Tokenization beyond real estate: yachts, factories, and industrial assets go on-chain

A $50 million superyacht sits idle 325 days a year. Tokenization lets the owner sell 30% to 200 investors and unlock $15 million — without selling the yacht. The same model works for factories, fleets, energy assets, and marinas. This is the practical guide to non-real-estate tokenization.

A $50 million superyacht sits in a marina in Monaco. It sails maybe 40 days a year. The other 325 days, it burns through crew salaries, docking fees, insurance, and maintenance — roughly $5 to $7.5 million annually — while producing zero income. The owner wants liquidity but does not want to sell. The yacht market is slow, brokers take months, and buyers want discounts.

Now imagine the same yacht, tokenized. The owner sells 30% through digital securities to 200 investors. Those investors receive a share of charter revenue when the yacht is rented. The owner keeps 70%, keeps using the yacht, and unlocks $15 million in capital without selling a single rope.

This is already happening. Superyachts are being fractionally sold through blockchain-based platforms. Yacht builders are accepting crypto payments and offering tokenization on new builds. Token holders are booking sailing time and earning yield from charter pools — all managed by smart contracts.

And yachts are just the beginning.

The same structure that tokenizes a building — SPV, security token, KYC/AML compliance, automated dividends — works for any income-producing or high-value physical asset. Factories. Logistics fleets. Mining equipment. Agricultural machinery. Energy infrastructure. Marinas. Aircraft. If it has value and generates cash flow, it can be tokenized.

This article covers what is happening beyond real estate, why it matters for asset owners, and where the real opportunities are in 2026.

Why tokenization is not a real estate story anymore

Most people hear "tokenization" and think "buildings." That made sense in 2020, when St. Regis Aspen and a few residential projects were the only live deals. But by 2026, the picture has changed.

On-chain real-world assets have crossed $26 billion in value. Tokenized US Treasuries alone account for $8.7 billion. The Motley Fool reports that McKinsey projects the RWA tokenization market could reach $2 trillion by 2030. That estimate spans far beyond property. Equities, bonds, commodities, private credit, and physical assets of all kinds are moving on-chain.

The logic is simple. Tokenization solves three problems that exist in every illiquid asset class — real estate included, but far from the only one: capital is locked, ownership is hard to transfer, and the investor pool is artificially small. A factory in Poland has the same liquidity problem as an office building in Manhattan. A fleet of container ships has the same ownership-transfer friction as a hotel in Tulum. The technology does not care what the asset is. It cares about the legal wrapper, the cash flow, and the compliance structure.

For decision-makers who own assets beyond buildings — fleet operators, industrial manufacturers, marina owners, energy companies, mining operators — this means the tool is ready. The question is whether the asset fits.

