Tokenized Real Estate: A Decision Framework for Single-Asset vs. Diversified Fund Tokenization

A practical framework for fund managers choosing between single-asset and diversified fund tokenization — covering legal wrappers, issuance costs, secondary liquidity, and operational risks, with real numbers from live platforms.

This article is for fund managers, asset allocators, and real estate operators evaluating whether to tokenize a property or a portfolio — and choosing between two structurally different approaches before committing capital and legal budget.

The decision between tokenizing a single trophy asset and tokenizing a diversified property fund determines your regulatory path, your cost structure, your investor base, and the operational risks you inherit. This article maps the trade-offs between both approaches, drawing on verified transaction data from platforms operating across the US, EU, Switzerland, Singapore, and the Middle East.

Key takeaways

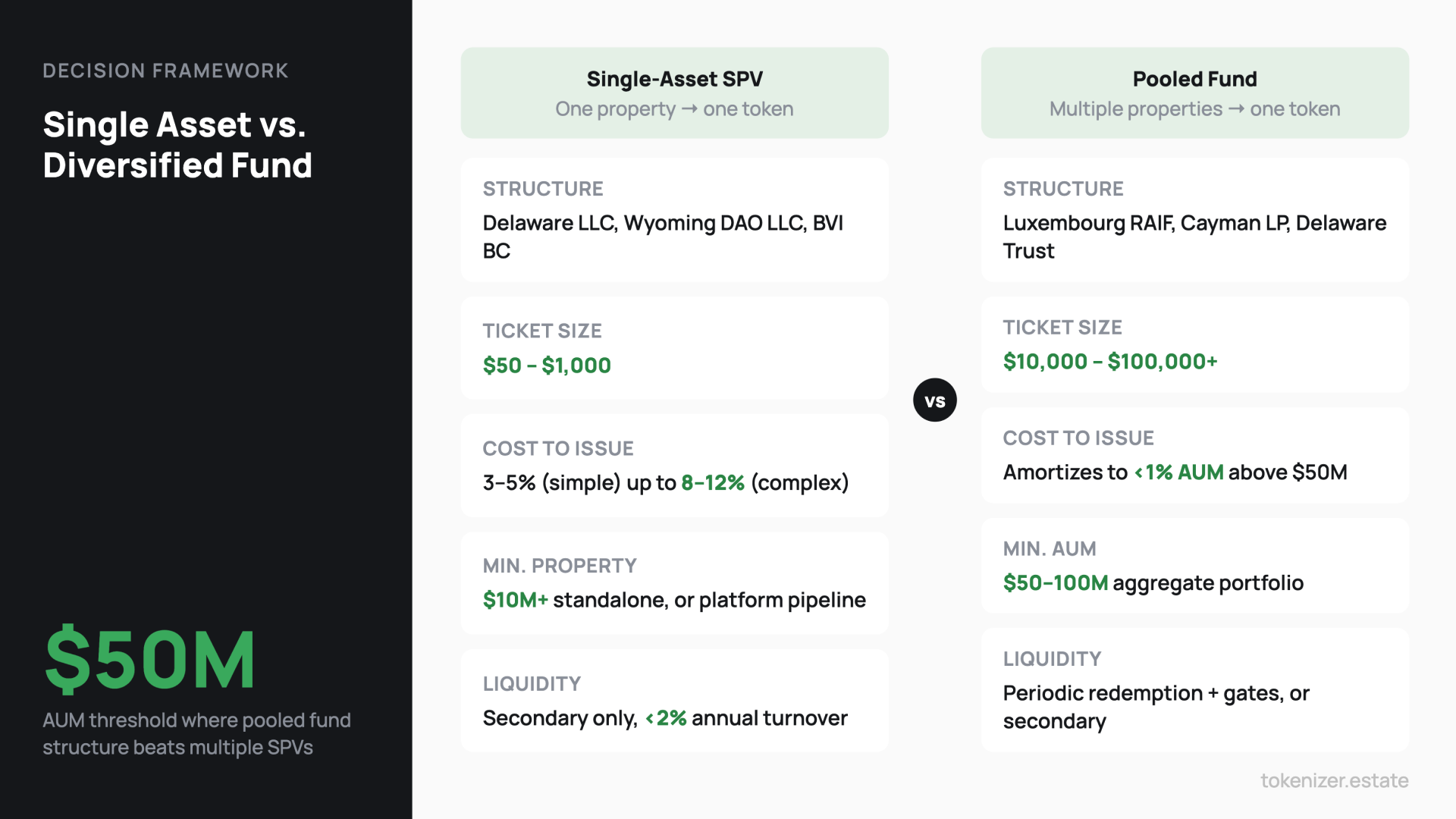

- Single-asset tokenization works economically only above $10 million in property value — or through a standardized platform that has already absorbed the per-deal legal and technical costs. Below that, structuring costs consume 8%–12% of the raise.

