Tokenization vs Credit: Why Tokenization Is a Great Alternative to Loans for Developers

Today we’re diving into a smarter way to finance real estate. Instead of piling on bank debt, developers can raise capital by tokenizing projects—turning buildings into digital shares for global investors. We’ll explore how it works, why it’s faster, and who benefits.

Real estate developers have traditionally relied on bank loans (credit) to finance projects – but this comes with high costs and risks, especially when interest rates rise. In recent years, a global shift toward asset tokenization has emerged as an innovative alternative. Tokenization means turning real estate value into digital shares or “tokens” on a blockchain that investors can buy. Experts predict this trend will unlock enormous value worldwide; for example, Boston Consulting Group estimates tokenization could unlock a $16 trillion market by 2030 and even BlackRock’s CEO has hailed tokenization as “the next generation for markets”. In short, tokenization is not just a tech buzzword – it’s becoming a practical funding tool. This article explores how tokenization can serve as an excellent alternative to traditional credit (loans) for property developers, offering a way to raise capital that is faster, less risky, and more inclusive than bank financing.

Tokenization: Turning Buildings into Digital Shares

Tokenization is the process of converting rights in an asset (like a building or a development project) into small digital units called tokens. In simple terms, it turns bricks into tiny digital shares kept on a blockchain. Each token represents a fraction of the property’s value or ownership. Because these tokens are recorded on a secure distributed ledger, transactions can happen quickly and transparently. In fact, deals can clear in seconds and paperwork is coded, so costs fall and small investors get access once reserved for big funds. Tokens can be bought and sold online, allowing people around the world to invest in a property without the usual barriers.

For a developer, this means you can fractionalize your project into, say, thousands of tokens, each giving the buyer a small stake. It’s similar to crowdfunding, but powered by blockchain: investors immediately receive digital proof of their ownership stake. These security tokens might grant investors rights to a share of rental income or future profits from the sale, depending on how the deal is structured. All of this is done in a regulated framework with compliance checks (know-your-customer, anti-money-laundering, etc.) handled by the platform, so the process is secure and legal. In essence, tokenization provides a new fundraising route for developers – one that doesn’t depend on taking a bank loan.

