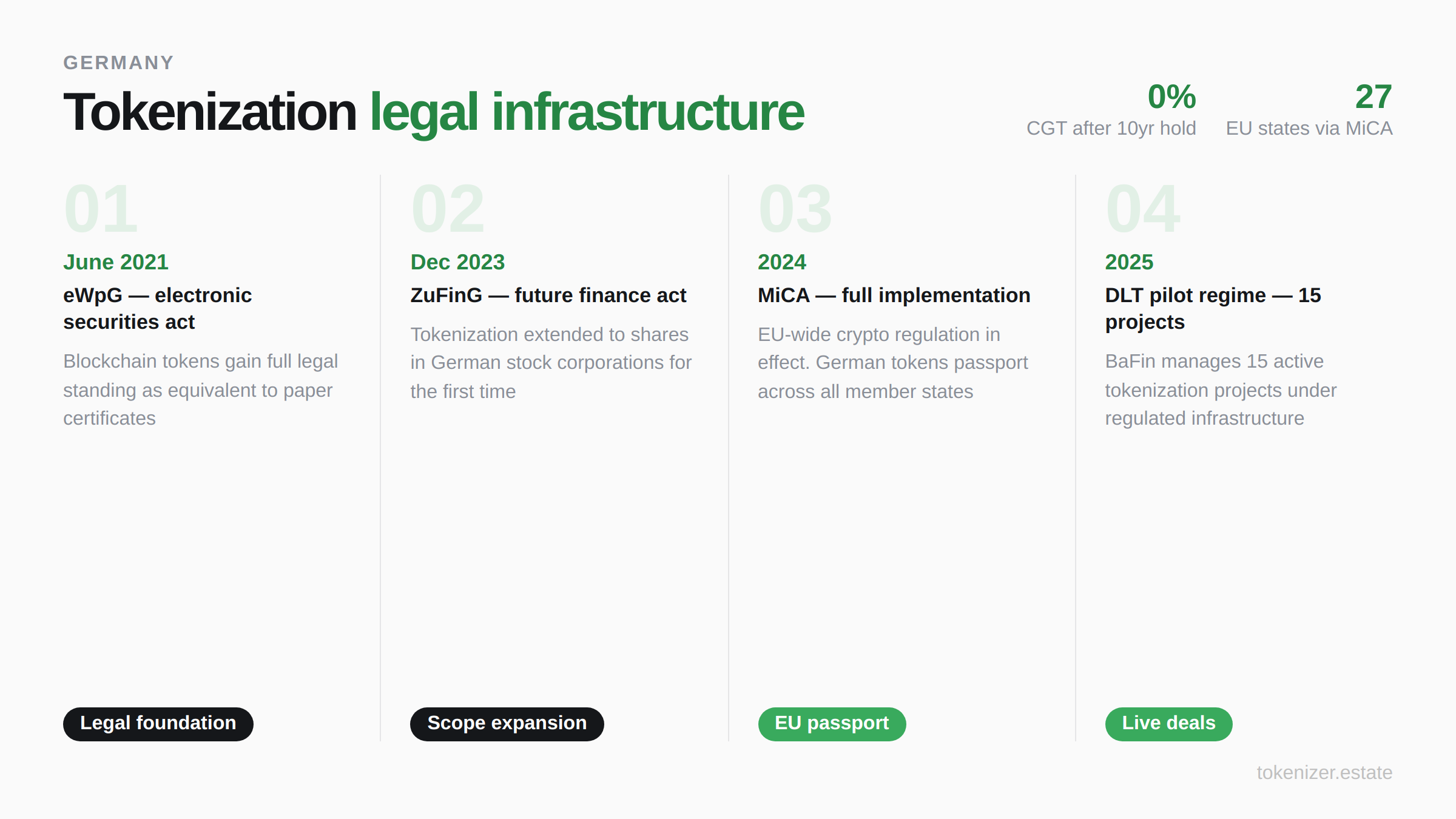

The legal foundation is the eWpG — the Electronic Securities Act, which came into force in June 2021. Before eWpG, German law required physical certificates for certain financial instruments. Blockchain tokens simply had no legal standing. The eWpG changed everything: it explicitly recognized electronic securities registered on a digital ledger as legally equivalent to paper instruments.

In the EU, if a token qualifies as a transferable security under MiFID II, it falls under the full framework of EU financial services law — the same rules that apply to traditional stocks and bonds. In Germany, this means BaFin oversight, proper prospectus requirements, and investor protections. It sounds like burden. What it actually is: credibility that institutional investors in Europe will pay a premium for.

In December 2023, the ZuFinG (Future Finance Act) extended the framework further, allowing tokenization of shares in German stock corporations for the first time. Germany is also participating in the EU's DLT Pilot Regime — by 2025, BaFin manages 15 active projects under this initiative.

What does the German tax picture actually look like?

Here is where Germany surprises people. Two scenarios:

Bonds and debt tokens. Most German tokenized real estate projects use tokenized bonds (Schuldverschreibungen) issued under the eWpG framework. Investors receive coupon payments taxed as capital income at a flat 25% plus solidarity surcharge (roughly 26.4% total). This is lower than the top German income tax rate of 45%. For European family office investors, this is a clean, predictable structure.

Direct property interest. Germany has a famous rule: capital gains on real property held for more than 10 years are completely tax-free. This applies to the underlying asset. Whether it passes through to token holders depends on the structure — but for long-term asset owners and operators, it creates powerful incentive to structure accordingly.

What does a real deal look like?

The Hamburg logistics park example is not hypothetical. German platforms like Exporo and Bergfürst have tokenized dozens of properties — from residential complexes in Leipzig to commercial assets in Frankfurt — using BaFin-approved prospectuses and the eWpG bond structure. A typical deal: €5M to €40M in issuance, minimum investment €500–€1,000, bond coupon of 5–7%, 3–5 year term.

For a marina operator or industrial park owner in Europe, Germany offers something valuable: a legal framework that European investors recognize, MiCA compliance (EU's crypto regulation now in full effect), and tax treatment that rewards long-term structures. It is the right jurisdiction for developers who want EU institutional capital and are willing to do the compliance work properly.

For a deeper look at how Germany fits into the European regulatory landscape, this country-by-country regulation guide from the Tokenizer blog is worth reading in full.

Singapore: Where Zero Capital Gains Meets Institutional Credibility

Is Singapore really as good as it sounds for tokenization?

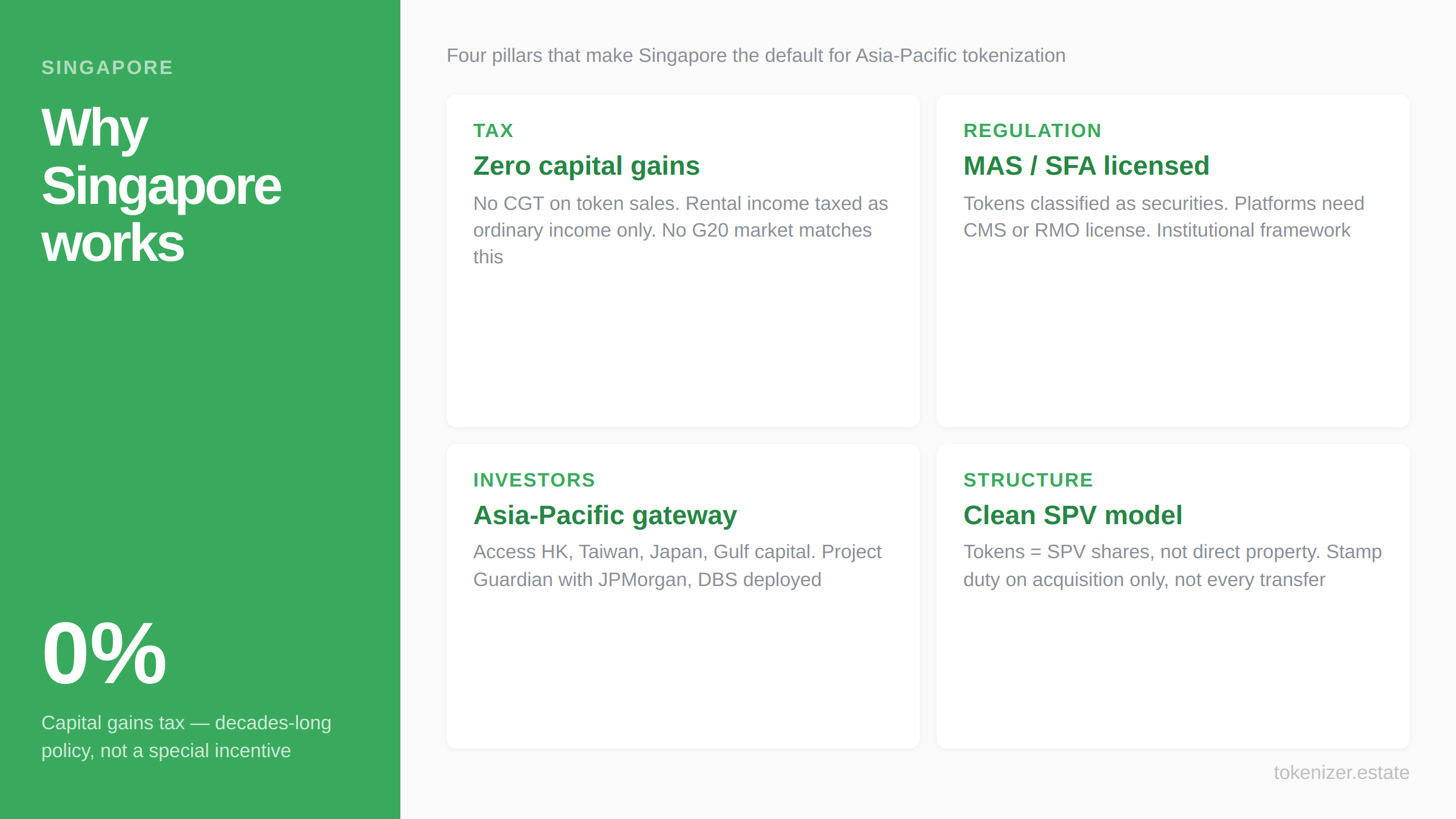

Yes — with nuance. Singapore has no capital gains tax. That is not a special blockchain rule or a temporary incentive. It is how Singapore has operated for decades, and it applies to tokenized real estate in exactly the same way it applies to stocks, traditional property, and other investment assets.

Sell a token at a profit. No capital gains tax. Full stop.

Rental income and distributions to token holders are taxable as ordinary income. But for investors primarily motivated by appreciation in the underlying asset — commercial buildings in Singapore's CBD, data centers in Jurong, hospitality assets across Southeast Asia — the capital gains treatment is a structural advantage that no other developed G20 market offers.

How does MAS actually regulate tokenized real estate?

The Monetary Authority of Singapore (MAS) treats real estate tokens as securities under the Securities and Futures Act (SFA), since they exhibit the characteristics of traditional investment instruments. This means real estate tokens are not in a regulatory grey zone. They are securities, platforms need proper licensing (Capital Markets Services or Recognized Market Operator), and investor protections apply.

What this does is give institutional investors from Europe, the Middle East, and the US a framework they understand. Singapore's credibility as a financial center is not an accident — it is built on consistent, rigorous regulation. When a Swiss family office or a Korean insurance company evaluates a tokenized Singapore asset, they are not buying into the unknown. They are buying into a licensed, regulated structure.

Project Guardian — MAS's flagship tokenization program — has moved from sandbox to real-world deployment. In 2024, MAS announced the commercialization of asset tokenization, transitioning from pilot trials to institutional-grade implementation with major financial institutions. JPMorgan, DBS, and others are active participants.

What about the stamp duty question?

Singapore charges stamp duty on property transfers. The key structural question for tokenized assets: is a token transfer a property transfer (triggering stamp duty) or a securities transfer (different, generally lighter treatment)?

Most well-structured Singapore tokenization deals answer this by using an SPV to hold the underlying property. Tokens represent shares or interests in the SPV — not direct property interests. Token transfers are therefore securities transfers, not property transfers. Stamp duty on the property itself only applied once, when the SPV acquired it. This is a clean, legally robust approach that Singapore advisors have refined over the past several years.

For developers targeting Asian capital — investors from Hong Kong, Taiwan, Japan, Indonesia, or the Gulf who want Singapore-regulated exposure — this jurisdiction is often the default choice. Singapore and Hong Kong are the leaders in real estate tokenization in the Asia-Pacific region. The infrastructure, the investor base, and the tax environment are all aligned.

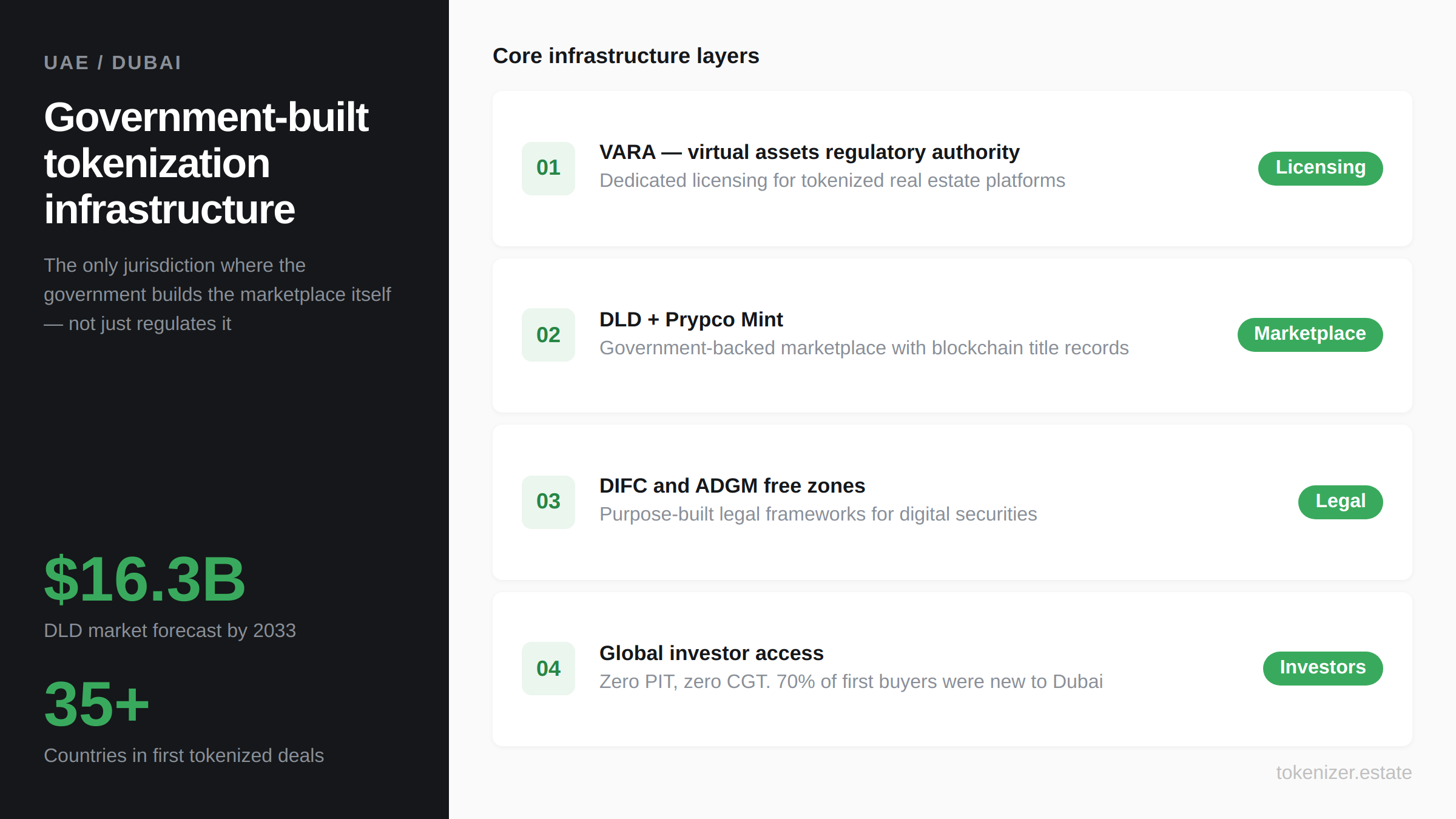

UAE / Dubai: The Boldest Tokenization Experiment in the World

What makes the UAE different from every other jurisdiction?

In every other market covered in this guide, tokenization is something the private sector is doing while regulators try to keep up. In the UAE, the government is building the infrastructure itself — and inviting asset owners to join.

The Dubai Land Department launched Prypco Mint in 2024 — the world's first government-backed tokenized real estate marketplace. The DLD is integrating blockchain directly into official property title records. VARA (Virtual Assets Regulatory Authority) provides licensing for tokenized real estate platforms. The DIFC and ADGM free zones offer purpose-built legal frameworks for digital securities. The Dubai Land Department has forecast the real estate tokenization market to reach $16.3 billion by 2033, representing 7% of Dubai's total real estate transactions.

No other government in the world has committed to tokenization at this level. Not in policy papers — in actual infrastructure.

What is the tax situation?

Personal income tax in the UAE: zero. Capital gains tax: zero. For investors holding tokenized real estate, the after-tax return profile is unmatched by any developed market.

Corporate tax was introduced at 9% in 2023 for businesses earning above AED 375,000. But investment holding structures operating within DIFC or ADGM free zones often qualify for specific exemptions or favorable treatment that significantly reduce or eliminate this liability. Most tokenization deal structures are designed with this in mind from the start.

The open question is VAT. The UAE has a 5% VAT rate. Whether it applies to tokenized real estate depends on classification: traditional property interest (5% on commercial, exempt on residential) or virtual asset (potentially exempt as a financial service). This classification question is actively being worked through by VARA and deal-level legal advisors — and the answer affects structuring. It is not a dealbreaker, but it is a conversation that needs to happen before issuance.

What does a real deal in the UAE look like right now?

In mid-2025, Dubai oversaw the tokenized sale of two luxury residential properties. Both offerings sold out within minutes. Buyers came from over 35 countries. Roughly 70% were first-time investors in Dubai real estate — attracted specifically by the ability to enter a market that had previously been inaccessible to them.

That is the UAE value proposition in a single data point. The government is not just removing barriers — it is actively building the platform that makes global capital flow into Dubai assets. For a developer with a hotel, a marina, or a mixed-use development in the Gulf region, the combination of zero personal tax, government-backed marketplace infrastructure, and institutional licensing through DIFC/ADGM is almost impossible to replicate elsewhere.

Track the latest deal flow and regulatory updates from this market at Tokenizer News, which covers the major developments across all four jurisdictions in real time.

The Honest Comparison: What Actually Matters for Your Decision

Before you choose a jurisdiction — or build a multi-jurisdictional structure — here is what the picture looks like when you put all four side by side:

