Commercial real estate tokenization 2026: offices, warehouses, and data centers go on-chain

In 2020, RedSwan tokenized $2.2 billion of Class A buildings in an hour. By 2026, they have $5 billion on-chain. Deloitte predicts $4 trillion by 2035. This is the practical guide to commercial real estate tokenization — deal structure, economics, asset types, and the honest risks.

In 2020, a company called RedSwan tokenized $2.2 billion worth of office buildings and apartment complexes across New York, California, and Texas. Class A properties — the kind normally reserved for funds with $100 million to deploy. They did it in an hour using a token studio. No banks. No six-month process. Just digital securities on a blockchain, each representing a fraction of a real building with real tenants.

By 2026, RedSwan has tokenized over $5 billion in commercial real estate on the Hedera network, with a pipeline targeting $25 billion in 36 months. Their CEO, Ed Nwokedi — an 18-year Cushman & Wakefield veteran — put it simply: "Tokenization is not just about fractionalizing assets. It is about fundamentally redefining ownership, enhancing liquidity, and creating a more transparent marketplace."

The $4 trillion forecast — and why CRE leads it

In April 2025, Deloitte's Center for Financial Services published a prediction that changed how the industry talks about scale: tokenized real estate will reach $4 trillion by 2035, growing at 27% annually from less than $300 billion in 2024.

Here is the part that matters for commercial real estate owners: the largest segment of that $4 trillion — roughly $2.4 trillion — is expected to be tokenized loans and securitizations tied to commercial properties. Another $1 trillion will be tokenized private real estate funds. And $500 billion will come from undeveloped land and construction-stage projects.

In other words, commercial real estate is not a side story in the tokenization narrative. It is the main event.

Why? Because CRE has the exact properties that make tokenization valuable: large ticket sizes that need fractionalization, long-term leases that make automated dividends reliable, corporate tenants that make cash flow predictable, and a chronic liquidity problem that tokenization directly addresses.

A $40 million logistics warehouse leased to Amazon for ten years is a perfect tokenization candidate. The income is stable, the tenant is creditworthy, the lease terms are programmed into a smart contract, and 400 investors across 14 countries can participate at $5,000 each — while the original owner keeps 80% and continues to manage the asset.

Why commercial is different from residential — and why it matters

Most tokenization stories start with residential: a house in Detroit for $50, an apartment in Bali for $500. These deals are real, and they opened the market. But commercial real estate is a fundamentally different asset class, and the differences change how tokenization works.

Ticket sizes are larger. A single commercial building can be worth $20 million to $2 billion. The traditional investor pool is tiny — banks, institutional funds, ultra-high-net-worth individuals. Tokenization expands this pool by orders of magnitude.

Income is more predictable. Commercial leases run 5 to 15 years with built-in escalations. This makes smart contract automation — automatic dividend distribution to hundreds of token holders — far more reliable than residential rent, which changes month to month.

Legal complexity is higher. Commercial properties sit inside multi-layered SPV structures, holding companies, and joint ventures. Tokenization adds a digital layer on top. The token represents a share in the SPV that owns the building — not the building itself.

The liquidity problem is worse. Selling a commercial building takes 6 to 18 months. Selling a token can take minutes — if there is a buyer and a secondary market.

What types of commercial property are being tokenized

Not every building is a good fit. Here is what is working in 2026 — and why.

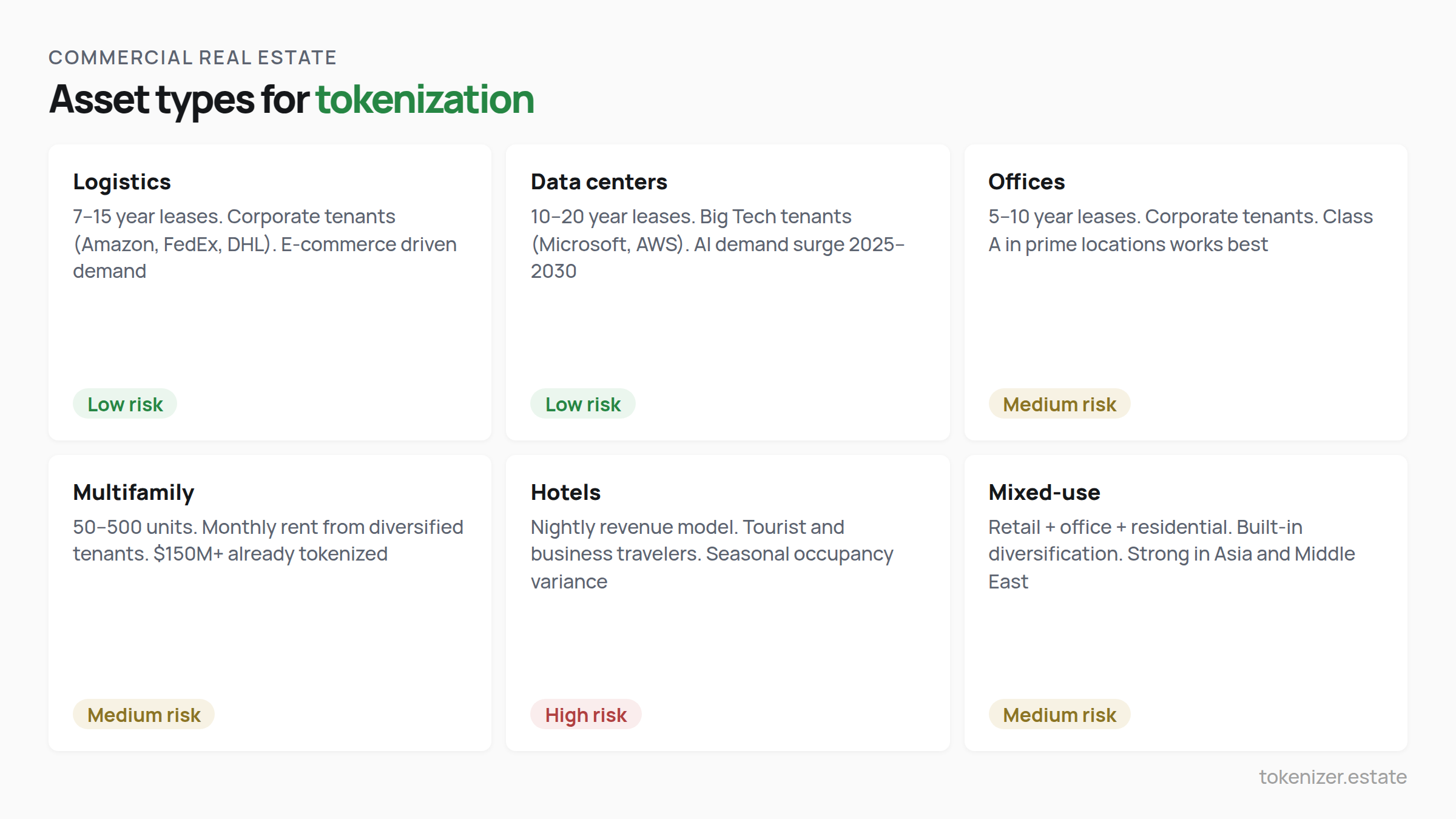

Logistics and warehouses are the fastest-growing segment. E-commerce has made distribution centers, cold storage, and last-mile hubs some of the most in-demand real estate in the world. The tenants — Amazon, FedEx, Walmart, DHL — sign long leases and pay predictable rent. For tokenization, these assets are ideal: stable income, low management complexity, strong appreciation story. RedSwan recently launched a tokenized logistics portfolio across Costa Rica's industrial hubs — fully leased, operational, and backed by corporate tenants.

Data centers are the breakout asset class of 2026. AI infrastructure demand is growing so fast that operators cannot build capacity fast enough. The tenants — Microsoft, Google, AWS, Meta — are among the most creditworthy companies on earth. The leases are long, the margins are strong, and the growth trajectory is obvious. Data center operators need capital now, not in six months. Tokenization lets them raise it from global investors while banks are still reviewing the loan application. Office buildings are being repurposed into AI data centers in cities across the US and Europe — and tokenization is how the capital is being assembled.

Office buildings were the first CRE asset type to be tokenized. Class A offices in prime locations — Manhattan, Faria Lima in São Paulo, Canary Wharf in London — still tokenize well. Long leases with corporate tenants create reliable cash flows. The challenge: post-pandemic remote work has increased vacancy in some markets, making investors more selective. Location and tenant quality matter more than ever.

Multifamily apartments — buildings with 50 to 500 units — sit at the intersection of commercial and residential. They generate rental income from many tenants, which reduces single-point-of-failure risk. RealT has tokenized over $150 million in US multifamily units. HoneyBricks (now EquityMultiple) closed $180 million in deals for 3,500 investors. RedSwan's Rhythm & Blues project in Oak Park, Illinois, offers tokenized access to a modern apartment community.

Hotels and hospitality offer the highest potential returns — and the highest risk. The St. Regis Aspen Resort raised $18 million through tokenization. RedSwan listed the Carmen Hotel in Playa del Carmen, an adults-only boutique property. Nightly revenue can exceed long-term rental yields, but occupancy varies by season and economic conditions.

Mixed-use developments combine retail, office, and residential in a single building. They offer built-in diversification: if the office floor is vacant, the retail and residential floors still generate income. These are emerging as a strong tokenization category, particularly in Asian and Middle Eastern markets.

Inside a real deal: how RedSwan + Altus tokenized a CRE portfolio

Theory is one thing. Let us look at an actual deal.

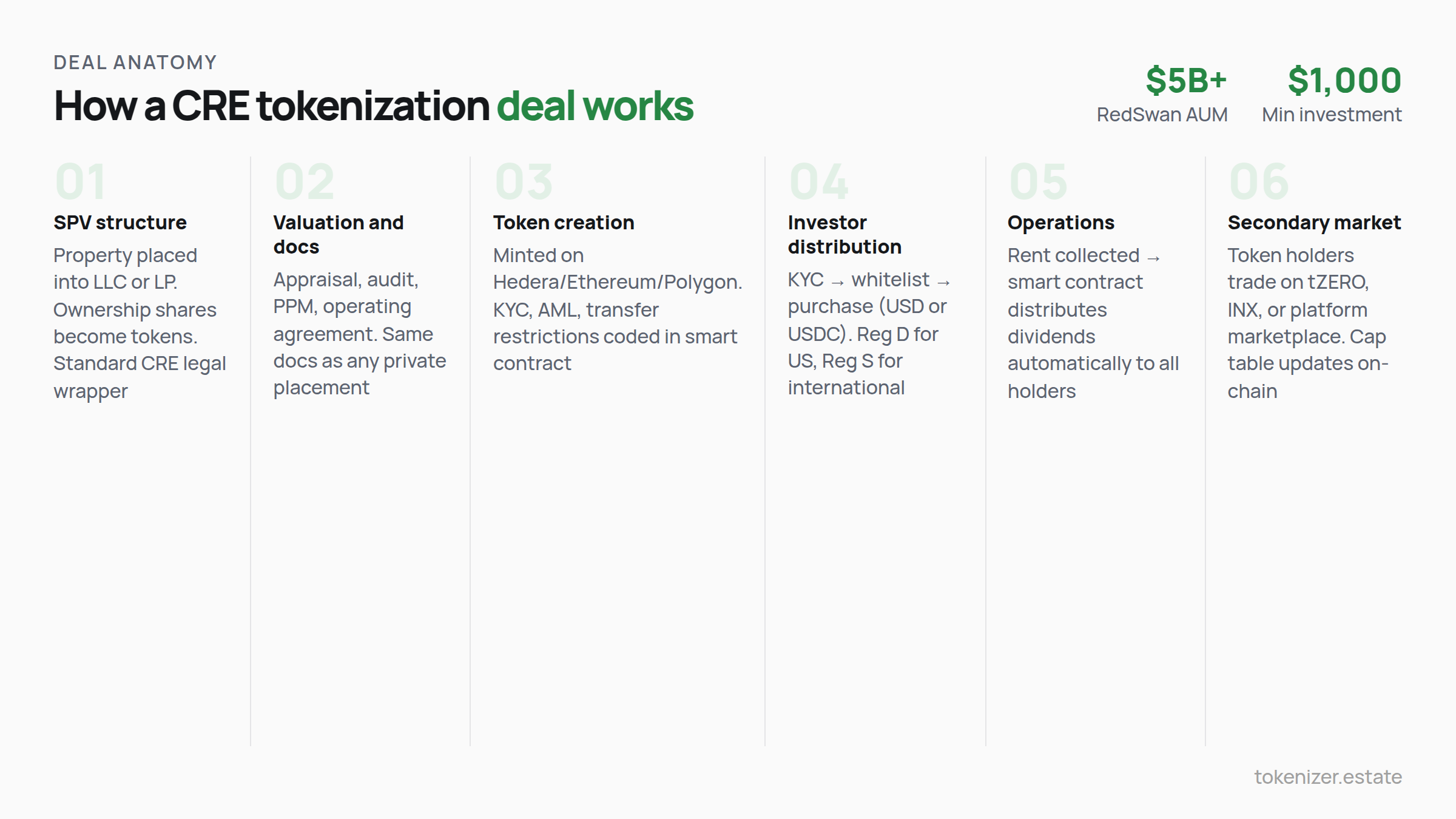

RedSwan partnered with Altus Equity Group to tokenize a portion of the Altus Opportunity Fund — a diversified portfolio of income-generating properties across rapidly expanding US markets. The tokens were minted on the Hedera network and offered to accredited investors under Regulation D (for US investors) and Regulation S (for international investors).

Here is how it worked in practice.

Altus Equity had an existing portfolio of stabilized properties — multifamily, hospitality, and industrial assets across several US states. They wanted to raise additional capital without selling assets or diluting existing investors disproportionately. RedSwan structured the deal as a tokenized limited partnership. Each token represented fractional ownership in the fund, giving holders rights to cash flow distributions and a share of appreciation.

The tokens were created using Hedera Token Service with built-in KYC/AML compliance. Transfer restrictions were coded into the smart contract — only whitelisted, verified investors could hold or trade the tokens. The minimum investment was brought down from the traditional institutional threshold (often $250,000+) to a level accessible to accredited individual investors.

As Forrest Jinks, CEO of Altus Equity Group, put it: the fund's architecture was "designed to mitigate risk, generate meaningful cash flow, and capture significant upside potential — all within a single, well-structured vehicle."

The tokens can be traded on RedSwan's secondary marketplace, giving investors liquidity that traditional private real estate funds simply cannot offer. The underlying assets continue to operate normally — tenants pay rent, property managers manage, and cash flows are distributed to token holders automatically.

This is what institutional-grade CRE tokenization looks like in 2026. Not a concept. A completed deal with real assets, real investors, and a real cap table running on-chain.

The economics — a concrete example

Every asset owner asks: what does it cost, and what does it return?

Let us use a specific example. You own a logistics warehouse worth $40 million. It generates $2.8 million in annual net operating income (7% cap rate). You want to tokenize 25% — $10 million — to raise capital without selling the asset.

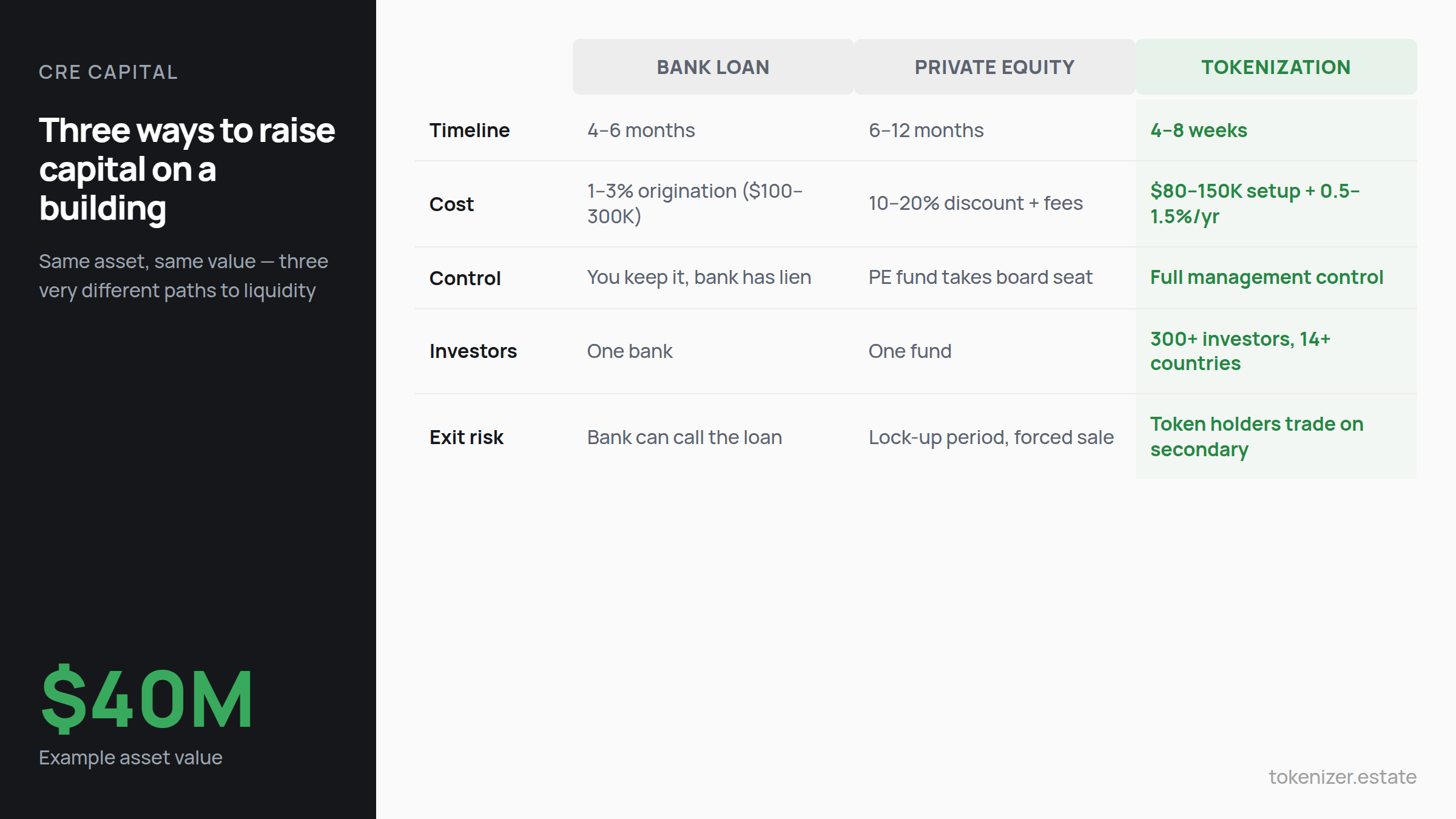

Setup costs: Legal structuring, smart contract development, KYC/AML infrastructure, platform integration — roughly $80,000 to $150,000, depending on jurisdiction and complexity.

Ongoing costs: Platform fees, compliance monitoring, investor relations — typically 0.5% to 1.5% of the tokenized amount per year. On $10 million, that is $50,000 to $150,000 annually.

Time to market: 4 to 8 weeks from decision to first investor dollar, compared to 6–12 months for a traditional private placement or bank refinancing.

Investor returns: The 25% ownership stake entitles token holders to $700,000 per year in distributions (25% of $2.8M NOI). At a $10 million raise, that is a 7% cash yield. If the property appreciates and is sold later, token holders receive their proportional share of the proceeds.

The real advantage for the owner: You raised $10 million in working capital in under two months, kept 75% ownership, maintained full management control, and did not give a bank a lien on your building or a PE fund a board seat. You now have 300 investors from 14 countries who are aligned with your success because they earn when the building earns.

Compare this to a traditional refinancing: 6 months of paperwork, 1–3% origination fee ($100K–$300K), a bank that can call the loan, and no new investor relationships. Or a PE fund that takes 12 months of due diligence, demands 10–20% discount to appraised value, and installs their own reporting requirements.

Tokenization is not free. But the speed, the cost, and the control structure are fundamentally different.

For a broader view of how these deals flow across issuance platforms, custody, and secondary markets, the market map on the Tokenizer blog explains the full ecosystem.

What still does not work — the honest version

Every serious article about tokenization should include this section. Here is what is still hard.

Liquidity is real but thin. Having a token does not guarantee you can sell it today at the price you want. Secondary markets for tokenized CRE exist — tZERO processed $200 million in CRE tokenizations in 2025, RedSwan runs its own marketplace — but daily volumes are still measured in dozens of trades, not thousands. This is improving. But anyone who tells you tokenized CRE has stock-market liquidity is not being honest.

Regulation is fragmented. A tokenized office building in New York follows SEC rules (Reg D or Reg A+). The same deal in Frankfurt follows MiFID II. In Dubai, VARA. In Singapore, MAS. There is no global standard yet. Cross-border distribution works but requires careful legal structuring per jurisdiction.

Default scenarios are untested. If a tokenized building defaults on its mortgage, what happens? Can the lender seize the physical asset while token holders have claims on the SPV? Deloitte itself flagged this as one of the key unresolved questions: the link between on-chain tokens and off-chain legal enforcement needs more real-world testing.

The education gap is real. Most commercial real estate brokers, lenders, and appraisers do not understand tokenization yet. This slows adoption. The industry needs fewer buzzwords and more completed deals. Every successful deal — like RedSwan-Altus — makes the next one easier to explain and execute.

Stay current with tokenization deals and regulatory changes at Tokenizer.Estate News.

Who should move now — and who can afford to wait

If you own or manage commercial real estate — offices, warehouses, data centers, industrial facilities, hotels, mixed-use buildings — tokenization is now a real capital strategy. Not for every deal. Not for every market. But for the right asset, at the right time, with the right structure, it is faster, cheaper, and more flexible than any traditional alternative.

If you run a family office or control significant assets — whether commercial buildings, logistics operations, marinas, or industrial plants — tokenization gives you a way to unlock value without selling and without losing control.

If you are a fund manager launching a new vehicle, a tokenized structure gives you something traditional funds cannot: built-in secondary liquidity and global distribution from day one.

And if you are sitting on a $40 million building, generating solid rent, with capital locked inside — the math is straightforward. You can spend six months negotiating with one bank, or you can spend six weeks reaching hundreds of investors who want exactly the exposure your building provides.

The infrastructure is built. The regulation is live. The deals are closing. The only question left is timing.

For a comparison of tokenization platforms across jurisdictions and asset types, read our platform comparison guide.

This article is for informational purposes only and does not constitute legal, tax, or investment advice. Commercial real estate investments carry risk including loss of capital. Always consult qualified professionals before making structuring or investment decisions.