- Pooled fund tokenization becomes efficient above $50–$100 million in aggregate AUM. At that scale, administration amortizes to under 1% of assets annually — competitive with traditional PE real estate. The value proposition is access: Hamilton Lane cut its minimum ticket by 12.5x, Investcorp by 25x.

- Tokenization is not an alternative to REITs or LP structures — it is a distribution and compliance layer on top of existing legal wrappers. It outperforms traditional private placement when the issuer needs a global accredited investor base, programmable transfer restrictions, and automated distributions. It underperforms when secondary liquidity is critical.

- Current secondary turnover on tokenized real estate sits below 2% annually — better than unlisted LP interests, far below public REITs. The gap is narrowing in the fund segment as institutional platforms scale.

- Cross-border tax structuring can save 15–25 percentage points on withholding — but only if the wrapper is chosen correctly at the outset.

What a tokenized real estate offering actually is

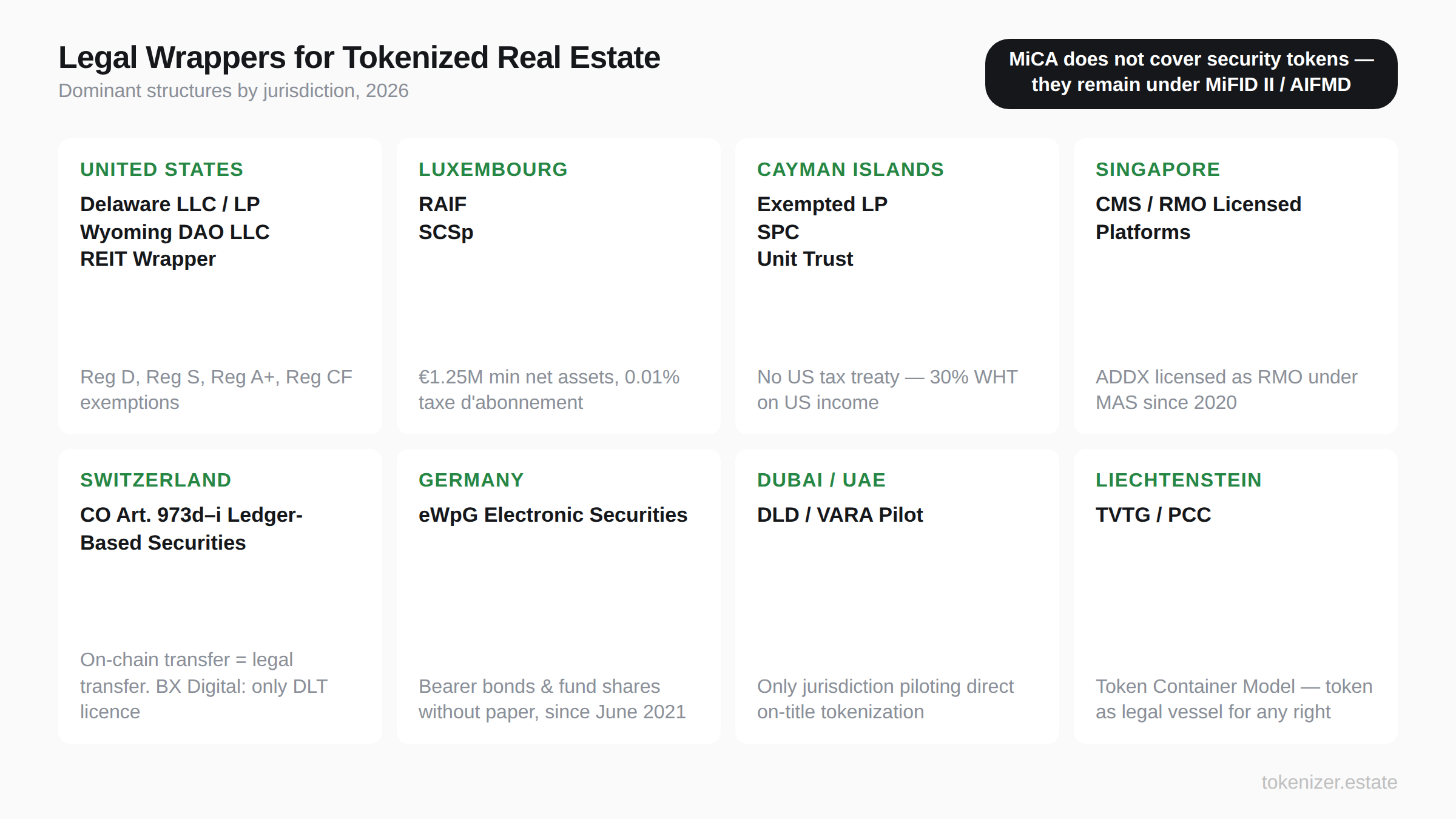

A common misunderstanding needs clearing up before anything else. Tokens never represent direct real-property title in virtually any jurisdiction worldwide. Title is held by a legal entity — an SPV, fund, trust, or foundation — and the token represents a membership, equity, debt, or beneficial interest in that entity. The enforceable legal chain runs four layers deep: investor to token to legal entity to land-registry title. Dubai's DLD/VARA pilot program (2024–25) is the notable experimental exception; every other jurisdiction requires an intermediate legal wrapper, as the SEC confirmed in its 2025 staff statement on tokenized securities.

This matters once you start thinking about what "fractional ownership" actually confers. Holders own equity in an SPV — LLC interests, preferred shares, debt instruments — they don't appear on the deed. RealT investors discovered this in 2025 when tokens purported to represent properties that RealT had never completed purchasing; the deed showed a different owner, as Outlier Media reported. "Fractional ownership" almost never means co-ownership. Dubai is notable precisely because it is exceptional.

The SEC's 2025 staff statement treats distributed ledger technology as a recording format, not a legal status change. Offerings must still be registered under the Securities Act of 1933 or qualify for an exemption — Reg D, Reg S, Reg A+, or Regulation Crowdfunding. Howey applies. Broker-dealer rules apply. Transfer-agent rules apply. The Fed, OCC, and FDIC confirmed in their joint FAQ of March 2025 that capital treatment is technology-neutral: a tokenized security receives the same capital treatment as its non-tokenized equivalent.

In Europe, MiCA (Regulation (EU) 2023/1114), fully applicable to crypto-asset service providers since December 30, 2024, explicitly does not cover tokenized financial instruments. Security tokens and fund units remain under MiFID II, AIFMD, and UCITS. Germany's eWpG (in force since June 10, 2021) allows tokenized bearer bonds and fund-share certificates without paper. Switzerland permits ledger-based securities under CO Articles 973d–i, where on-chain transfer equals legal transfer — but only if the token meets specific functional requirements, and retail secondary trading requires a FINMA DLT Trading Facility licence. As of 2026, BX Digital is the only holder of that licence.

Why single-asset tokenization is structurally more expensive than it looks

Single-asset tokenization means one SPV per property. The most common vehicles are the Delaware LLC (valued for Chancery Court precedent and flexible operating agreements), the Wyoming DAO LLC (Wyo. Stat. §17-31, with algorithmically recognized management), BVI business companies, and Cayman exempted companies. RealT uses a Delaware series LLC structure under 6 Del. C. §18-215(b), where each property sits in its own series — for example, "Series #1-9943 Marlowe" — with interests split into roughly 1,000 ERC-20 tokens and rent distributed in DAI or USDC. Lofty uses a Wyoming DAO LLC per property on Algorand, with tokens at $50 each and a 60% supermajority required for governance votes.

The economics need context. All-in first-year costs for a single-asset tokenization typically run 3%–5% of the raise for a straightforward US Reg D structure, and can reach 8%–12% for complex multi-jurisdictional deals. That is comparable to a traditional mid-size IPO (about 7% in underwriting per Cornell Real Estate Review), but with a structural advantage: once the platform pipeline is built, marginal cost per additional property drops significantly. RealT amortizes legal and technical overhead across 500-plus properties. Lofty does the same across 150-plus. The cost is front-loaded; the efficiency compounds.

Industry consensus places the minimum viable property value at $10 million for standalone commercial deals. Below that, the cost-to-capital ratio breaks the economics. The calibration points are real: Harbor's Hub at Columbia targeted $20 million (955 units at $21,000 each) before it was cancelled. Elevated Returns tokenized $18 million in equity out of approximately $262 million in asset value for the St. Regis Aspen, as its Reg A+ filing shows. Residential single-family tokenization — the RealT and Lofty model — only works through standardized platform pipelines that amortize per-property costs across hundreds of deals.

A pattern worth noting: the Aspen's $18 million tokenized raise cost an estimated 10%+ of capital once platform, legal, transfer-agent, and broker-dealer fees were included — higher than a comparable traditional raise. But it also opened the asset to a global accredited investor base that a conventional private placement would not have reached, and created a transferable digital security with secondary-market potential. The trade-off is real: higher upfront cost in exchange for broader distribution and programmable compliance. Whether that trade-off works depends on the size of the raise and whether the platform has already built the infrastructure.

How the diversified fund model actually works across jurisdictions

Diversified fund tokenization pools multiple assets into a single vehicle. The token represents a fund unit or share. The dominant structures worldwide are the Luxembourg SCSp or RAIF (under the Law of July 23, 2016, requiring €1.25 million minimum net assets within 24 months, with a 0.01% taxe d'abonnement), the Cayman unit trust or exempted limited partnership, the Delaware LP or LLC, or a tokenized REIT wrapper, per the CSSF registry.

The canonical benchmark is Hamilton Lane's Global Private Assets Fund, which tokenized a share class on ADDX in Singapore (licensed as a Recognized Market Operator under MAS since February 2020), cutting the minimum ticket from $125,000 to $10,000 — a 12.5x reduction — in March 2022. That is the core value proposition of fund tokenization: institutional-quality product, accessible at a fraction of the traditional minimum. Investcorp did the same with a US real estate fund — $150 million in AUM, over 2,200 units across Sun Belt markets — dropping the entry from $500,000 to $20,000, a 25x reduction, as Securities.io reported.

Practitioner consensus puts the threshold at roughly $50 million to $100 million in aggregate AUM before a pooled structure beats multiple SPVs. Below this, single-asset SPVs preserve underwriting transparency and avoid fund-level fee drag. A Luxembourg RAIF is typically sub-scale below €20–30 million in AUM — at that size, the fixed costs of an authorized AIFM and depositary represent too high a percentage of assets. Above that threshold, the same costs amortize to under 1% of AUM annually, which is competitive with traditional PE real estate fund administration (1.5%–2%).

NAV calculation is where the structural difference bites hardest. Single-asset tokens track one-to-one with the underlying property; each independent appraisal adds cost and happens only quarterly or annually — no diversification smoothing. Fund structures use administrator-calculated NAV across the portfolio, monthly or quarterly, spreading appraisal costs across dozens of assets. Chainlink's on-chain NAV feeds are now used by Fidelity International and Sygnum and in the UBS–Swift–Chainlink Project Guardian pilot. But there is a critical caveat: Chainlink Proof of Reserve "only ensures that data from centralized entities is not tampered with before it makes it on-chain" — it does not validate the credibility of the underlying attestation, as CoinDesk noted in July 2023.

Redemption is structurally asymmetric between the two models. Single-asset tokens typically offer no issuer redemption — exit means finding a buyer on a secondary market or waiting for a refinance or sale. Fund structures may offer periodic redemption with gates, queues, and side-pockets (the standard AIFMD toolkit), though closed-ended commercial real estate funds offer none. Tokenization itself neither adds nor subtracts redemption rights.

How secondary liquidity actually works in tokenized real estate

The most common misalignment in tokenized real estate is between tradability and liquidity. A token can be transferred 24/7; that does not mean a counterparty is available.

Secondary volumes remain thin relative to traditional markets. In March 2021, the combined monthly turnover across all tokenized real estate on all alternative trading systems was less than 0.1% of aggregate market cap, with a single token (Aspen Coin) accounting for 83% of all volume, per STM Data.

RealT — with roughly 500 properties, about 16,000 investors across 150-plus countries, and peak AUM of $130–$150 million — showed annual secondary turnover below 2% in late 2022. Bid-ask spreads frequently run 2%–5%, based on Gnosisscan on-chain data and WIRED reporting. Lofty shows tighter spreads of 1%–4% on active listings, widening to 5%–10% on less liquid ones per Algorand's insights. For context: a listed REIT typically trades at sub-1% spreads with daily turnover orders of magnitude higher.

An arXiv analysis published in 2025, covering more than $25 billion in tokenized real-world assets, concluded that most tokenized assets continue to exhibit low trading volumes, long holding periods, and limited secondary-market activity. RealT's implied annual turnover sits below 2%; investor self-reports indicate typical holding periods exceeding two years. The practical rule is to treat tokenized real estate liquidity as incrementally better than unlisted LP interests — not comparable to public REITs.

This does not mean the liquidity gap is permanent. US REITs traded thinly for years after the 1960 enabling legislation; meaningful institutional liquidity arrived only after the Tax Reform Act of 1986 and the REIT Modernization Act of 1999 expanded the eligible investor base and operating flexibility. Tokenized real estate is arguably at its own pre-1986 stage — infrastructure exists, volumes do not. The relevant question is whether regulatory clarity, institutional adoption (BlackRock, Franklin Templeton, Fidelity International are already active in tokenized funds), and market-maker economics converge fast enough to pull secondary volumes upward. Early signs in the fund segment are more encouraging than in single-asset tokens.

A separate dynamic is worth acknowledging. The first wave of retail tokenized real estate investors is predominantly crypto-native. RealT accepts only cryptocurrency and bars US residents. Lofty users arrive via Discord and decentralized exchanges. The overlap is largely with ETH holders seeking yield-bearing collateral. But this is a feature of early adoption, not a ceiling. Institutional entry — BlackRock's BUIDL, Hamilton Lane on ADDX, Apollo and VanEck via Securitize — is already broadening the investor base beyond crypto natives. The distribution channel for tokenized funds is converging with traditional alternative-asset distribution; single-asset retail platforms have not yet made that transition.

Operational risks after the raise closes

The operational risks that matter most in tokenized real estate are the ones that become visible after the capital is committed. They differ depending on the structure chosen.

Single-asset deals are exposed to key-man risk, property management disconnect, and SPV governance deadlocks. The St. Regis Aspen carries a 50-year Marriott/Starwood management contract that token holders cannot renegotiate. The RealT case in Detroit illustrates the extreme end of this spectrum: over 100 vacant properties, millions in unpaid property taxes and utility bills, and acquisitions that were never completed — none of which was visible on-chain despite real-time dividend transparency, as Outlier Media and the Wayne County Circuit case record document.

It is worth separating the operator from the model. RealT's failures are failures of property management, tax compliance, and sponsor accountability — none intrinsic to tokenization. Lofty operates over 150 properties across 40 US markets without analogous enforcement actions; RedSwan tokenizes institutional-grade commercial assets with third-party management. The broader lesson is that on-chain transparency covers the financial layer but not the operational one — and this gap exists in any SPV-based real estate structure, tokenized or not.

Fund structures face different risks: NAV manipulation through sponsor-paid appraisers with no forcing mechanism between market bid and appraisal, platform dependency when tokens are tradeable on only one ATS, and compliance drift as regulations compound year over year. The platform landscape has consolidated significantly since 2018, which is a normal pattern for any emerging financial infrastructure — not a sign that tokenization itself is failing. Harbor was acquired by BitGo (February 2020), OpenFinance was absorbed by INX (June 2021), Meridio folded into ConsenSys's Codefi (March 2020), and Polymath pivoted to Polymesh (May 2019). What matters is that the survivors — Securitize, ADDX, tZERO — are now more capitalized, better regulated, and processing materially larger deal flow than any first-generation platform managed. Securitize is going public via SPAC at $1.25 billion pre-money valuation. That trajectory is closer to fintech maturation than to market failure. Still, the practical risk for any issuer choosing a single platform today is real: Aspen Coin migrated from Templum to Securitize to tZERO with KYC re-onboarding required each time. Multi-venue issuance and transfer-agent independence from the ATS remain the best structural mitigants.

Smart contracts introduce an additional legal coordination layer. Every tokenized deal requires securities counsel, corporate counsel, blockchain counsel, tax counsel for cross-border structures, platform legal integration, and smart-contract audits. This is a cost of doing it properly — not a sign that the model is flawed. Elevated Returns' Aspen deal took "more than a year" on legal structuring alone.

Current market size and growth trajectory

The spread between industry projections and current market size is wide — and worth understanding in context. McKinsey's June 2024 base case projected approximately $2 trillion in tokenized assets by 2030, with a bull case of $4 trillion. BCG and ADDX (2022) projected $16 trillion by 2030. Deloitte (2025) estimated tokenized real estate specifically could grow from under $0.3 trillion in 2024 to $4 trillion by 2035, a 27% CAGR. Citi (2023) landed at $4–$5 trillion in tokenized digital securities by 2030. The range reflects genuine uncertainty about adoption pace, not disagreement about direction. We analyzed these projections and their underlying assumptions in detail in our RWA tokenization forecast.

Current verified reality as of April 2026: total active tokenized real estate on public chains remains below $1 billion. The top tokens by size are GRO at $68.2 million, RSR at $27.3 million, ALTUS at $25 million, and VIZI at $23 million, per RWA.xyz. For comparison, tokenized Treasuries exceed $9 billion and private credit exceeds $18.9 billion. The tokenized fund segment — dominated by BlackRock's BUIDL at $2.5–$2.9 billion, Hamilton Lane, Apollo, VanEck, and Franklin Templeton — is real and scaling. Single-asset real estate tokenization is still early, at under $1 billion — but the fund segment is demonstrating that the infrastructure works at institutional scale.

The Financial Stability Board concluded in 2024 that tokenization activity remains small-scale but noted liquidity mismatch, oracle dependency, and cross-border legal uncertainty as areas requiring attention as the market scales.

Cross-border tax and compliance

Wrapper choice directly affects investor returns: a Cayman fund distributing US rental income faces 30% withholding; a properly structured Luxembourg SICAV-SIF can reduce this to 5%–15%, as the IRS treaty table confirms. Since DAC8 and the EU Transfer of Funds Regulation took effect, compliance costs compound 10%–20% annually — making it the category most often underbudgeted.

When tokenization outperforms traditional alternatives

Tokenization is not a replacement for REITs, LP structures, or direct investment — it is a distribution and compliance layer that sits on top of the same legal wrappers. The conditions under which it objectively outperforms traditional channels are specific. Tokenization wins when the issuer needs to reach a global accredited investor base that domestic private placement cannot access — Hamilton Lane's 12.5x ticket reduction is the clearest example. It wins when the fund manager wants programmable transfer restrictions and automated compliance (KYC/AML whitelist enforcement, automated distributions in stablecoin) that reduce ongoing administrative overhead at scale. And it wins when the asset is illiquid by nature and the marginal liquidity improvement from secondary-market transferability — even at 2% annual turnover — is an upgrade over a locked 7–10 year LP commitment with no exit.

Tokenization loses when the issuer needs deep, reliable secondary liquidity (public REIT is the better vehicle), when the investor base is domestic and accredited (traditional Reg D placement is cheaper), or when the asset is a single property below $10 million (the structuring costs consume too much capital). The question is not "tokenization vs. traditional" — it is which specific friction tokenization removes in your specific deal, and whether the removal is worth the added structuring layer.

The hard takeaway

Below $50 million in AUM, tokenize individual assets only through a standardized platform pipeline that has already amortized the per-deal legal and technical costs. Above $50 million, a pooled fund structure under an established regulatory wrapper — Luxembourg RAIF, Cayman LP, or Delaware statutory trust — will deliver lower per-dollar costs, broader investor eligibility, and more defensible compliance. Neither structure solves the liquidity problem on its own, and neither protects against off-chain operational failures.

That sentence should inform the go/no-go conversation. A fund manager evaluating tokenization in 2026 is not choosing between innovation and tradition. The infrastructure works — Securitize is processing billions, ADDX is onboarding institutional funds, ERC-3643 is the dominant compliance standard, and regulators from the SEC to CSSF to MAS have built workable frameworks around security tokens. The choice is between two cost structures, two regulatory paths, and two sets of failure modes — with the understanding that on-chain transparency covers the thinnest layer of the operational stack. The question to ask is not "should we tokenize?" but "which structure matches my portfolio size, investor base, and operational capacity — and what does it cost to get wrong?"