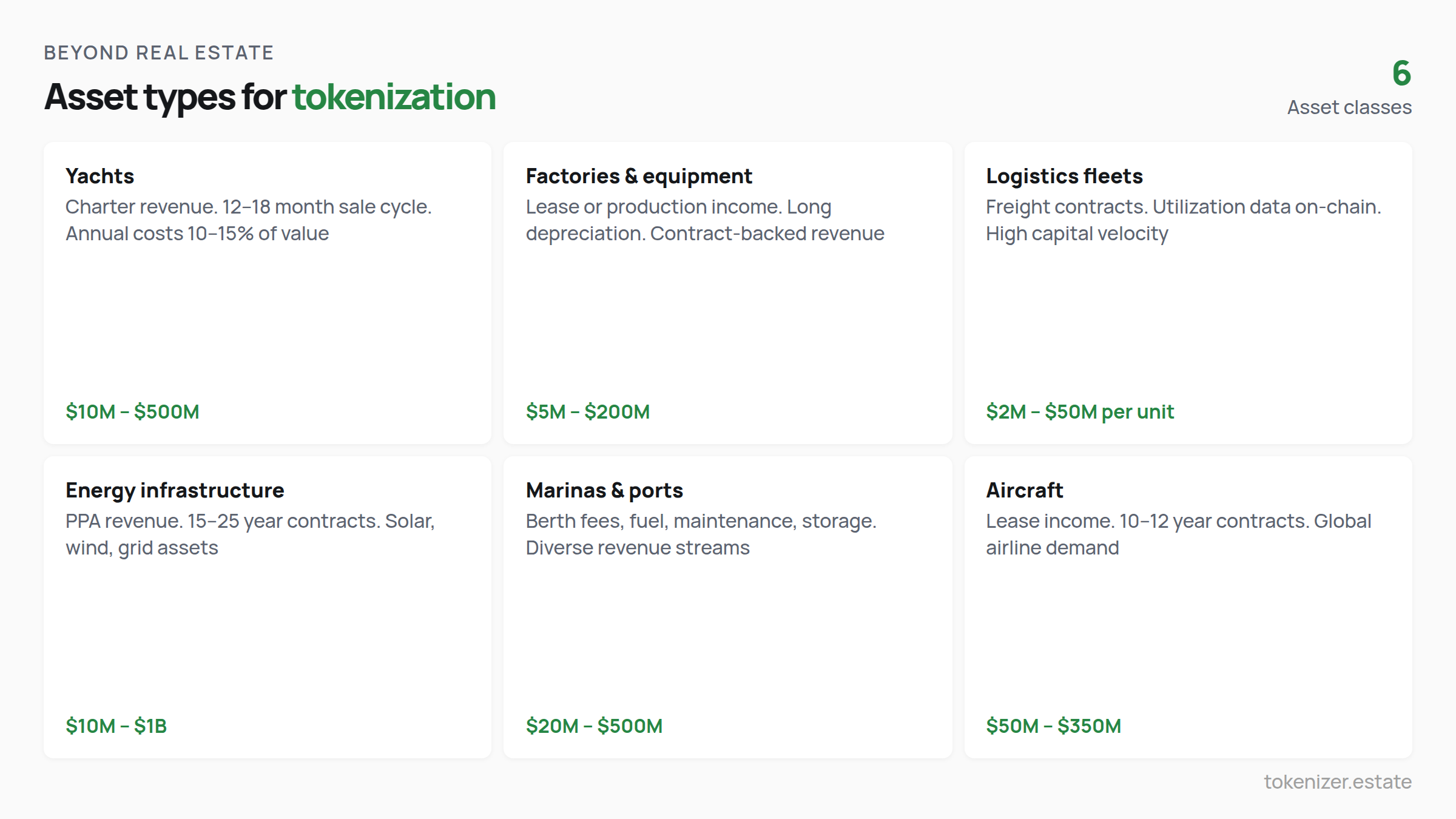

Yachts: the most visible non-RE tokenization

Superyachts are the poster child for non-real-estate tokenization, and for good reason. They are expensive ($10 million to $500 million), depreciating, and extremely illiquid. The average time to sell a yacht is 12 to 18 months. Annual operating costs run 10–15% of the vessel's value. Most yachts sit idle 90% of the year.

Tokenization flips the economics. Instead of one owner bearing 100% of costs, fractional owners share the burden. Charter revenue — which can reach $500,000 per week for a large superyacht — flows through the smart contract and gets distributed to token holders proportionally.

Quantum Luxury Yacht Ownership created what they call a "crypto yacht exchange" — a multi-currency platform where owners and shipyards tokenize superyachts for sole or co-ownership. The yacht sits inside a company (SPV), and tokens represent shares in that company. Buyers go through a vetting process. The blockchain handles the cap table, the transfers, and the distributions.

Investing Yachts takes a different approach: a fleet model. Their $YATE token represents a proportional stake across a portfolio of charter yachts. Holders earn up to 65% of net charter profits distributed annually, with a deflationary buyback mechanism that burns tokens over time.

Mustaa, built on LUKSO, focuses on access rather than pure ownership. Token holders get guaranteed yacht time — one week in peak season or two in shoulder season — and can rent unused slots to others for yield. The team includes a Feadship veteran and a serial tech entrepreneur.

What makes yacht tokenization work: clear ownership structure (SPV holds the vessel), measurable revenue stream (charter income), global demand for the asset (tourism and leisure), and a buyer pool that already thinks in terms of fractional access (yacht clubs and charter companies have been doing shared models for decades — blockchain just makes it liquid and transparent).

Factories and industrial equipment: the quiet opportunity

Nobody writes articles about tokenizing a packaging plant in Brno or a CNC machining center in Guadalajara. But the economics work. And for a very specific reason.

Industrial assets generate predictable, contract-based revenue. A factory with five-year production contracts and three corporate clients has cash flow that is often more stable than a hotel. The equipment has a known depreciation schedule. The operating costs are measurable. And the capital locked in the asset is significant — a mid-size manufacturing facility can be worth $20 million to $200 million, with most of that capital inaccessible to the owner.

Tokenization lets the factory owner raise capital against the asset without selling it and without a bank lien. The structure is identical to real estate tokenization: the factory (or the equipment inside it) sits inside an SPV, tokens represent shares in the SPV, and cash flow from production contracts or equipment leases gets distributed to token holders.

The BDO report on tokenization trends for 2026 notes that private equity fund managers are already using tokenization to facilitate cheaper deals and expand investor access. Industrial assets — factories, warehouses, production lines, specialized equipment — are a natural extension. The challenge: unlike real estate, industrial assets depreciate. A building might appreciate over 20 years. A CNC machine loses value every year. Tokenization deals for industrial equipment need to account for this through higher initial yields, shorter time horizons, or residual value guarantees.

For the decision-maker who owns industrial operations — whether that is a food processing plant, a textile factory, an auto parts manufacturer, or a steel mill — the question is straightforward: do you have a contract-backed revenue stream, and is your capital locked? If both answers are yes, the asset can be tokenized using the same infrastructure that handles commercial buildings.

Logistics fleets, shipping, and transport

A container ship costs $150 million to $200 million. A fleet of 50 long-haul trucks costs $7.5 million. A regional airline's narrow-body aircraft costs $50 million to $120 million. These are capital-intensive assets with long useful lives and measurable utilization data.

The maritime industry has been exploring tokenization for several years. Vessel ownership has traditionally been structured through SPVs (one company per ship), which makes the transition to tokenized ownership structurally simple. The SPV already exists. The token replaces the paper share certificate.

Aircraft leasing is another natural fit. The global aircraft leasing market is worth over $300 billion. Lessors buy aircraft and lease them to airlines on 10–12 year contracts. The income is predictable, the tenants are known, and the asset has global mobility. Tokenizing a share of an aircraft lease portfolio gives investors access to aviation-grade yields without buying a plane.

For fleet operators in trucking, rail, or maritime, the value proposition is about capital velocity. Instead of waiting for a bank to approve a fleet expansion loan, you tokenize 20% of your existing fleet, raise capital from 150 investors globally, and use the funds to buy more vehicles. The existing fleet's freight contracts back the tokens. The new vehicles generate additional revenue. The flywheel turns faster.

Energy infrastructure: solar farms, wind, and beyond

Renewable energy is one of the most discussed applications for non-RE tokenization. A solar farm generates predictable income from Power Purchase Agreements (PPAs) — often 15 to 25 year contracts with utilities or corporations. The revenue is measurable, the counterparty risk is known, and the asset has a long useful life.

The challenge — as the Tokenizer.Estate energy sector analysis detailed — is operational complexity. Energy assets require servicing, metering, maintenance, and regulatory compliance that is more complex than collecting rent. The token can represent a claim, but enforcing that claim when something goes wrong (a panel breaks, a utility disputes a payment, a permit expires) still sits in the off-chain world.

That said, several projects are operational. Tokenized solar funds exist in Europe and the US. Carbon credit tokenization is growing — blockchain adds traceability to credits that have historically suffered from double-counting and fraud. And infrastructure assets like toll roads and bridges are being explored as tokenization candidates because of their long-term, contract-backed revenue.

Marinas, ports, and waterfront assets

Marinas are an interesting hybrid: part real estate (the physical berths and buildings), part service business (fuel, maintenance, storage, provisioning), and part lifestyle asset (members and tenants pay for location, access, and community). A marina in the Mediterranean can be worth $20 million to $500 million depending on location and capacity.

For marina owners, tokenization offers a way to unlock capital from an asset that is hard to mortgage (banks struggle with marina valuations) and hard to sell (the buyer pool is tiny). The revenue streams are diverse — berth fees, fuel sales, maintenance services, winter storage, boat sales commissions — which actually makes the token more attractive to investors than a single-tenant commercial property.

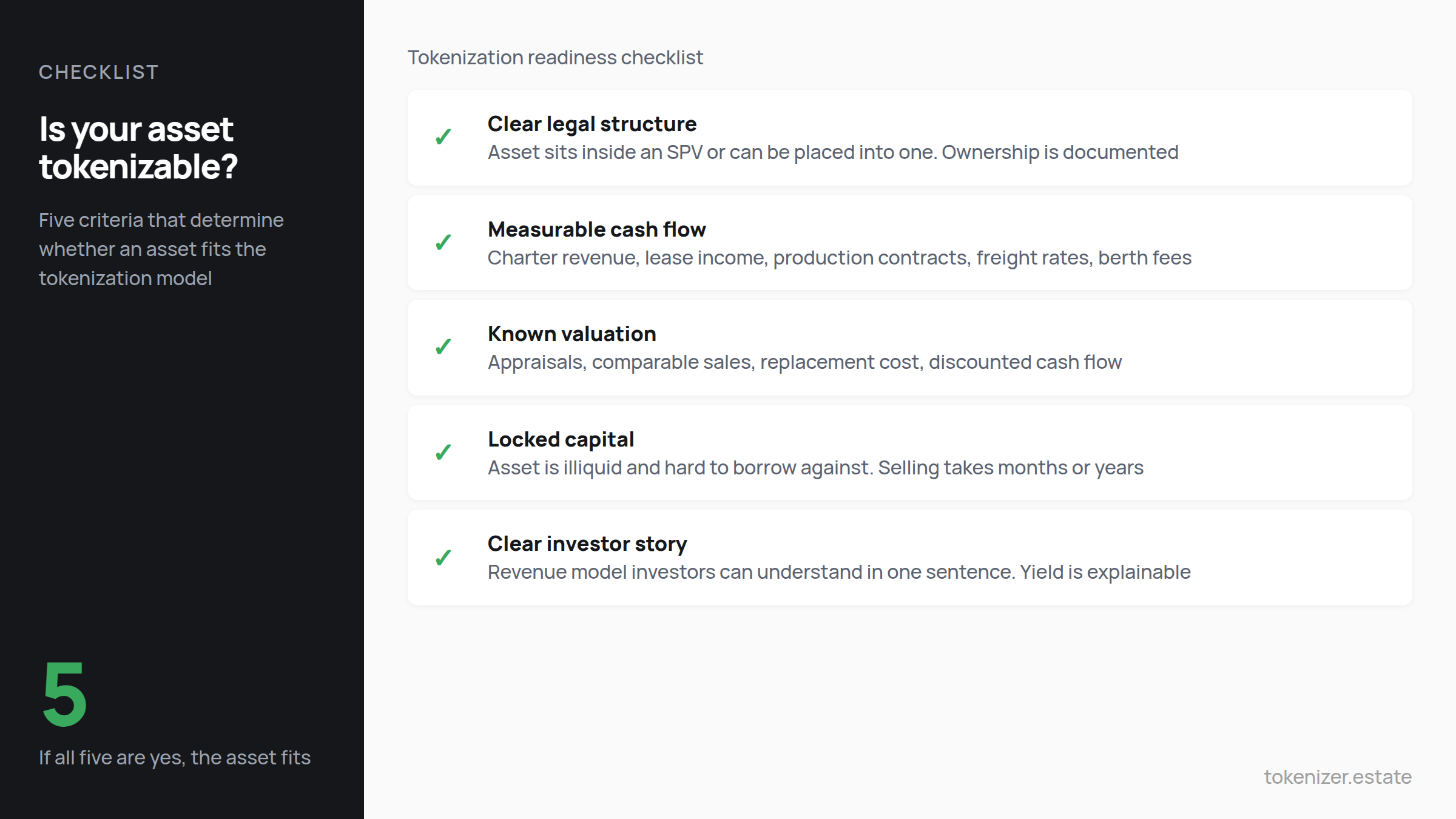

What makes a non-RE asset tokenizable

After looking at yachts, factories, fleets, energy, and marinas, here is the pattern. An asset is a good tokenization candidate when:

It has a clear legal structure. The asset sits inside an SPV or can be placed into one. Ownership is documented and enforceable. Title is clean.

It generates measurable cash flow. Charter revenue, lease income, production contracts, freight rates, berth fees, PPAs. The smart contract needs a number to distribute. No revenue, no dividends, no investor interest.

It has a known valuation methodology. Appraisals, comparable sales, replacement cost, discounted cash flow. Investors need to know what the asset is worth. If valuation is speculative, the deal is harder to structure.

The capital is locked. This is the trigger. If you can easily borrow against the asset or sell it quickly, tokenization adds less value. The more illiquid and capital-intensive the asset, the more tokenization helps.

The investor story is clear. "You own a share of a superyacht that charters in the Mediterranean and earns 8% annually" is a story investors understand. "You own a share of a CNC machine in a factory" is harder to sell. Unless the revenue contract behind it is strong.

What this means for your business

If you are reading this article, you probably own or operate more than buildings. Maybe you have a logistics fleet and a warehouse. A hotel and a marina. A factory and an office park. Industrial equipment that generates income but locks your capital.

The technology does not distinguish between these assets. The same smart contract that distributes rent from a tokenized office building can distribute charter revenue from a yacht or lease income from a CNC machine. The same KYC/AML pipeline that verifies a real estate investor verifies an equipment investor. The same secondary market where property tokens trade can trade industrial tokens.

What changes is the legal wrapper (SPV structure varies by asset type and jurisdiction), the valuation approach (buildings appreciate, equipment depreciates), and the investor narrative (everyone understands rent, not everyone understands freight rates).

For a full view of how tokenization platforms, legal structures, and compliance frameworks work across asset types, the market map on the Tokenizer blog covers the ecosystem.

The real opportunity in 2026 is not "tokenize a building." It is "tokenize the balance sheet." Every capital-intensive asset you own — every building, every vehicle, every machine, every vessel — is a candidate. The ones with strong cash flow and clear legal structure go first. The rest follow as the market matures.

Stay current with tokenization developments across all asset classes at Tokenizer.Estate News.

This article is for informational purposes only and does not constitute legal, tax, or investment advice. Tokenization of non-real-estate assets involves specific legal and regulatory considerations that vary by asset type and jurisdiction. Always consult qualified professionals before structuring tokenized offerings.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo