How tokenized property is valued: appraisals, NAV, and the lag nobody warns you about

Every tokenized property has a hidden number behind it — the valuation. The token can move every minute, but the appraisal under it usually moves once a year. This guide explains how the valuation actually works, where it breaks, and what to ask before you tokenize an asset or invest in one.

There are now hundreds of platforms tokenizing real estate, hotels, yachts, and industrial assets. Most articles about tokenization focus on what is loud — bigger investor pools, instant liquidity, fractional ownership starting at fifty dollars. The quiet part, the one almost nobody covers in plain English, is how the property gets valued in the first place.

A token is just a wrapper. What gives it meaning is the value of the building, the marina, the factory, or the hotel sitting under it. If that value is wrong, late, or unclear, the token loses its anchor. Every promise about transparency, liquidity, and global investors depends on this one quiet step.

This article walks through how tokenized property is actually valued in 2026 — the methods, the standards, the role of NAV, the role of oracles, and the lag problem that catches new asset owners off guard. The goal is to give you a clear map before you sign anything.

Two layers of valuation — and why they almost never match

Before we get into methods and standards, you need to understand the basic split inside every tokenized property deal. There are two values for any token, and they are produced in completely different ways.

The first is the off-chain valuation — the appraisal of the underlying property by a professional valuer, usually under standards like the RICS Red Book or local equivalents. This is the legally binding number. It is what auditors, regulators, banks, and tax authorities will look at. It is produced once a year, sometimes twice, occasionally quarterly. It is slow, careful, and expensive.

The second is the on-chain price — the number at which tokens actually trade between buyers and sellers on a secondary marketplace. This price moves every time a trade happens. It can be hourly, daily, or weekly, depending on liquidity. It reflects what people are willing to pay right now, not what an appraiser said six months ago.

These two numbers almost never match exactly, and they are not supposed to. Understanding why is the first step in understanding tokenized real estate valuation.

The off-chain valuation answers the question: what is this asset worth on paper, under professional standards? The on-chain price answers a different question: what will someone pay for a small piece of it today? These are not the same question, and the difference between them is where most of the interesting things in tokenization happen.

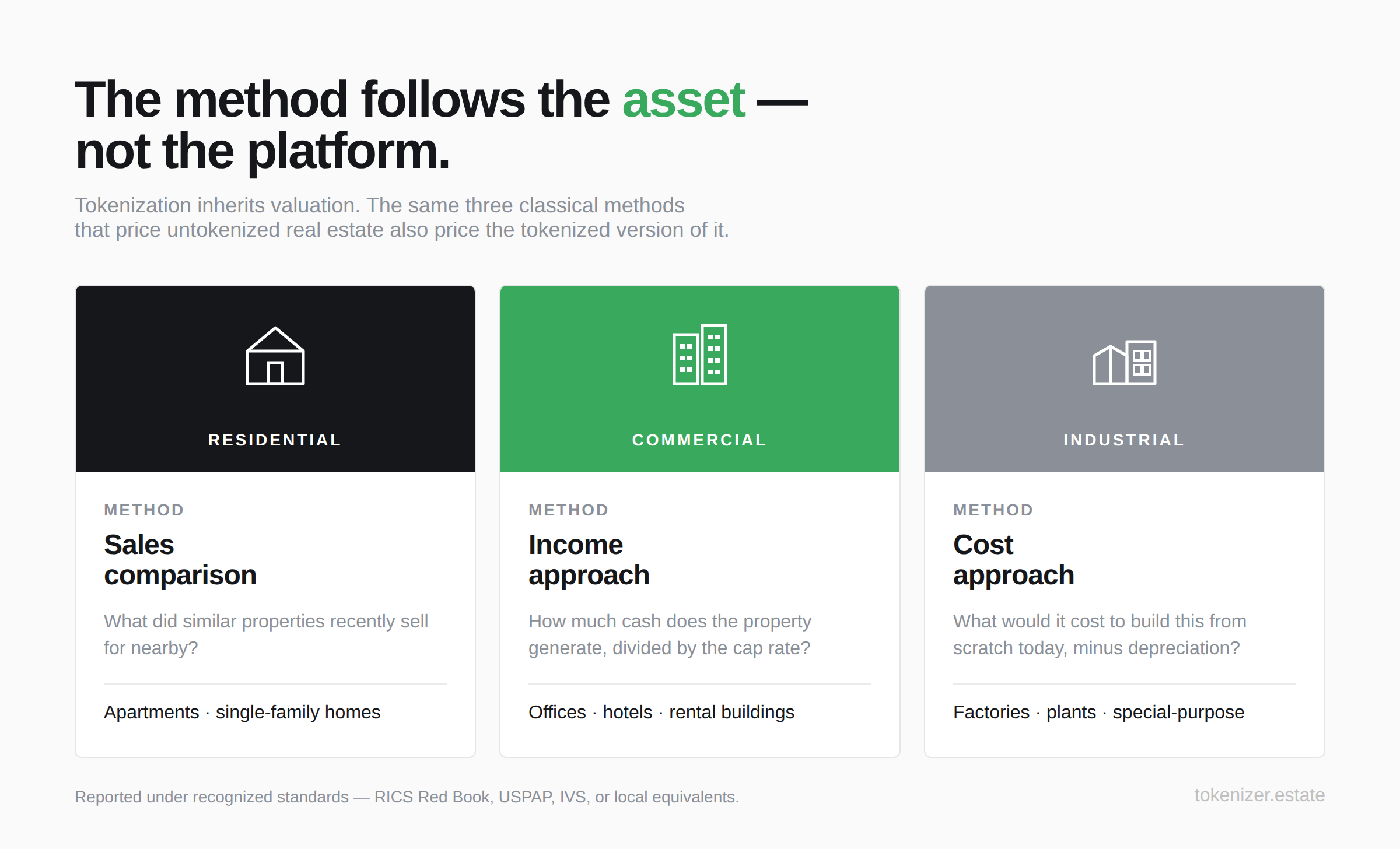

The three valuation methods that still rule everything

Here is something that surprises people new to tokenization: blockchain did not invent a new way to value buildings. The methods used to value a tokenized warehouse in Rotterdam are the same methods used to value an untokenized warehouse in Rotterdam. Tokenization inherits the valuation; it does not replace it.

There are three classic methods, and every property — tokenized or not — gets valued using one or two of them.

The sales comparison approach looks at recent sales of similar properties nearby and adjusts the price up or down for differences. This works well for apartments, single-family homes, and standard buildings in active markets. It works poorly for unique assets — a custom superyacht or a private marina has no real comparables. It is the most common method for residential property worldwide.

The income approach values a property based on the cash it generates. The valuer takes Net Operating Income and divides it by the cap rate — the return investors expect for that asset class in that location. This is the main method for offices, hotels, rental buildings, and most commercial real estate. A small change in the cap rate can move the value by millions, which is why this method is sensitive to market mood and interest rate cycles.

The cost approach estimates what it would cost to build the property from scratch today, then subtracts depreciation. This is used for special-purpose buildings — factories, schools, industrial plants — where neither sales data nor income data is reliable.

For most tokenized commercial real estate, the income approach dominates. For tokenized residential, sales comparison rules. For tokenized industrial assets and unique properties, cost approach often steps in. The platform does not change which method applies; the asset does.

When the valuer signs the report, they usually do it under a recognized standard. The most common one globally is the RICS Red Book Global Standards, updated and effective from 31 January 2025. The Red Book sets the rules for how valuers must work, what they must disclose, and how often they must rotate off an asset. Under the latest rules, the same individual valuer cannot value the same asset for more than five years in a row, and the same firm cannot value it for more than ten years. This is to keep them honest, regardless of whether the asset is tokenized or not.

NAV vs token price — the gap that confuses everyone

So the property has a value. How does that turn into a token price?

In the middle sits a number called Net Asset Value, or NAV. NAV is straightforward in concept: take the fair value of the property, subtract the debt, subtract any planned capital expenses, and divide by the number of tokens outstanding. That is what each token represents in terms of the underlying asset. NAV is calculated and reported by the fund administrator on a fixed schedule — quarterly is most common for real estate funds, sometimes monthly, sometimes annually for smaller deals.

The market price of the token is what people actually pay for it on a secondary market. This is set by buyers and sellers, just like the price of an ETF or a stock. It can be higher than NAV (a premium) or lower (a discount).

Here is the part that confuses new entrants: NAV and market price are not supposed to be identical. Even in well-run, regulated markets, they drift apart. A token can trade at 95 cents on the dollar of NAV one week and at 1.05 the next, and that doesn't mean anyone is doing anything wrong. It means the market is pricing in liquidity, sentiment, and any uncertainty about whether the official NAV is current.

In traditional private real estate funds, secondary buyers have averaged discounts of around 30% to NAV since 2022, according to Jefferies' Global Secondary Market Review. That is for non-tokenized funds, where redemptions are gated and exits take months. Tokenized real estate has shown a noticeably different pattern in some cases — tokens have actually traded at small premiums to NAV in 2025 because instant liquidity is genuinely valuable, while traditional funds remain stuck at quarterly redemption windows or worse.

This is one of the more honest wins for tokenization. When liquidity exists, the discount narrows or even disappears. The token price stops being a hostage to redemption queues.

But this only holds when there is real trading volume. A tokenized property with thin liquidity will trade at a discount, sometimes a deep one, regardless of how good the NAV calculation is. We covered this dynamic in detail in our framework for single-asset vs. diversified fund tokenization, where the link between liquidity depth and price stability becomes obvious.

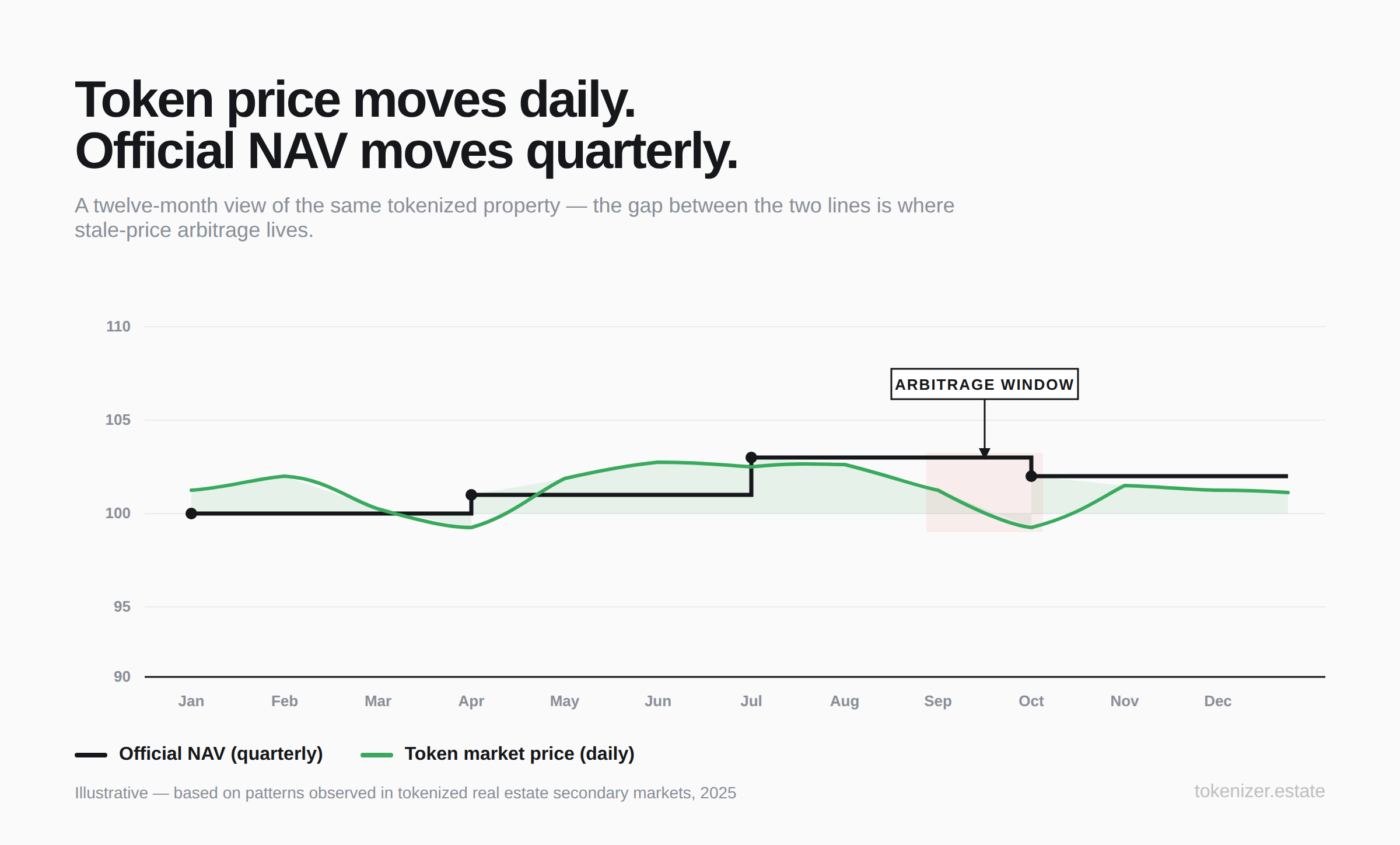

The lag problem — slow appraisals on fast rails

Here is where things get harder, and where most asset owners get caught off guard.

A traditional property appraisal happens once a year. A token can be traded every minute. So you have a fast price layered on top of a slow value. When the property market moves, the token price reacts within hours. The appraisal stays still for months.

This gap is called valuation lag, and it is the single most underestimated risk in tokenized real estate. It is not a bug in the blockchain. It is a feature of how property has always been valued. The blockchain just makes the gap visible to everyone, in real time, with timestamps.

When the property market drops sharply, holders of tokens see the token price fall, but the official NAV stays at the old, higher level. Sophisticated traders can spot this and arbitrage it: buy tokens at the discounted secondary price, then redeem them at the stale, higher NAV if the platform allows redemption. This is called stale-price arbitrage, and it is well documented in mutual funds. It now shows up in tokenized funds too. Chainlink describes the problem clearly in its NAV data piece — without timely NAV updates, protocols can issue tokens at the wrong price, diluting existing holders.

This is why frequency of revaluation matters more than people realize. A property valued once a year inside a token wrapper is technically fine but practically risky. A property valued quarterly is better. A property where cash flow and key inputs are tracked monthly, and the appraisal is refreshed at least every six months, sits much closer to what serious institutional investors expect.

There is no universal standard yet for how often a tokenized property should be revalued, but the direction is clear. Markets reward platforms that update more often. They punish the ones that hide behind annual appraisals while pretending to offer real-time pricing.

What oracles actually do — and what they don't

You will hear a lot about oracles and Chainlink in tokenization marketing. The pitch is usually that oracles solve the valuation problem by bringing real-world data on-chain in real time.

This is partly true and mostly misleading.

An oracle is a piece of software that takes information from the off-chain world and writes it onto the blockchain so smart contracts can use it. Chainlink runs a service called SmartData that delivers NAV figures, reserve data, and other financial information directly to tokenized fund contracts. This is real, it works, and major institutions use it for tokenized treasuries and money market funds.

But the oracle does not check whether the value is correct. It only checks that the value reported by the fund administrator was published faithfully on-chain. If the administrator reports a NAV based on a six-month-old appraisal, the oracle will deliver that six-month-old number to the blockchain with high precision and a beautiful timestamp. The data is fresh in transmission but stale in content.

Oracles are necessary but not sufficient. They are part of the technical pipeline that connects the off-chain valuation to the on-chain token, and we explained how that pipeline fits together in our piece on KYC/AML and on-chain compliance for tokenized securities. They are one of the layers that make tokenization technically possible. They are not a substitute for good appraisal practice.

For owners deciding whether to tokenize, this means one thing: the quality of your tokenized asset is set by the quality of your appraiser, your administrator, and your valuation policy. The smart contracts and the oracles sit downstream. They cannot fix bad inputs.

Automated valuation models — useful, but not for everything

Some platforms try to close the lag by using Automated Valuation Models, or AVMs. These are software tools that estimate property value based on comparable sales, location data, and market trends, sometimes updated daily or even hourly.

AVMs are used heavily by mortgage lenders and online property platforms. For ordinary residential homes in busy markets, they perform reasonably well. Industry research summarized by Bankrate's AVM overview shows that around 70% of US residential AVM outputs land within 10% of true value on average. That sounds decent until you look closer: in some counties, only 20% of estimates fall in that 10% band, while in others over 90% do. Accuracy depends entirely on local data quality and transaction volume.

AVMs also do something useful that human appraisers don't always do well: they remove personal bias. One US study found that 44.9% of residential refinance appraisals came in at least 5% higher than the matching AVM estimate. Appraisers are not always wrong, but they are sometimes optimistic when the client pays them. Algorithms don't care.

The problem is that AVMs work poorly outside of generic residential markets. They cannot value a 200-room hotel in the Maldives, a chemical plant in Houston, or a fishing fleet in Norway. They cannot inspect the building. They cannot see that the roof needs replacing. They cannot tell you the anchor tenant just gave notice.

For commercial real estate, hospitality, industrial assets, yachts, and other unique properties, an AVM is at best a useful indicator between formal appraisals. It should never replace a Red Book valuation as the binding number. Most serious tokenization platforms use a layered approach — a formal appraisal at fixed intervals, AVM-based pricing in between for transparency, and clear disclosure to investors about which is the legally meaningful number.

What regulators expect from valuation

If you tokenize through a fund structure in Europe, you will likely fall under the Alternative Investment Fund Managers Directive, known as AIFMD. Article 19 of AIFMD sets specific rules: the fund manager is fully responsible for proper and independent valuation. The manager can hire an external valuer, but the manager stays liable to investors no matter what.

This is the part many tokenization founders misunderstand. Hiring a famous valuation firm does not transfer the risk. If the NAV is wrong, the fund manager is on the hook, not the valuer. In practice, this is why most real estate funds in Europe use external valuers in an advisory role, while the manager keeps the final word on NAV. Few valuation firms are willing to accept the unlimited liability that a strict reading of AIFMD would require.

The fund's depositary also has an independent duty to verify that NAV per token was calculated according to the fund's stated procedure. This is a quiet but powerful safeguard. If the procedure says quarterly Red Book valuations and the manager skips one, the depositary should flag it.

Other jurisdictions have similar but not identical frameworks. The US relies on USPAP standards and SEC rules for funds. Singapore uses RICS-aligned standards. Brazil has its own rules from CVM and COFECI. Pakistan recently told tokenization pilots to seek approval first, signaling that valuation transparency will be part of any future licensing review.

The point for asset owners is simple: wherever you are, the valuation rules of the underlying asset class still apply. Tokenization does not let you skip them. It just adds a digital layer on top of the same standards that have governed property valuation for decades.

Ten questions to ask before you tokenize

Before signing with any tokenization platform, run this checklist with your prospective valuer and administrator. If you do not get a clean answer to all ten, you have not yet found a serious counterparty.

- Who is the appointed valuer, and under which standard do they sign? Red Book, USPAP, IVS, or local equivalent — and is the firm RICS-regulated or equivalently licensed?

- How long has this valuer worked on this asset? Five years for an individual and ten for a firm is the Red Book ceiling — anything close to those limits means rotation is overdue.

- What is the appraisal cadence? Annual, semi-annual, or quarterly. Anything less frequent than annual is a disqualifier for tokenized assets.

- How is NAV calculated between appraisals? Cap-rate roll-forward, AVM blending, or held flat — and who signs off on the interim number?

- Who calculates NAV — the manager, the administrator, or an independent third party? If it's the manager alone, ask why.

- Is there a depositary or independent verifier of NAV? Under AIFMD this is mandatory. Outside Europe it is a strong signal of seriousness.

- What triggers an interim revaluation? A 10% market move, loss of a major tenant, a debt covenant breach — there should be written triggers, not discretion.

- How is the on-chain NAV figure delivered — via oracle, manual upload, or signed publication? And how is its freshness timestamped?

- Is redemption at NAV permitted, and how is stale-price arbitrage prevented? Look for fair-value adjustments, gates, or anti-dilution mechanisms.

- Where is the valuation policy published? Investors should be able to read it before they buy, not request it after.

The bottom line

Tokenization is real and it works. Serious capital is moving on-chain — total real-world asset value sits above $30 billion across all asset classes as of April 2026, with tokenized real estate alone at around $444 million according to recent on-chain market data. None of that exists without working valuation infrastructure underneath.

But the technology does not solve the hard part. The hard part is producing a credible, defensible, regularly updated value for a real-world asset. That is still done by humans, with professional standards, in a process that costs real money and takes real time. Tokenization makes that value more visible and more tradeable. It does not make it easier to produce.

For an owner of a building, a yacht, a logistics park, or a hotel, the question to ask before tokenizing is not whether the smart contract works. It is whether the appraisal cadence, the valuer independence, and the gap between revaluations match what serious investors will accept.

A token wrapped around an annual appraisal will trade. A token wrapped around a quarterly appraisal with a strong valuation policy will trade better and at tighter spreads. A token where the NAV process is opaque or where the manager controls the final value without independent oversight will eventually meet a market that prices in that risk — usually at the worst possible time.

When a developer, a fund manager, or a yacht owner sits down to decide whether to tokenize, the first question is always the same: who values the asset, how often, and under what standard? Everything else — the smart contracts, the oracles, the secondary markets, the global investor base — follows from that one answer.

This article is for informational purposes only and does not constitute investment, legal, or valuation advice. Always conduct your own due diligence and consult qualified professionals before tokenizing an asset or investing in a tokenized offering.