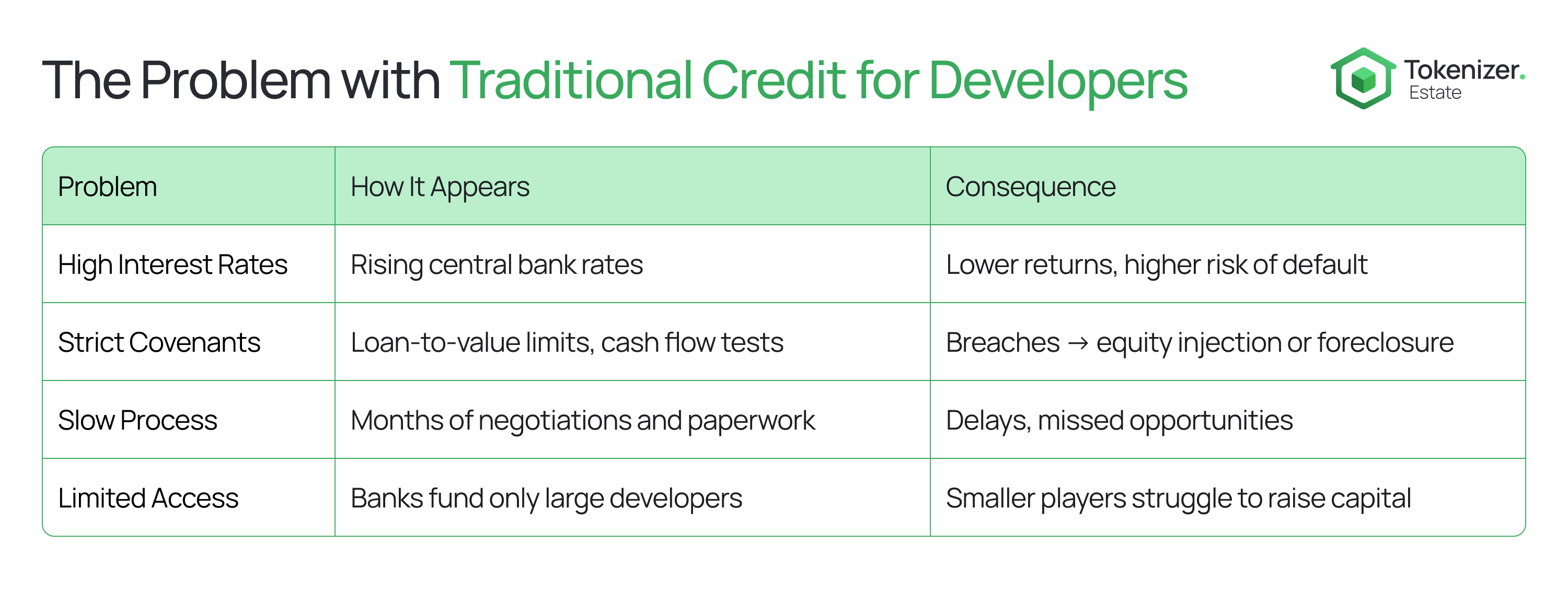

The Problem with Traditional Credit for Developers

Raising capital through bank loans has long been the norm, but it carries significant downsides for developers:

- High Costs and Interest Rate Risk: Loans come with interest that can eat into project returns. When central bank rates climb, borrowing becomes more expensive. As one industry CEO explained, when interest rates rise, property values drop – leading to higher borrowing costs and riskier loans for developers. If a project’s value falls, a developer with a large loan might breach loan covenants and face pressure to inject more cash or risk foreclosure. In other words, debt can turn a downturn in the market into a crisis for the project.

- Strict Terms and Covenants: Banks often impose strict conditions (like loan-to-value limits). If the property value declines or sales slow, the developer might violate these terms. For example, a loan usually must remain below a certain percentage of the property’s value (often 80%). Should values drop, the loan can become distressed, forcing the developer to put in additional equity to rebalance the loan ratio. Failing to do so could result in the bank taking over the property (foreclosure). This scenario is a constant worry when relying heavily on credit.

- Slow and Opaque Process: Traditional financing can be slow and bureaucratic. Securing a big construction loan or mortgage for a development means lengthy negotiations, extensive paperwork, and multiple intermediaries (brokers, underwriters, appraisers). A typical commercial real estate financing deal might take many months to close, delaying projects. All the while, market conditions (interest rates, investor demand, costs) can change, adding uncertainty. This slow timeline can hinder developers who need to move quickly or seize a market window.

- Limited Access to Capital: Banks are often conservative, and some worthwhile projects don’t get funded because they “don’t fit the box.” Smaller developers or those in emerging markets might struggle to get large loans without extensive credit history or collateral. Moreover, banks and private lenders usually offer big sums to a few borrowers, rather than small sums to many – meaning the pool of available capital is limited to those traditional channels.

In summary, while credit has been the go-to financing method, it can be expensive, rigid, and risky. A developer taking on a huge loan is essentially betting that the project value will stay high and that cash flow will cover the interest. If anything goes wrong, the debt becomes a heavy burden. This is where tokenization offers a compelling alternative.

How Tokenization Offers an Alternative to Bank Loans

Tokenization can address many of the above issues by offering a different approach to raising money – more like equity financing from a broad base of investors rather than debt from a bank. Here’s why tokenization is such an attractive alternative for developers:

- No Interest or Monthly Payments: Unlike a loan, tokenization isn’t about borrowing money that must be paid back with interest. Instead, the developer sells a portion of the project’s equity to investors via tokens. There are no interest payments draining the project’s cash flow each month, and no balloon payment to worry about later. This dramatically lowers the cost of capital. In fact, replacing a bank loan with tokenized investor equity removes interest rate risk and reduces financing costs overall. The project’s funding becomes more stable because it’s based on shared ownership, not owed debt.

- Lower Risk of Default: Since there is no debt to repay, the concept of default changes. The investors who bought tokens accept the investment risk in exchange for potential returns, just like any equity investor. A developer doesn’t face foreclosure risk from token holders the way they would from a bank loan. If the market dips, the asset value might temporarily drop, but there isn’t a bank demanding its money back. This de-risks the project structure – the developer and investors share the upside and downside, rather than the developer having a fixed obligation to a lender regardless of performance.

- Faster and More Flexible Fundraising: Tokenization can dramatically speed up the fundraising process. Instead of negotiations with a bank credit committee, a token offering can be marketed on a platform to many investors at once. Once the offering goes live, the capital can be raised in a very short time frame – even days or hours rather than months. We’ve already seen striking examples: a tokenized real estate offering in Dubai was fully funded in just 1 minute 58 seconds, attracting 149 investors from 35 countries. In another case, one project raised $18 million by tokenizing a luxury resort, with the sale closing much faster than a traditional deal. This speed is possible because blockchain platforms streamline the process of issuing shares and handling transactions, cutting out many middlemen and inefficiencies. A developer can essentially “crowdfund” a large sum from a global audience once the digital infrastructure is set up – a far cry from waiting on a single bank’s approval. The fundraising doesn’t need to be all-or-nothing either; developers can raise portions of the required capital in stages, or combine tokenized equity with some bank financing to reduce overall debt.

- Access to a Global Investor Pool: One of the greatest advantages is the global reach of tokenized fundraising. By converting a property into digital tokens, a developer can tap investors far beyond their local market. Anyone with an internet connection and proper accreditation (as required by regulations) can participate. This means a project in one country can attract capital from investors in diverse regions, which is usually impossible with traditional loans confined to local banks. For example, the Dubai tokenized apartment sale mentioned above had buyers from dozens of countries. Tokenization removes geographic barriers for investors. Moreover, because tokens can be inexpensive (you could split a building into tens of thousands of tokens), the buy-in can be as low as $50 or even less, enabling ordinary people to invest. In Saudi Arabia, a developer in 2025 even unveiled a pilot allowing every citizen to buy tokens in a luxury tower for as little as 1 Saudi Riyal (about $0.27). This kind of access was unthinkable with traditional financing – it essentially democratizes real estate investment. For developers, a wider investor base means fundraising can be quicker and less dependent on a few big players. If one source of funding dries up, there are others around the world who might still participate.

- More Liquidity for Investors (and Developers): Real estate is famously illiquid – once you invest, your money is typically locked until the project is sold or refinanced. Tokenization changes that by making shares of the project tradeable. Investors know they may be able to sell their tokens on secondary markets without waiting years, which makes them more willing to invest in the first place. This liquidity optionality is a huge draw. From the developer’s perspective, a more liquid investment product is easier to sell to investors – it’s a selling point that can attract more capital. In some cases, tokenization might even allow the developer to recoup some funds early by selling a portion of their own tokens once the project is successful, though this depends on the arrangement. The key point is that tokenization brings the flexibility of markets to an asset class that used to be very rigid. Investors can enter and exit more freely, which ultimately supports developers in raising money and maintaining investor confidence.

- Streamlined Process with Fewer Middlemen: Traditional fundraising involves many intermediaries (lawyers, brokers, banks), each adding cost and delay. Tokenization platforms use smart contracts to automate many processes (like verifying transactions, distributing dividends, etc.). This has eliminated the need for many intermediaries such as brokers and banks in the transaction, which lowers transaction costs and makes the process more efficient. Developers save on fees and paperwork. For instance, smart contracts can automatically handle rent collection and profit distribution to hundreds of token holders, tasks that would be cumbersome manually. With tokens, a developer could manage thousands of investors’ contributions and payouts at the push of a button, whereas traditionally having even a dozen investors would require significant administrative work. This efficiency means even a small team can manage a large, tokenized investor base without hiring an army of accountants and lawyers, keeping overhead low.

- Retention of Control and Flexibility: One concern developers might have is: “If I sell tokens, am I giving up ownership or control of my project?” Tokenization is typically structured so that while investors obtain a share of the economic rights (like a share of income or eventual sale proceeds), the developer (sponsor) retains decision-making control over the project. In many tokenized real estate offerings, investors are passive and the sponsor continues to manage the asset. It’s somewhat analogous to being the general partner (GP) who runs the project while token holders are like limited partners. The developer can choose how much equity to tokenize – it could be 10%, 30%, 50% of the project, depending on funding needs and how much they want to avoid debt. They can still hold a significant fraction of the property so they don’t “give everything up”. This flexibility allows developers to optimize their capital stack: maybe replace the most expensive debt first, or avoid having to bring in a big private equity investor who might demand control. In short, tokenization can be structured to fill financing gaps while the developer maintains operational control and a sizeable ownership stake.

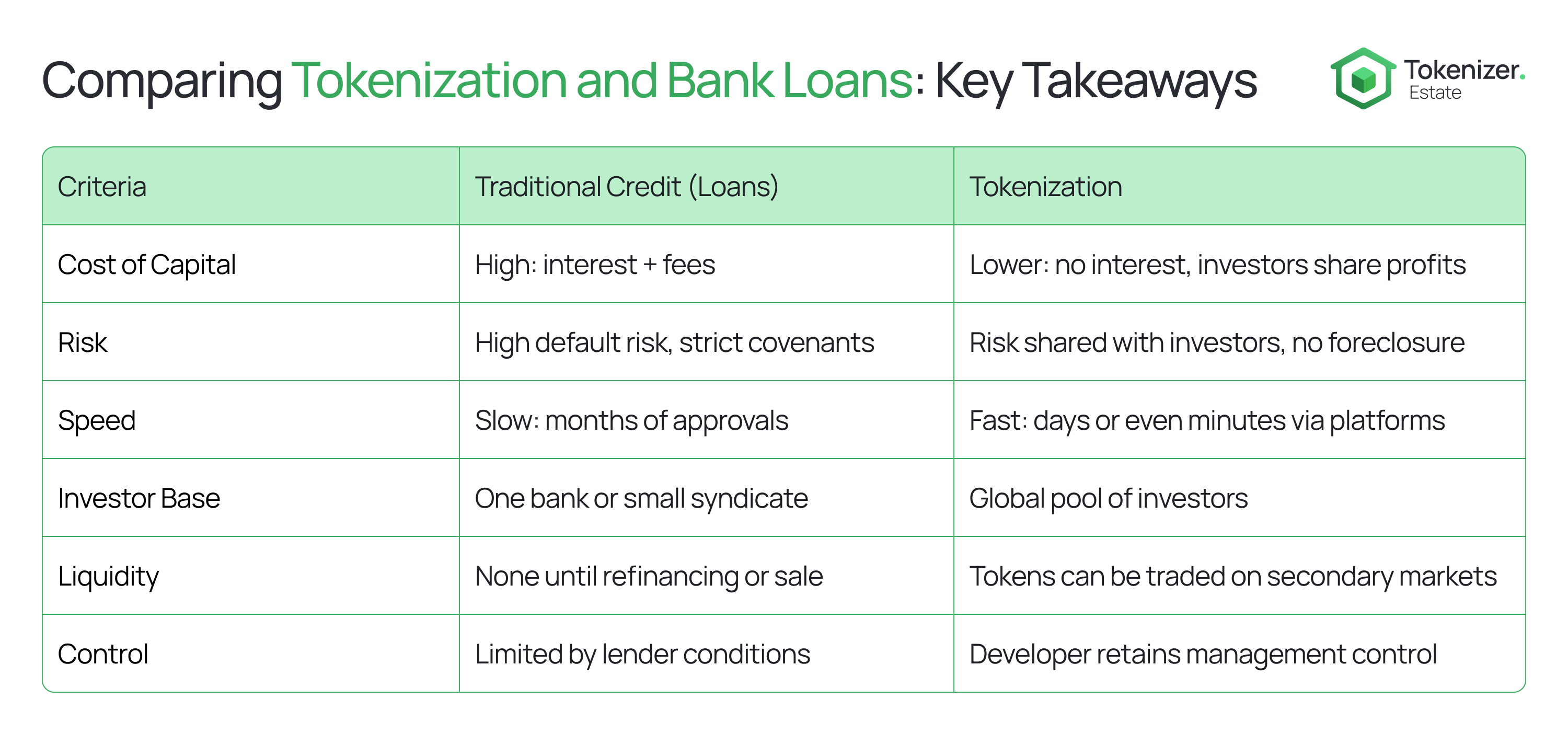

Comparing Tokenization and Bank Loans: Key Takeaways

Let’s summarize the differences between raising money via traditional credit vs. via tokenization:

- Cost of Capital: A bank loan comes with fixed interest that must be paid regardless of project performance. Tokenization brings in equity funding with no mandatory interest payments – investors are paid from actual project returns. This can significantly lower the financing cost and remove pressure during slow periods.

- Risk Distribution: With a loan, the developer carries the repayment risk entirely (potential default if things go wrong). With tokenization, risk is shared with investors – if the market weakens, everyone’s share value might dip, but there’s no lender to trigger a foreclosure. This spreads out risk and provides a cushion for the developer in tough times.

- Investor Base: Credit usually comes from one institution or a small syndicate of lenders. Tokenization opens the door to hundreds or thousands of investors worldwide. This broader investor base can often supply capital more quickly and flexibly, as seen when a tokenized offering sells out in minutes online. It also means a project’s success isn’t tied to one financier’s conditions.

- Speed and Convenience: Obtaining a loan can take months of due diligence, while a token offering, once prepared, can fund much faster through a platform. Digital transactions cut down delays – fundraising that once took 6–9 months can potentially happen in weeks or less in a well-orchestrated token sale. Moreover, the process is investor-friendly: people can invest with a few clicks, which increases participation. One source notes that thanks to blockchain and smart contracts, real estate developers can raise capital faster and more efficiently at any stage, instead of being held back by traditional funding bureaucracy.

- Regulatory Compliance: Banks are heavily regulated (which provides some safety to the process but also rigidity). Tokenization is a newer field, but it is increasingly operating under securities laws with proper compliance. Platforms conducting Security Token Offerings ensure KYC/AML checks and follow regulations (often using exemptions like Regulation D, S, or A+ in the US, for example). The difference is the innovation in tech doesn’t compromise investor protection – compliance is built into the process with digital efficiency. Many jurisdictions are updating laws to recognize tokenized securities. For instance, Dubai integrated tokenized properties into its legal system in 2025, and other governments are also crafting supportive rules. The bottom line: tokenization can be done in a regulated, legal manner, similar to issuing shares – it’s not an outlaw alternative, but a legitimate one.

- Outcome for the Developer: With a loan, if the project succeeds, the developer repays principal + interest, and whatever profit remains is theirs (after also paying the bank’s interest). With tokenization, if the project succeeds, the developer shares some of the profit or ownership increase with token investors, but often still comes out well (they kept a portion of equity without the drag of interest). If the project struggles, the developer with a loan could lose the property, whereas with tokens, the developer might lose some equity value but not the project control. In essence, tokenization can offer more upside sharing but less catastrophic downside compared to heavy leverage.

A Global Perspective: Momentum Builds

Tokenization isn’t just a niche idea – it’s becoming a worldwide movement in real estate finance. In a global real estate tokenization highlights report, it was noted that by mid-2024 about 12% of real estate firms globally had already implemented tokenization in some form, with another 46% piloting projects. This shows that nearly half of the industry’s players were experimenting with tokenized assets, signaling rapidly growing acceptance. Around the world, from the Middle East to Asia, regulators and companies are launching tokenized property initiatives. We saw Saudi Arabia’s 1-riyal token pilot for inclusion of everyday citizens, and Dubai’s pioneering projects that made headlines by selling fractions of buildings instantly to international buyers.

Major financial institutions are also backing the trend. Besides BlackRock’s endorsement of tokenization’s future, firms like Ripple predict that tokenizing real-world assets (including real estate) could reach nearly $19 trillion in value by 2033. Even traditional banks and exchanges are investing in tokenization platforms, recognizing that this could become a standard way to trade assets. All this momentum means developers who opt for tokenization aren’t alone – they’re part of a broad movement reshaping how real estate is bought and sold. The technology, investor interest, and regulatory frameworks are aligning in favor of tokenized finance, making it an increasingly viable option across the globe.

Conclusion: Tokenization as a Smart Financing Alternative

For today’s property developers, especially in an era of high interest rates and tight credit, tokenization offers a breath of fresh air and a powerful alternative to traditional loans. By issuing digital tokens, developers can tap into global capital markets, access funding faster, and avoid saddling their projects with onerous debt. The narrative is clear: tokenization can replace or supplement bank loans with investor equity, allowing developers to fund projects without the strain of interest payments and with significantly reduced risk. It’s a financing strategy where investors big and small become partners in the project’s success, rather than the developer borrowing money under pressure to pay it back no matter what.

Crucially, tokenization aligns with the interests of both developers and investors. Developers gain flexibility, speed, and wider access to funds; investors gain access to asset classes (like high-end real estate) that they could not touch before, plus the chance for liquidity. As we highlighted in our own case study from Dubai, when given the opportunity to buy fractional real estate via tokens, investors will rush in – even in under two minutes. The demand is out there, and it’s growing.

Of course, tokenization is still a new approach. It requires setting up proper legal structures and choosing the right platform to ensure everything is compliant and secure. But these hurdles are getting lower each year, with more service providers and clear regulations in place. Early adopters are already proving that tokenized real estate funding works, from upscale condominiums to commercial towers. By 2025, the technology is mature enough to trust, yet still novel enough that those who act now can stand out and reap the benefits of being pioneers.

In summary, tokenization is proving to be a great alternative to traditional credit financing for real estate. It empowers developers to raise capital on their own terms – faster, with less cost and risk – by leveraging the power of blockchain and global investor interest. While bank loans will certainly remain part of the financing toolkit, tokenization provides a complementary (and in many cases superior) route to fund projects. Developers who embrace this new model can unlock funds without being chained to debt, all while bringing more investors along for the journey. Given the advantages and the global trend toward digitizing assets, tokenization is poised to move from an alternative to a mainstream solution in real estate finance. For forward-thinking developers, it’s an opportunity to secure funding in a smarter way – one that aligns with the future of investment and the democratization of wealth in real estate.

Ultimately, the choice is not just tokenization vs credit, but how best to combine innovation with prudence. And as the evidence shows, tokenization offers a compelling path to do things differently: to build and finance the world around us with broader participation and fewer limitations. It’s a win-win scenario – making it an alternative well worth considering for your next project.