Tokenization in Malta

Tokenization in Malta can improve investor reach and shared recordkeeping, but only if legal classification, the authoritative register, and custody/eligibility operations stay aligned. This article explains what works, what breaks, and how to decide.

You are here because you have a real choice to make, not because you need another “what is tokenization” explainer.

This article looks at Tokenization in Malta as a set of real-world risks, constraints, and trade-offs—so you can make a clean do / don’t / how decision.

If you want a quick refresher on what tokenization means in plain words, you can read overview. For what follows, we will stay focused on Malta-specific reality.

How tokenization works in Malta

Tokenization in Malta is not one single “thing.” In operational terms, it is a way to represent an asset (or a right) as a token on a shared ledger, so the token can be held and transferred across a network. The important point is what the token stands for and where the authoritative record sits.

Tokenization in Malta is the digital representation of an asset or right on a ledger, where token transfers can be recorded on-chain, but legal enforceability still depends on the underlying legal instrument and the official register (if one exists).

This matters once you move from demos to production. The token can move instantly, but your project still needs a clear answer to “who controls the register,” “who can access it,” and “what happens when the chain record and the off-chain record disagree.”

That is why Malta’s own discussion of fund-unit tokenization starts from the transfer agency angle: the share register, not trading hype. If you are tokenizing fund units, the MFSA frames the scope around how units/shares are recorded and maintained, including the difference between models where only the administrator has register access (off-chain) and models where multiple parties can access the network (on-chain). You can review paper if your use case touches funds.

There is also a quiet upside here, if you design it honestly: on-chain models can support wider investor reach because holding and transferring a token can be done across a network, not inside one closed administrator database. But that “reach” is real only when eligibility and distribution rules are built into the operating model, not bolted on later.

