Tokenization for Developers: How to Fund Construction with Tokens

Bank construction loans got expensive. Tokens give developers a new way to fill the mezzanine and equity gap with real investors and real money. This is the practical guide for owners of yet-to-be-built assets in 2026.

In February 2026, the Trump Organization sold tokens in a hotel that does not exist yet. The villas will be built by 2030. The investors who bought in receive a fixed yield and a share of future villa sales — all from a property that is still a plan and a piece of beachfront in the Maldives.

Five years ago this would have been a private bank loan. Today it is a token, distributed under US private placement rules to accredited investors around the world.

This deal is not unusual anymore. Banks tightened credit. Construction loan rates climbed past 11% on most US development loans, with NAHB data putting average rates above 11.77% for land development and 12.82% for speculative single-family construction in Q2 2025. Mezzanine lenders ask for 15% plus equity kickers. The deal a developer penciled at 8% two years ago does not work anymore.

Tokens fill the gap. Smaller developers and asset owners — including those with yachts, factories, and industrial sites — are starting to ask the same question: can tokens fund my project? The short answer is yes, in specific layers of the capital stack. This article covers which layers, what it really costs, and where the model breaks.

Why developers are looking at tokens in 2026

For most of the last decade, developer financing followed a simple pattern. Senior debt from a bank covered 60–70% of the project cost. Mezzanine debt or preferred equity from a private fund filled another 10–20%. The developer put in the rest.

That model is under pressure. Three things changed at once.

Bank credit tightened. Tight credit conditions ran for fourteen consecutive quarters through Q2 2025. Banks now cap senior leverage at 65–75% loan-to-cost and 65–70% loan-to-value, often less. Mezzanine lenders raised rates and demanded more equity protection. And the public market for new development bonds shrank.

At the same time, the technology stack for tokenization matured. Securitize, Tokeny, ADDX, RedSwan, Chintai, and other platforms now run compliant token issuance with KYC, transfer restrictions, and on-chain distribution as standard. Major institutions — BlackRock, JPMorgan, Apollo — issued tokenized funds at scale. The plumbing works.

For a developer, this opens a new option. Instead of negotiating with a single mezz lender for $10 million at 15%, you can issue a tokenized debt or revenue instrument to dozens or hundreds of accredited investors at 12–14%, with quarterly distributions automated by smart contract.

This is not magic. It is a different distribution channel for the same kind of capital that has always financed construction. But the channel changes who can participate, how fast the money arrives, and what the developer has to give up in return.

The asset owner does not need to be a New York skyscraper sponsor. The same logic applies to a marina developer in Croatia, a factory expansion in Poland, or a hotel operator adding a wing in Dubai. As long as the asset is real and the legal wrapper is clean, the model works.

A token does not change what gets built. It changes who pays for it.

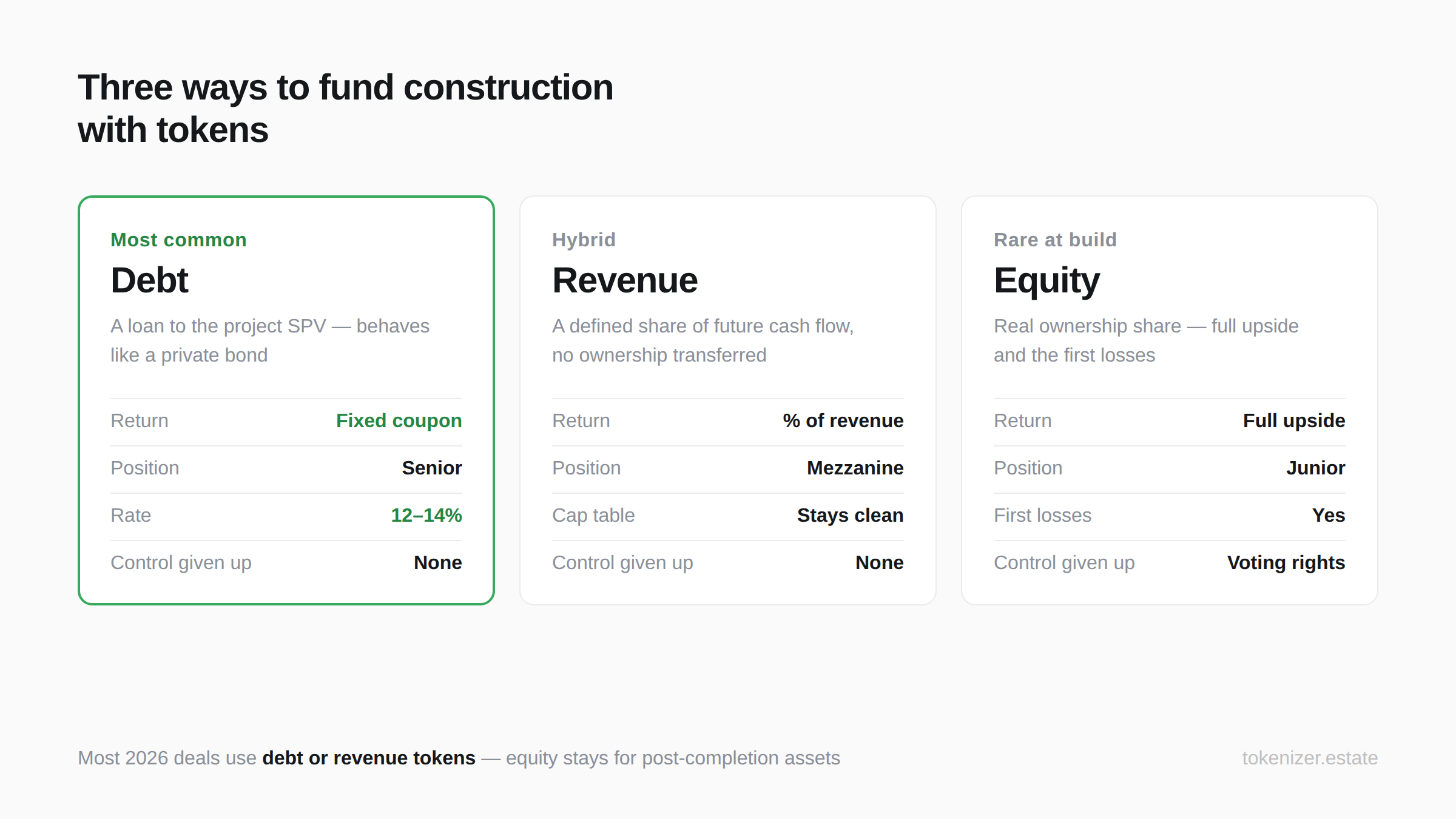

The three token types developers actually use

When a developer issues tokens to fund construction, they pick one of three instruments. Each one fits a different stage of the capital stack and a different investor.

Debt tokens are the workhorse of developer tokenization in 2026. The token represents a loan to the project SPV. Investors receive a fixed coupon, usually paid quarterly, and stand senior in the capital stack. The developer keeps full control of the project. At maturity, the principal is returned. If the project is sold or refinanced earlier, debt token holders are paid before equity holders see anything.

This is the model most developers reach for, because it looks and behaves like a private bond. Compliance teams understand it. Investors price it like fixed income. We covered the mechanics in detail in our guide on debt vs equity tokens for real estate.

Revenue participation tokens are a hybrid. The investor does not own equity, but they get a defined share of future cash flow — rental income, hotel revenue, or sale proceeds. The developer keeps the cap table clean and avoids governance rights. This works well when the project will generate revenue at completion (a hotel, an apartment building, a logistics warehouse with pre-leased space) but the developer does not want to hand over ownership.

Equity tokens transfer real ownership. Investors share the full upside if the project succeeds and the first losses if it does not. They may have voting rights on major decisions like refinancing, sale, or large capital expenditure. This is the strongest form of investor protection and the heaviest one in terms of disclosure and governance.

Most construction-stage deals in 2026 use debt or revenue tokens. Equity tokens during construction are still rare, because investors prefer to take equity exposure after completion when the asset has measurable value. Equity tokens during construction work mainly when the developer has a strong track record and is targeting institutional family-office capital that demands ownership.

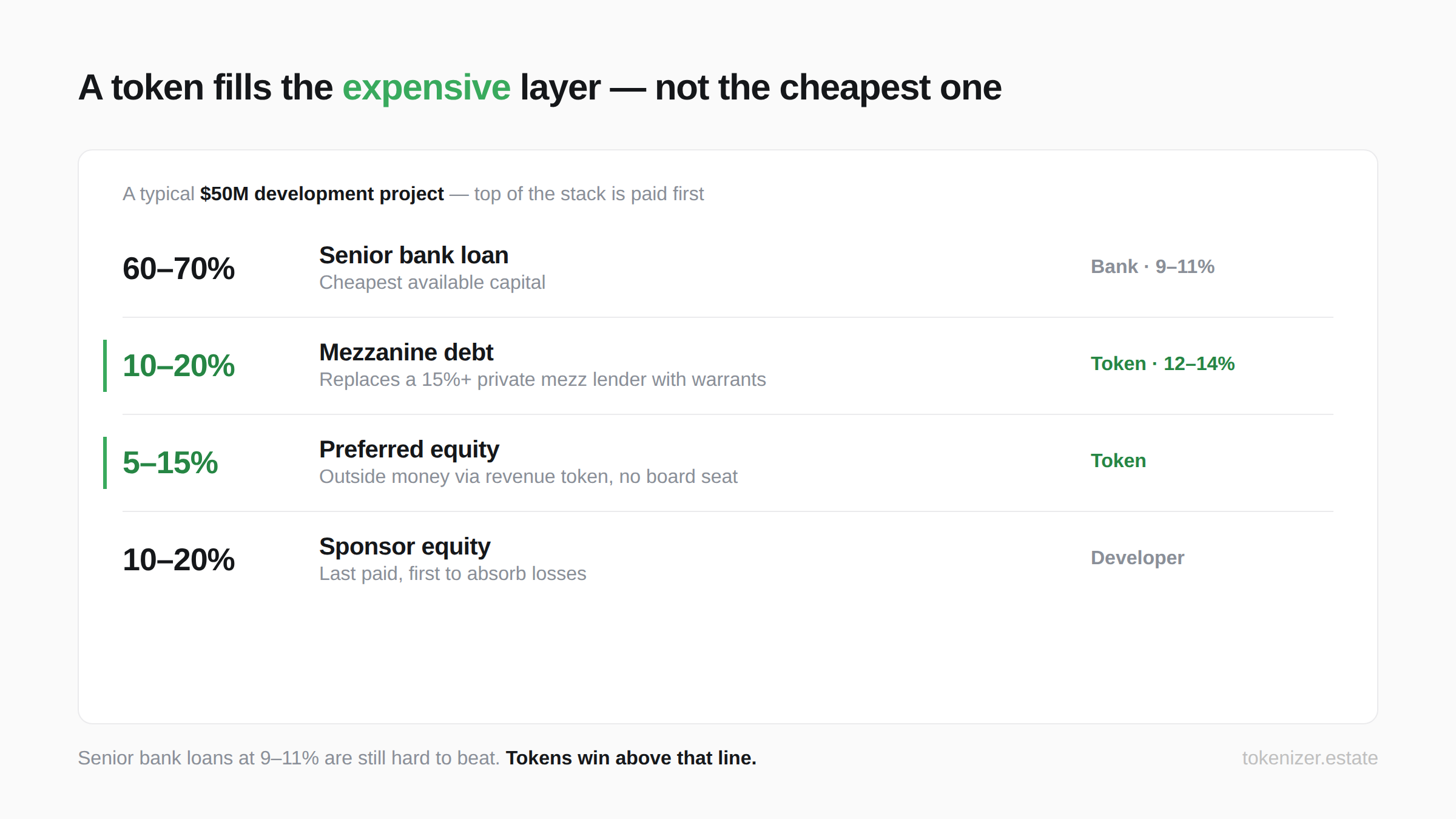

How tokens fit into the capital stack

Tokenization does not replace bank financing. In most working models, it sits next to it.

A typical $50 million development project still gets a senior construction loan from a bank. That loan covers 60% of the cost at the cheapest available rate. What tokenization changes is the layer above that — the mezzanine, the preferred equity, or part of the sponsor's own capital.

This is the part that catches most developers off guard. Tokenization is not always cheaper than a bank loan. A senior bank construction loan at 9–11% is hard to beat with tokens. But a private mezzanine lender at 15% plus warrants is easy to beat with a tokenized debt instrument at 12–14% with no warrants. That is where tokens win.

For sponsor equity — the layer that takes the most risk and waits the longest — tokens give the developer a way to bring in outside money without giving up control of the project. Revenue participation tokens, in particular, let an investor share the upside without sitting on the board.

The smart contract enforces the order of payment on every distribution. Senior debt gets paid first, mezzanine second, revenue tokens or preferred equity third, sponsor equity last. This is exactly how a traditional waterfall works. The difference is that the smart contract does the math automatically every quarter, instead of a fund administrator running spreadsheets.

Two deals that show the model working

The clearest way to understand developer tokenization in 2026 is to look at deals that already exist.

In February 2026, World Liberty Financial announced a tokenization of loan revenue interests tied to the Trump International Hotel & Resort, Maldives. The resort is a flagship project by DarGlobal, scheduled for completion in 2030, with about 100 ultra-luxury beach and overwater villas. The structure is striking: tokens represent a slice of the loan revenue stream from a property that does not exist yet, with investors receiving fixed yield plus participation in proceeds from future villa sales. Distribution runs under US private placement rules — Reg D 506(c) for accredited US investors, Reg S for offshore non-US persons. Securitize handles the issuance. The Trump Organization licenses the brand but does not issue the tokens.

What makes this deal interesting is not the brand. It is the structure. Loan revenue interests on a construction-stage project are exactly the kind of mezzanine financing that used to require a single private lender. Now it is split across many accredited investors, each holding a token that they can trade if a secondary market develops.

A second example sits closer to home for most developers. Kin Capital launched a $100 million tokenized real estate debt fund on the Chintai network, with an initial $5 million tranche. The fund holds first-performing real estate trust deeds, with a $50,000 minimum investment and a target annual return of 14–15% paid quarterly. It is not a single project. It is a fund that lends to multiple development deals, with the tokens representing fund interests rather than direct loans. For investors, this is diversification. For developers, it means there is now a tokenized debt buyer in the market who is not a bank.

Two different shapes of the same idea. One funds a specific construction project directly. The other pools capital and lends across many. Both are real. Both are operating under existing securities frameworks. Neither is a pilot.

What it really costs and what it really delivers

This is where developers need to think carefully, because the marketing around tokenization sometimes oversells the cost story.

The headline benefit you hear is the elimination of intermediaries — no transfer agents, no quarterly distribution checks, no investor relations team cutting paperwork. The smart contract handles all of that. Operational costs at scale do drop materially compared to a traditional fund structure.

That advantage only kicks in at scale, though. For a deal below ten or fifteen million dollars, the setup cost can wipe out the savings. Setup costs for a tokenized offering — legal structuring, smart contract development, audits, KYC infrastructure — typically run into six figures before legal fees in the relevant jurisdiction. Below a certain deal size, a traditional private placement is simply cheaper.

Above $20 million, the math flips. The same compliance and distribution platform handles a $50 million deal almost as cheaply as a $20 million deal. The marginal cost of adding investors approaches zero. This is where tokenization wins.

The other thing tokenization delivers is speed. A traditional mezzanine raise can take several months from term sheet to close. A tokenized offering on an established platform can close materially faster if the legal wrapper and the asset documentation are ready. For a developer trying to lock in a construction window, that compression matters.

What tokenization does not deliver is cheaper capital than a bank can provide. If your bank is willing to lend at 9% senior, do not replace that with tokens at 13%. Use tokens where banks will not go — the mezzanine layer, the construction-stage equity layer, and the cross-border investor base that a domestic bank cannot reach.

There is also a less-obvious benefit. Onboarding mechanics matter more than developers expect. Modern tokenization platforms now support embedded-wallet flows that work through email login, removing the need for investors to manage their own private keys. Without that, a meaningful share of accredited investors abandon the process at the wallet step. With it, the offering actually completes.

Where construction-stage tokenization breaks

The honest part of this article. Construction-stage tokenization is real and it works, but it has failure modes that developers need to understand before they sign anything.

The first failure is cost-of-capital miscalculation. Developers compare the token coupon to retail wealth-management products and conclude that 12% is cheap. It is not cheap by absolute standards. It is cheap compared to the 15% mezzanine lender it replaces. The right comparison is always to the layer the token is replacing.

The second is the senior lender's veto. If you have a bank construction loan in place, that bank may refuse to subordinate to a tokenized mezzanine layer. Many traditional banks are still uncomfortable with tokenized debt sitting above their position. This needs to be confirmed in writing before you start the token offering.

The third is the construction-stage NAV vacuum. There is no operating cash flow to anchor the token's price during construction. If the secondary market opens before the project is complete, prices can swing on sentiment rather than asset performance. Some platforms address this with scheduled milestone valuations and independent verification by quantity surveyors. Others do not.

The fourth is jurisdictional re-registration. A token offering structured for Dubai investors under VARA does not automatically work for European investors under MiFID II. Cross-border distribution sounds frictionless on-chain, but in practice it requires manual jurisdiction-by-jurisdiction configuration of investor eligibility. This is the same pattern we see with emerging markets like Pakistan, where tokenization pilots are now told to seek regulator approval before launch. Plan for it before onboarding starts.

The fifth is the Reg D 506(c) lockup. US accredited investors expect to trade their tokens immediately because the blockchain settlement implies tradability. They cannot. Securities Act Rule 144 imposes a 12-month holding period on restricted securities. This needs to be communicated clearly at the offering, not after the fact.

The sixth and most important: default mechanics on construction-stage tokens are largely untested. Most issued instruments are too young to have hit a hard default, and the legal mechanics for token holders to enforce against a developer's SPV vary widely by jurisdiction. The smart contract can enforce a payment waterfall. It cannot put a lien on a half-built building. That is still a court process in the jurisdiction where the asset sits.

These are not reasons to avoid tokenization. They are reasons to do it carefully, with experienced legal counsel and a platform that has been through this process before.

The bottom line for developers and asset owners

Tokenization is a real financing channel for construction in 2026. It is not a replacement for bank lending and it is not free money. It is a structured way to bring outside capital into the layers of the capital stack where banks will not go and where private mezz lenders charge too much.

For a developer, the question to ask before tokenizing is not whether the technology works. It does. The question is whether the layer of the capital stack you are trying to fill matches what tokens do well. Senior debt from a bank is still cheaper. Sponsor equity from yourself is still safer. Tokens are the right answer for the mezzanine layer, the preferred equity layer, and any deal where you need to bring in dozens of accredited investors instead of one private fund.

For an owner of a yacht, a factory, a marina, or any other asset that needs construction or expansion capital, the same logic applies. The token does not change the asset. It changes who provides the money and on what terms.

Tokenization makes sense when the project is over $20 million, when the asset has a clear legal wrapper, when senior bank debt is already lined up or unavailable on reasonable terms, and when the mezzanine or equity gap is large enough to justify the setup cost. It does not make sense for a small project where a traditional private placement is cheaper, or for any deal where the developer is using tokens to avoid building real underwriting and disclosure.

When a developer, a fund manager, or an asset owner sits down to decide whether to tokenize, the first question is always the same: which layer of the capital stack am I filling, and is a token the cheapest credible source for that layer? The token does not change what gets built. It only changes who pays for it. Answer the question honestly, and the rest of the deal follows a defined path.

This article is for informational purposes only and does not constitute investment, legal, or tax advice. Always conduct your own due diligence and consult qualified professionals before structuring a tokenization project or investing in a tokenized offering.