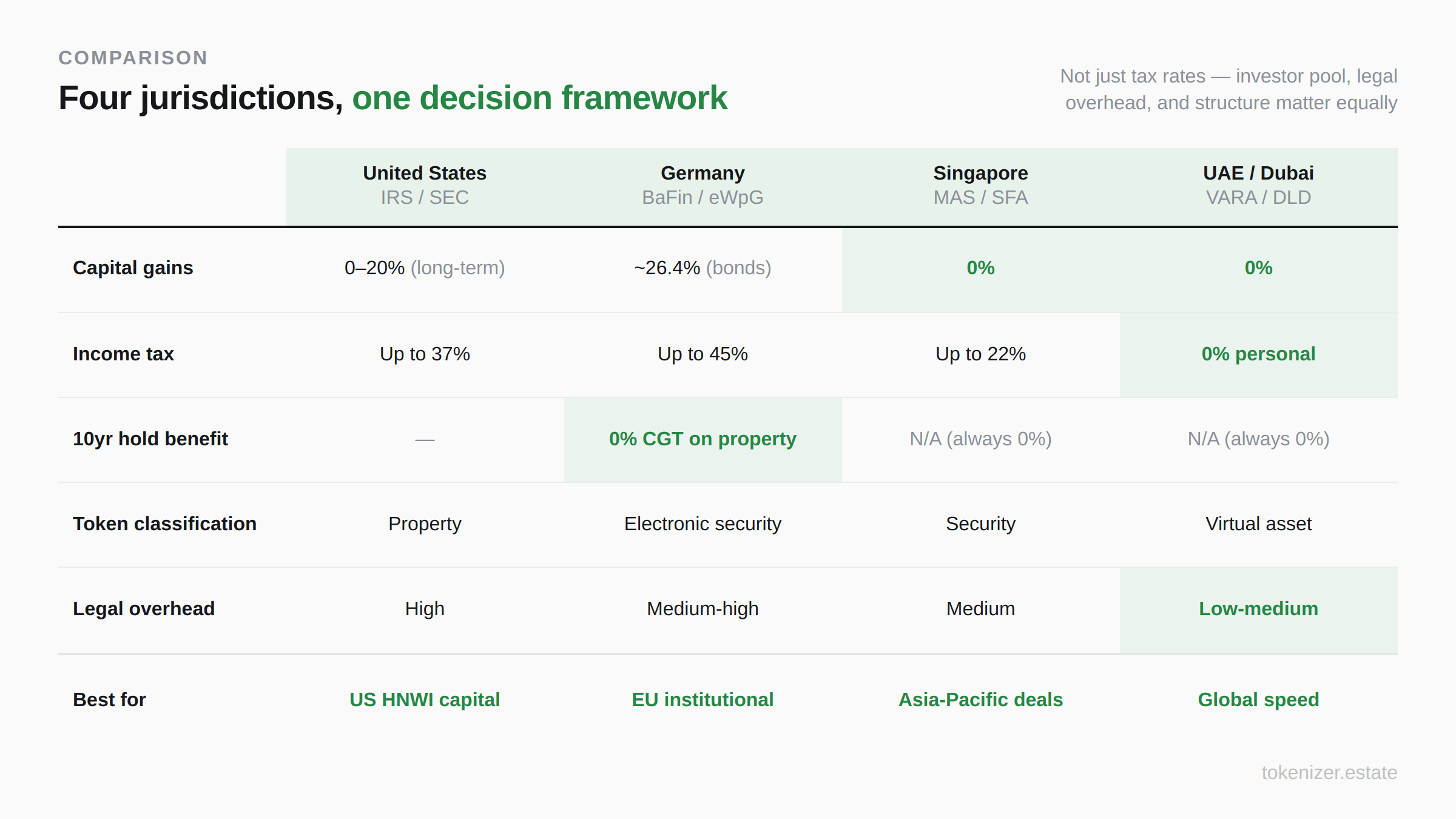

United States — deepest investor pool on earth, highest legal overhead, tokens treated as property under IRS rules. Capital gains rates depend on hold period. Best for US-based assets or developers who specifically need US institutional and HNWI capital. Be prepared for real compliance costs.

Germany — legal certainty through eWpG, EU passport for investors across 27 member states, flat 25% capital income tax on bond structures, potential 0% CGT on long-term property interests. Best for European assets and developers targeting European family offices or institutional capital. Slower, but credible.

Singapore — zero capital gains tax, MAS-regulated credibility, regional gateway to Asian capital, clean SPV structure for stamp duty optimization. Best for Asian assets and developers who want institutional-grade structure without the EU compliance overhead. Excellent for international investor diversity.

UAE — zero personal income tax, zero CGT, government-built marketplace, VARA licensing, DIFC/ADGM legal frameworks, fastest-moving regulatory environment in the world. Best for Gulf assets, international capital raises, and developers who want maximum operational speed and investor accessibility.

The choice is not only about tax rates. It is about where your investors are located, where your asset sits legally, and what structure gives you the most flexibility as this market matures over the next five years. The most sophisticated deals today use a multi-jurisdiction approach: the asset in one country, the issuance vehicle in another, secondary market access through a third.

What all four jurisdictions agree on: the tax conversation must happen at the beginning, not after the smart contract is deployed.

One Thing That Every Asset Owner in This Space Needs to Understand

Real estate tokenization tax treatment is still evolving everywhere. The IRS has issued limited specific guidance on tokenized securities (as opposed to cryptocurrencies). Germany's eWpG scope will expand. Singapore is still refining stamp duty treatment for digital asset transfers. The UAE is actively finalizing VAT classification for virtual assets.

This means two things practically.

First, the "optimal structure" of today may shift in 12 to 18 months. Work with advisors who are specifically active in this space and track regulatory developments, not just generalists who have read a few articles.

Second — and this is the more important point — the window for early movers is real. According to Deloitte, tokenized real estate is expected to grow from less than $0.3 trillion in 2024 to over $4 trillion by 2035. The developers, asset owners, and fund managers who build proper tokenization structures now — legal, tax, and technical — are establishing relationships with a global investor base that their competitors are not even in conversation with yet.

If you own a hotel portfolio, a logistics network, a marina, or a commercial property portfolio and you are reading this — you are not too early. The infrastructure exists. The licensing exists. The investors exist. The question is whether your asset and your structure are ready to meet them.

You can get a detailed picture of how the market infrastructure actually fits together — issuance platforms, custody, legal wrappers, secondary markets — in this 2026 Real Estate Tokenization Market Map from the Tokenizer blog. It maps the full ecosystem across all four jurisdictions and is the most comprehensive overview of who does what available right now.

The deals are getting done. The capital is moving. The only remaining question is whether you are on the right side of that flow — or watching from the outside.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo