Tokenization vs Crowdfunding: New Ways to Invest in Real Estate

Real estate investing is changing. Two models—crowdfunding and tokenization—make it possible to join projects with small amounts. This article explains how they differ and why tokenization is becoming the stronger trend in 2025.

Real estate investing has changed in recent years. Now many people can own a piece of a building with a relatively small amount of money. Two big new ideas are crowdfunding and tokenization. Both allow many small investors to join together to fund a real estate project. In crowdfunding, people pool their funds to help a project owner build or renovate a property. In tokenization, a property is split into digital shares on a blockchain, and investors buy these tokens to own a fraction of the asset.

Crowdfunding and tokenization work differently. Crowdfunding is like giving a loan to a project, while tokenization means you actually own part of the property. In this article, we will explain each method, compare their strengths and risks, and show why tokenization is becoming a more powerful model for investors. By 2025, tokenization was moving from theory into real projects worldwide, making real estate investing faster, more transparent, and more democratic than ever.

What Is Real Estate Crowdfunding?

Real estate crowdfunding is a way for many investors to finance a property project together. For example, a developer might list a new apartment building on an online platform. Dozens or hundreds of people each invest a small amount of money toward the project. Together, these funds reach the total needed to buy or develop the property. In return, the investors get paid back later, usually with interest or a share of the profits when the property is sold or earns rent.

Unlike buying a stock, crowdfunding investors do not own a piece of the building itself. Instead, their money is typically treated like a loan. A blog explains that in crowdfunding investors usually provide subordinate loans, meaning they lend money to a project but have no ownership claim on the property. This is important: if the project fails, crowdfunding investors are repaid last (after senior debt), so their investment is riskier.

Crowdfunding is popular because it is simple and well-known. Platforms handle the paperwork and legal issues. They often require only a modest minimum investment, so even new investors can join. One source notes that crowdfunding processes are usually straightforward and already accepted under existing laws. On the downside, crowdfunding money is often locked up for the duration of the project. Investors may have to wait months or years until the project finishes to see any return. If the project does not succeed, crowdfunding backers can lose their capital.

What Is Real Estate Tokenization?

Real estate tokenization uses blockchain technology to turn property into digital tokens. In simple terms, imagine a skyscraper is divided into many tiny digital pieces. Each piece is a token on the blockchain. If you buy a token, you become a fractional owner of that building. This is different from crowdfunding loans: token holders share in the actual ownership and income of the property.

In our blog we have already discussed that: tokenization converts property value or ownership rights into digital tokens on a blockchain, letting people buy and trade fractions of buildings as easily as stocks. In practice, the property is placed in a company or fund, and tokens are issued to represent shares of that entity. When you own tokens, you are entitled to a portion of any rental income or sale profits, just like a shareholder gets dividends.

Blockchain adds important features. Every token transaction is recorded on a secure public ledger. This means ownership is transparent and hard to tamper with. You can check on the blockchain to see who owns which tokens. Tokenization often uses smart contracts (automated rules) to distribute rent payments directly to token holders’ digital wallets. Some projects even let token holders vote on property decisions. In short, tokenized real estate blends property stability with the speed and transparency of digital markets.

Because of tokenization, investors can own real estate with much less money. Instead of needing tens of thousands of dollars to buy a share, some token sales allow investments of just a few dollars or euros. Tokens can often be traded on exchanges 24/7. This provides high liquidity: you can buy or sell your share of a property at almost any time. In fact, many tokenized projects target annual returns around 8–12% by cutting out middlemen and focusing on efficient rentals. Investopedia notes that tokenization cuts out red tape and many fees compared to traditional real estate, saving investors on costs.

On the other hand, tokenization is still new and can be complex. It usually requires some comfort with blockchain wallets and cryptocurrency. Because rules are still evolving globally, token offers must follow securities laws, which can vary by country. For now, tokenized markets are smaller than the overall real estate market (in 2025 maybe around a billion dollars worldwide), but they are growing fast. And with more governments beginning to recognize digital assets, tokenization is becoming increasingly secure and attractive.

Key Differences Between Crowdfunding and Tokenization

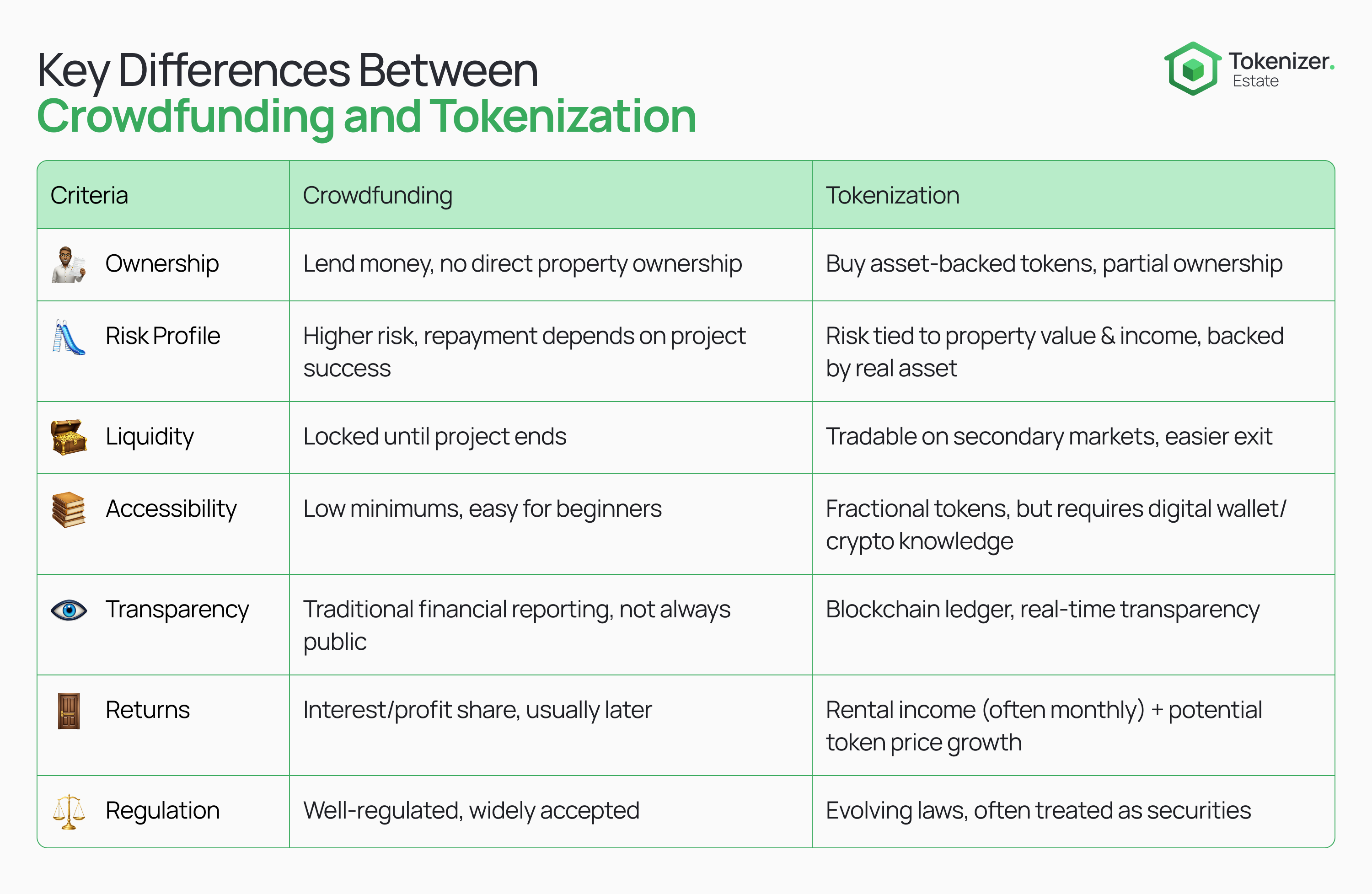

The main difference is ownership vs lending. In crowdfunding, you mostly lend money: the investors fund the project but do not hold the title to the property. They expect a loan repayment or share of profits. In tokenization, you buy actual shares of the asset. Owning tokens makes you a partial owner of the building (through a legal company).

This leads to different risk profiles. Crowdfunding is generally riskier because it sits lower in the debt chain. If the project fails or debts can’t be paid, crowdfunding backers may lose money. Token holders face risk tied to the property’s performance, but they at least own a real asset.

Liquidity also differs. Crowdfunding investments are usually locked until the project ends. You cannot easily sell your share before then. By contrast, tokens are often tradable on secondary markets. This means token investors can liquidate their holdings at any time. A token sale or exchange lets you exit faster.

Accessibility and entry costs: Both models lower the barrier compared to buying whole properties. Crowdfunding platforms often have low minimums, making them accessible to many people. Tokenization also allows tiny investment amounts thanks to fractional tokens. However, token buyers must be familiar with digital wallets or crypto exchanges, which adds a technical step. Yet, for many younger investors who already use digital apps, this is a natural shift.

Transparency and technology: Tokenization leverages blockchain technology to make records open. Every transaction is logged on the chain, giving real-time transparency to ownership and income. Crowdfunding uses traditional financial records, which are reliable but not always instantly public. The blockchain nature of tokens can increase trust and reduce fraud.

Returns and Payouts: Crowdfunding investors often earn returns from interest or profit shares, usually paid after the project ends or periodically from income. Token holders can receive rental income directly (sometimes in stable cryptocurrencies) and also benefit if the token’s market price goes up. For example, some token projects pay out monthly rent automatically. In effect, token rent payments are similar to REIT dividends but can occur more frequently.

Regulation and legal framework: Crowdfunding is generally well-regulated and accepted in many countries. Tokenization is newer, and laws are evolving. In some places, property tokens are treated like securities, requiring compliance with stock laws. While this adds complexity, it also signals that regulators are taking tokenization seriously as a mainstream financial tool.

Why Tokenization Stands Out

In practice, crowdfunding and tokenization serve different investor goals. Crowdfunding is often ideal for people who want a straightforward, hands-off investment and can accept locking up their money for a defined project period. It is like a loan to the developer with a planned return. But tokenization is more than that: it is a new financial model that gives investors true ownership, more liquidity, and stronger transparency.

- Crowdfunding: Good for beginners or those seeking short-term, fixed returns. It usually has low technical requirements and familiar investment structure.

- Tokenization: Suited for investors who want fractional ownership, global access, and the potential for higher liquidity and yields. It also empowers investors with transparency and gives them a direct role in the property’s income.

Ultimately, tokenization is the model that points toward the future. As one analysis concludes, “if you seek ownership, transparency, and liquidity, tokenization is the more advanced and secure model. But if you prefer straightforward, low-barrier entry into real estate with short-term goals, crowdfunding may be the way to go.”

Both crowdfunding and tokenization are likely to coexist, but tokenization clearly has the edge in shaping real estate’s digital future. By understanding their key features and risks, you can choose the method that fits your goals – and increasingly, that means exploring tokenized property.

Further Reading

For more on these topics, our blog has articles on how tokenization works and how it compares to traditional real estate models. For example, one post explains the detailed process of tokenizing a property. Another post compares tokenized real estate to REITs and mentions that tokenization uses blockchain instead of older systems.

Regardless of the method, always do your homework. Check the project details, the platform’s track record, and any legal notices. Real estate crowdfunding and tokenization both hold promise for democratizing real estate investment – but they each come with their own rules and risks. The key is to match your choice to what matters most to you: simplicity or ownership, stability or flexibility.