Tokenization in Malta regulation

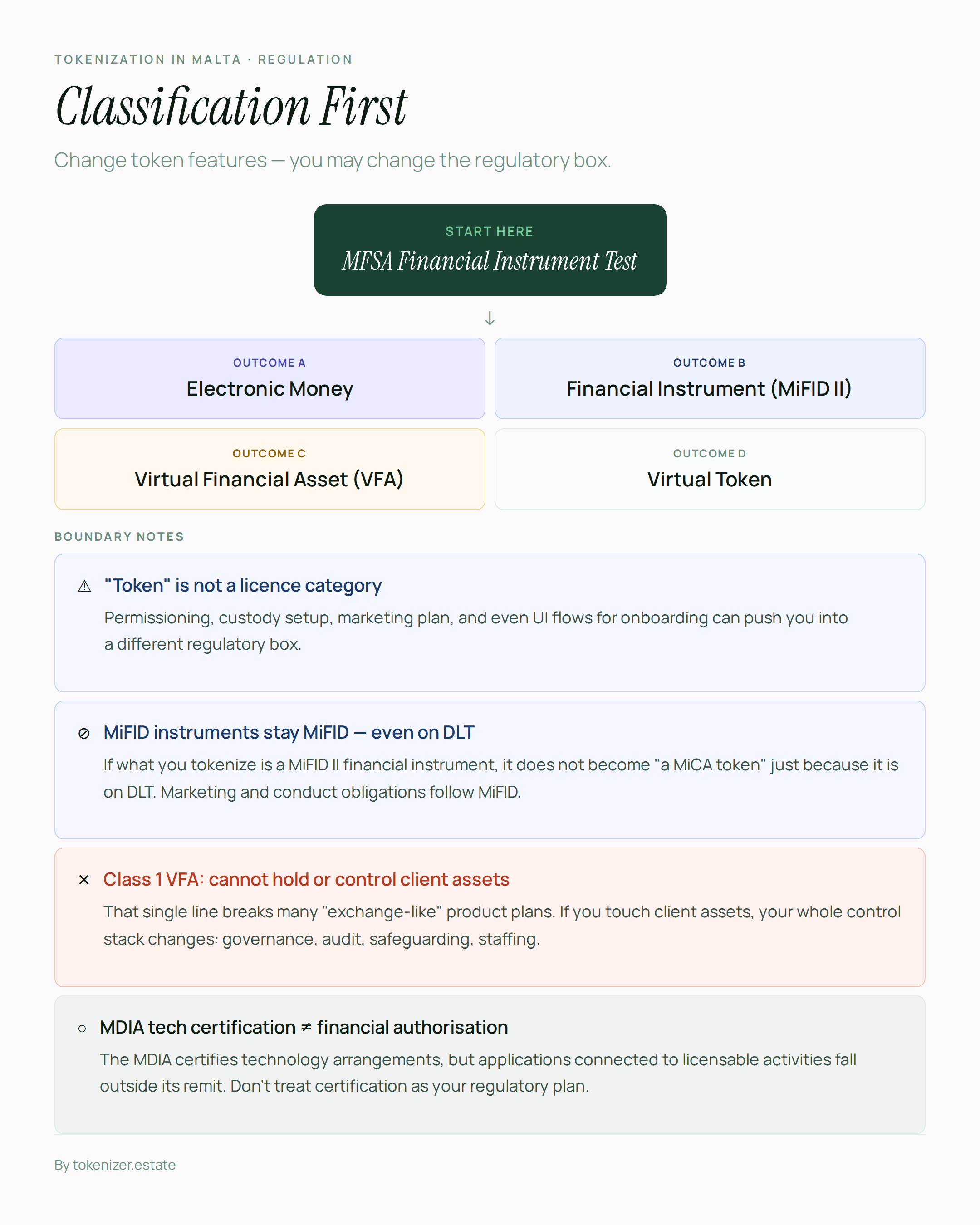

In Malta, the first hard step is classification. The MFSA Financial Instrument Test exists to determine whether a DLT asset is electronic money, a financial instrument, a VFA, or a virtual token. That sounds procedural, but it is a design constraint: change token features, and you may change your regulatory perimeter.

This usually surfaces when teams realize that “token” is not a license category. Your permissioning, custody setup, marketing plan, and even the UI flows for onboarding can push you into a different box.

A common confusion is around MiCA. If what you are tokenizing is already a MiFID II financial instrument (for example, the MFSA treats tokenized CIS units/shares as still being financial instruments), then it does not become “a MiCA token” just because it is on DLT. In the MFSA fund tokenization framing, marketing and conduct obligations follow MiFID, and MiCA is not the perimeter for that instrument.

If your model falls into the VFA services perimeter, the VFA Rulebook becomes operational, not theoretical. For example, Malta’s VFA licensing is class-based, and Class 1 is not allowed to hold or control client assets or money. That single line breaks many “exchange-like” product plans. You can check rulebook when you are mapping what your platform actually does.

This matters once you draw your service boundary. If you touch client assets, your whole control stack changes: governance, audit, safeguarding, and staffing. If you do not touch client assets, you must accept what you cannot offer (and what clients will still need from elsewhere).

One more boundary that trips people up: “tech certification” is not a substitute for financial authorization. The MDIA can certify certain technology arrangements, but it states that applications connected to licensable activities by other lead authorities (like the MFSA) fall outside its remit. Also, Malta’s ITAS Act (Cap. 592) is marked as repealed, with transitional handling for existing recognitions. For most teams, the practical message is simple: don’t treat certification as your regulatory plan.

Tokenization in Malta risks

Most projects fail because they treat the token as the legal record, while the legal truth still sits in the share register or in off-chain contracts.

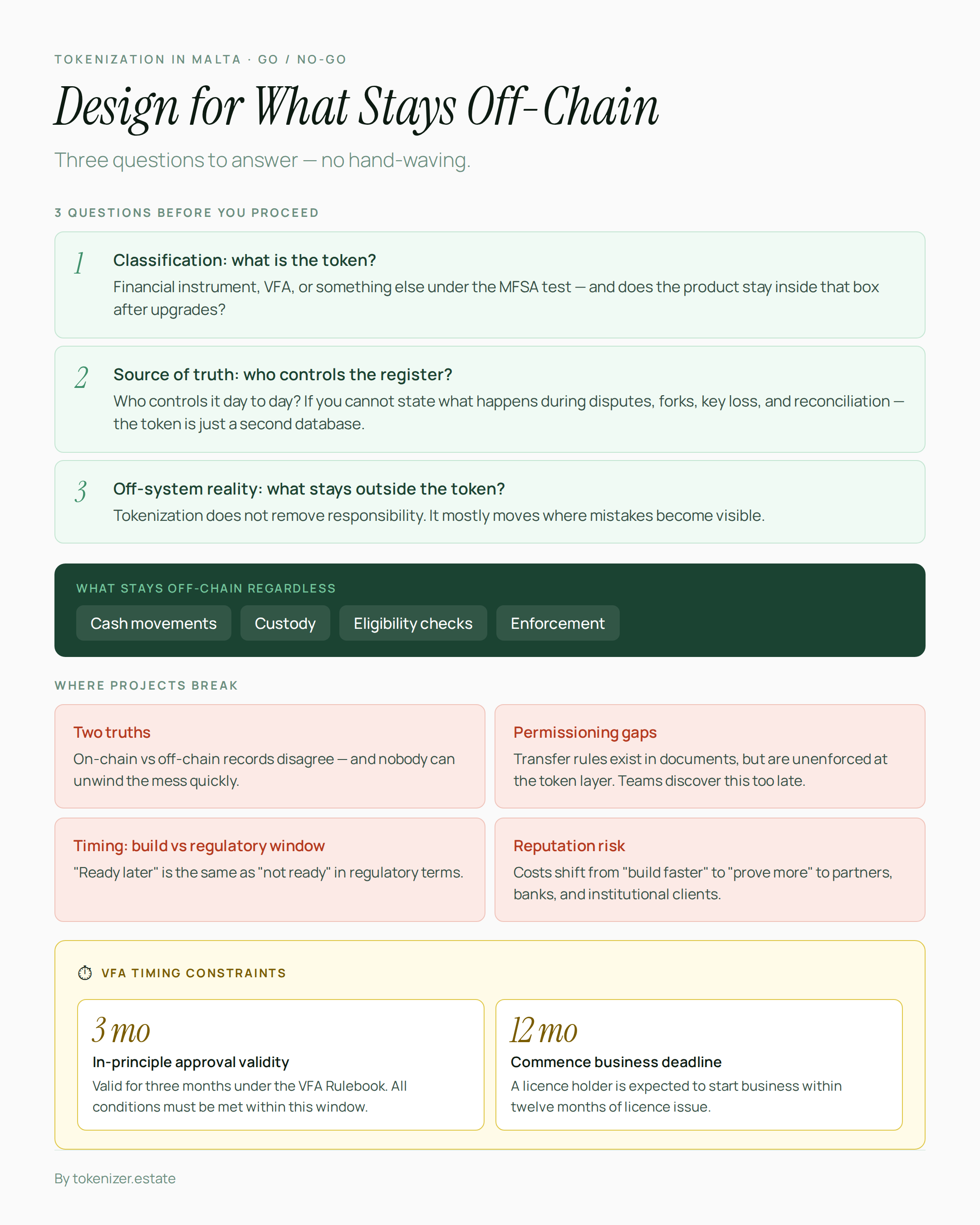

In Malta, this is not a philosophical point. It is an operational failure mode: you can end up with two “truths” (on-chain vs off-chain), and nobody can unwind the mess quickly. This is why share-register authority and reconciliation rules are not legal boilerplate. They are your incident-response plan.

Another under-estimated failure is permissioning. Transfer rules can exist in documents and still be unenforced at the token layer. Teams discover too late that “the smart contract standard” did not magically become their compliance engine.

Timing is also a constraint, not a project-management detail. Under the VFA Rulebook, an in-principle approval for a revised VFA services licence is stated as valid for three months, and a licence holder is expected to commence business within twelve months of licence issue. That matters once your build is longer than your regulatory window. You can end up “ready later,” which is the same as “not ready” in regulatory terms.

There is also a reputational risk that shows up mid-way: if your licensing strategy depends on speed, any public scrutiny of licensing quality can become friction with partners, banks, and institutional clients. In practice, this shifts your costs from “build faster” to “prove more,” and it is rarely budgeted.

If you want a practical lens on what investors later ask when things go wrong, scan checklist. Even if you are not issuing real estate tokens, the due diligence logic is the same: what is the right, who enforces it, and what breaks first.

When tokenization makes sense in Malta

Tokenization in Malta makes sense when you can clearly answer three questions without hand-waving.

First: is your token a financial instrument, a VFA, or something else under the MFSA’s classification approach—and does your product stay inside that box after upgrades?

Second: where is the authoritative record, and who controls it day to day? In fund-unit tokenization, Malta’s own framing puts share-register maintenance at the center for a reason. If you cannot state what happens during disputes, forks, key loss, and reconciliation, the token is just a second database.

Third: what stays off-system? Cash movements, custody relationships, investor eligibility checks, and enforcement do not disappear just because transfers are on-chain. Tokenization can still help. It can widen distribution and reduce friction in recordkeeping, especially when multiple parties need shared access. But it does not remove responsibility; it mostly moves where mistakes become visible.

Conclusion

Tokenization in Malta works best when the token is tied to a clear legal classification, a clear “source of truth” for the register, and a custody/eligibility setup that matches what you actually operate. When these three stay aligned, tokenization can genuinely help with broader investor access and smoother recordkeeping across parties, without pretending the law or operations have disappeared.

If you are at a real decision moment—signing a term sheet, locking a tech stack, or choosing whether to build custody into the platform—treat this as a scope decision, not a branding decision. Malta can support serious tokenization models, and teams do succeed when they choose a structure they can run for years. The key is to design for the parts that stay off-chain (cash, enforcement, eligibility) as carefully as the token itself, because that is where issues usually surface later.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo