Debt vs Equity Tokens: How to Choose for Real Estate

Debt and equity tokens look similar on-chain, but they sit in different parts of the capital stack and follow different rules. This guide walks through the choice that defines every tokenization deal before a single line of smart contract is written.

Debt and equity tokens look similar on-chain, but they sit in different parts of the capital stack and follow different rules. This guide walks through the choice that defines every tokenization deal before a single line of smart contract is written.

A $12 million commercial property is on the table. Two investors want in. One wants fixed quarterly income. The other wants long-term appreciation. Both can be served from the same building, but only if the token type is chosen correctly before the legal wrapper is set up.

This is the first real decision in any tokenization project. Most fund managers treat it as a financial product question and resolve it late, after they have already started talking to investors. By that point, switching the structure means rebuilding the SPV, redoing the disclosures, and pushing the launch back by months. We see this pattern often enough that it is worth writing about it directly.

Why this is the first decision, not the last

The token type sets the legal classification of the instrument. That classification then sets the regulatory pathway, the disclosure work, the type of investor who can buy it, and the way exits work later.

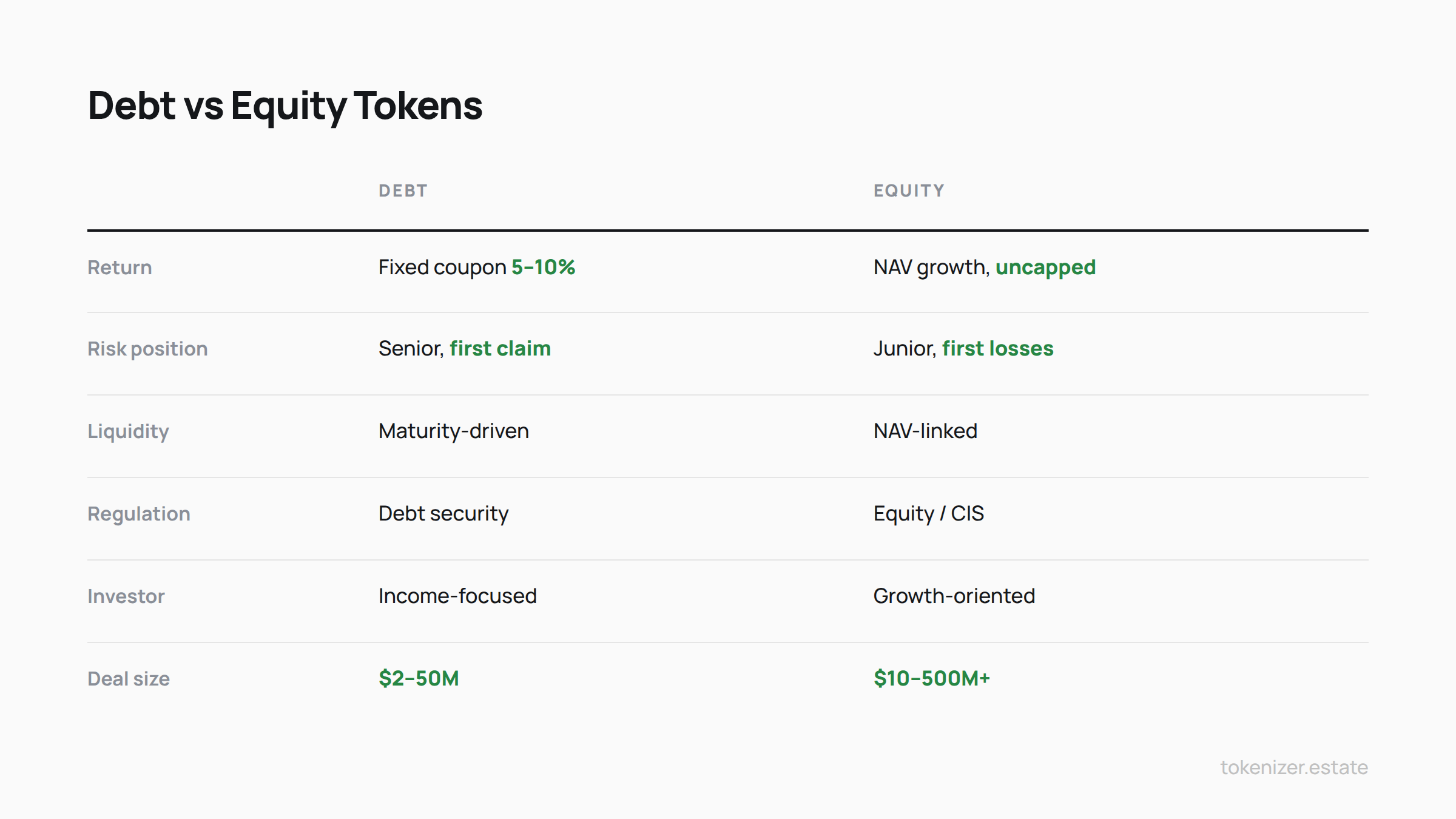

A debt token represents a loan. The holder lends capital to the issuer, receives a coupon, and has a senior claim if the asset is sold or defaults. An equity token represents ownership. The holder participates in the value of the property as it changes, receives a share of net income, and may have voting rights depending on the legal structure.

These are two different positions in the capital stack. A debt holder gets paid first but has a fixed return. An equity holder gets paid last but takes the upside if the property does well.

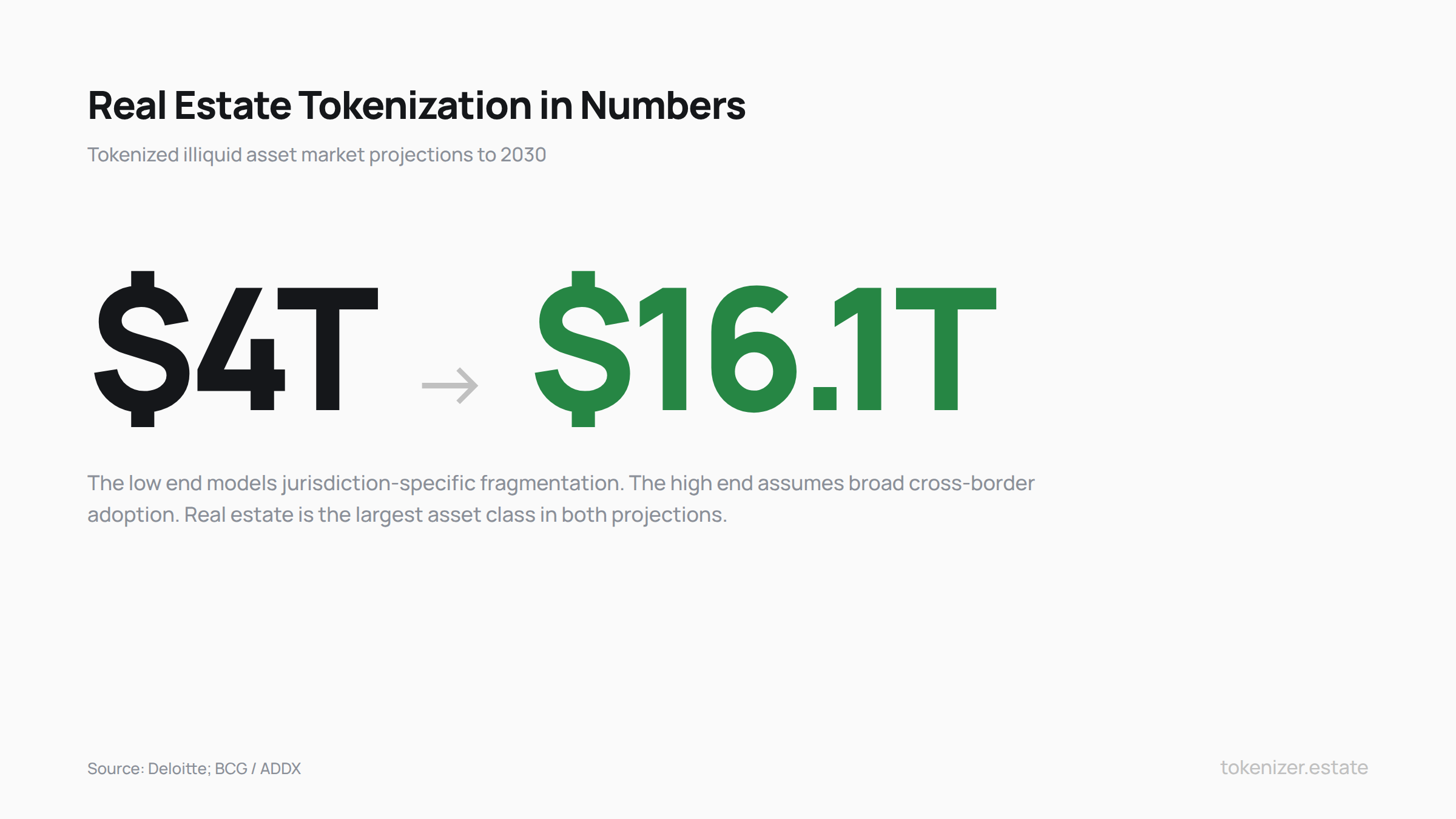

Real estate is now the largest single asset class in tokenization projections through 2030. The Deloitte Center for Financial Services projects tokenized real estate to reach $4 trillion by 2035, growing from under $300 billion in 2024 at a 27% annual rate. The high end of the range comes from a BCG and ADDX report estimating $16.1 trillion across all illiquid asset classes by 2030. The chart below shows both forecasts and what drives the spread between them.

Debt tokens: fixed coupon, senior claim

Debt tokens are the more predictable of the two instruments. The smart contract holds a defined principal, a coupon schedule, a maturity date, and a repayment priority. For compliance teams, this predictability is the main attraction.

An SPV that holds the property issues tokens representing a debt obligation. Token holders receive coupon payments on a schedule, usually quarterly, funded from rental income or asset sale proceeds. At maturity, the principal is returned. If the asset is sold or refinanced earlier, debt token holders are paid before equity holders see anything.

In most jurisdictions, debt tokens are classified as debt securities. They fall under existing bond and note rules, which makes them faster to clear with regulators than equity tokens in markets where the equity classification is still ambiguous. Risk disclosures focus on credit risk and asset coverage, which are familiar territory for any compliance officer.

Three structures are common in real estate. Senior secured notes are backed directly by the property. Mezzanine debt tokens sit below senior debt but still above equity in the capital stack and pay a higher coupon. Bridge loan tokens are short-term instruments used during construction or repositioning, with the highest coupons and the shortest maturities.

Tax treatment is also simpler. Coupon income is usually classified as interest income, which has established withholding rules in most markets. The valuation work behind a debt token is also lighter, because the binding number is the principal and the coupon, not a quarterly NAV. We covered the appraisal cadence problem in detail in our guide on how tokenized property is valued.

The limitation is the upside. If a $12 million office building sells for $18 million three years later, the debt token holder receives the principal and the coupon. Nothing more. Everything above that line goes to the equity layer.

Equity tokens: ownership and full upside

Equity tokens encode ownership. Each token represents a fractional interest in the legal entity that holds the property. The token's value moves with NAV. As the property appreciates, as rental income accumulates, as the portfolio is repositioned, the value of each token adjusts.

This is the instrument for investors who want to be in the asset for its full economic life. The St. Regis Aspen tokenization in 2018 sold 18.9% of a 179-room Colorado resort as digital tokens, and gave token holders ownership benefits including discounted hotel stays alongside the equity position. That kind of dual benefit only works with equity tokens. Debt instruments cannot carry it.

Distributions follow the same logic as dividends in a corporate structure. After operating costs and debt service, net rental income flows to token holders pro-rata. A holder of 0.5% of the token supply receives 0.5% of the distribution. The smart contract handles the calculation directly, without a fund administrator running spreadsheets.

Governance varies by structure. Some equity issuances grant voting rights on major decisions like refinancing, sale, or large capital expenditure. Others are purely economic, with governance kept by the issuer or a trustee. This is one of the most consequential design choices, and it has to be settled in the legal wrapper before the token is issued.

For family offices and fund managers running multi-jurisdiction portfolios, equity tokens allow a level of granularity that traditional fund structures do not. A family office that wants European logistics exposure can hold equity tokens in that sub-portfolio without buying into a residential tranche they do not want. Asset-level transparency at this resolution is becoming a real selling point with sophisticated investors who are tired of fund-level reporting.

The two instruments side by side

The differences are clearest when laid out together.

The two columns describe two different products. A retiree looking for predictable quarterly income is in the debt column. A family office looking for long-term capital appreciation is in the equity column. Most real-world deals have investors of both types showing up at the same time, which is why the smart move is often to issue both from the same property.

Why many fund managers issue both

The common assumption is that an issuer picks one instrument per asset. For diversified portfolios, the better approach is usually to issue both from the same property using a layered SPV structure that separates the two tranches legally and on-chain.

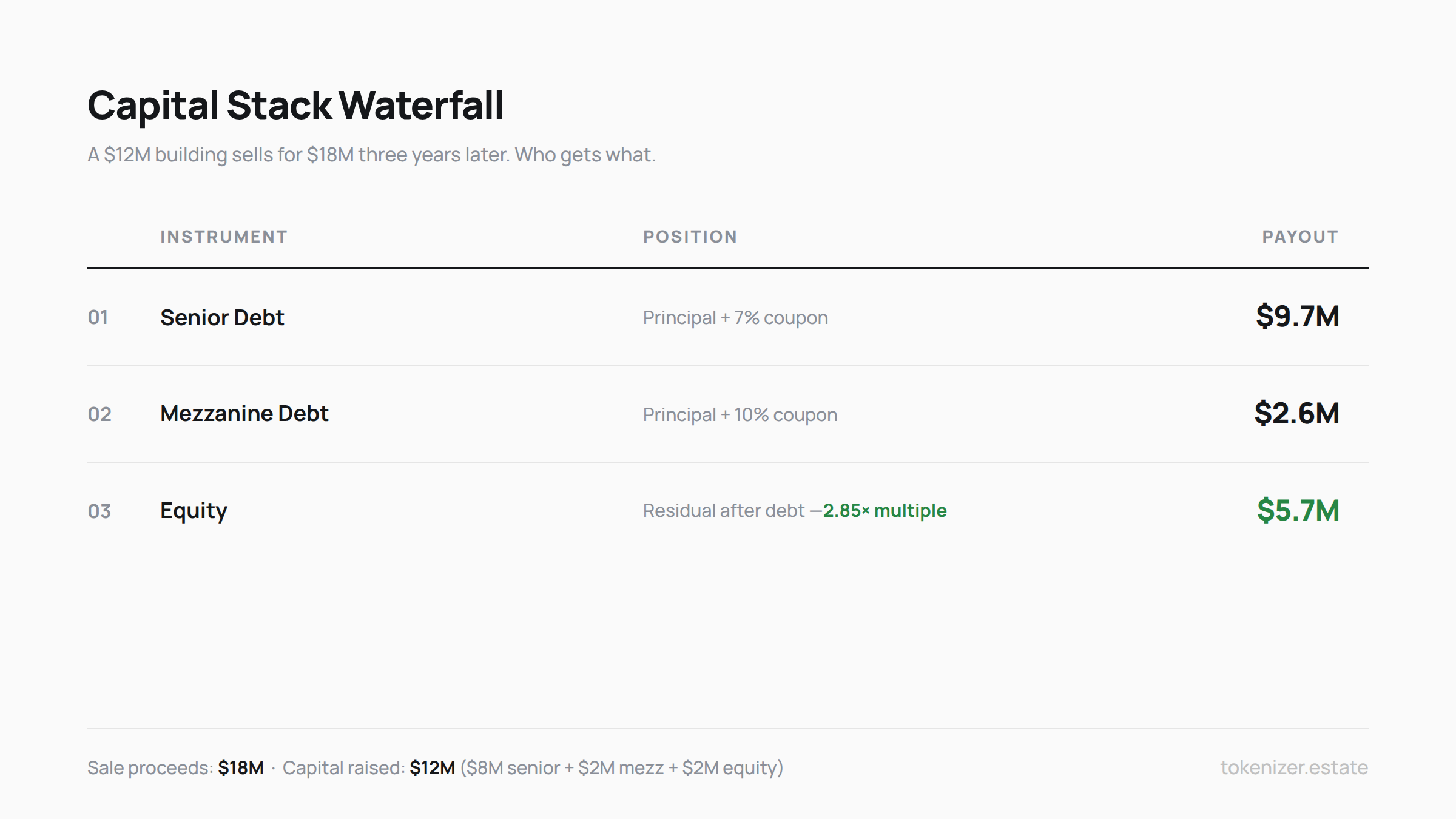

Here is how it works in practice. The asset-holding SPV issues debt tokens to income-seeking investors at a defined coupon and maturity. A second tranche of equity tokens, from the same SPV or a parent entity, captures whatever is left after debt service. The smart contract enforces the order: rental income covers debt coupon first, then equity distributions. At sale or refinancing, debt holders are paid at par, then equity takes everything above.

The example below shows how the math works on a real building.

In this case, equity holders triple their money on a deal where the property gained 50%. That is the leverage effect of sitting at the bottom of the stack with debt above you. It also works in reverse. If the same building had sold for $11 million instead of $18 million, the debt holders would still be made whole, and equity would take the loss.

Two operational requirements decide whether this dual structure is economical. The cap table has to track both instruments separately, with transfer restrictions enforced per tranche. And the smart contract waterfall has to handle edge cases like partial sales, refinancing events, and distressed scenarios without manual intervention. When both layers run on the same compliance and deployment platform, the cost of adding the second tranche is small. When they need parallel legal setups and separate onboarding flows, the structure stops making sense for deals below roughly $20 million.

What changes by jurisdiction

Tokenized debt and equity instruments backed by real estate are securities under most national laws. The specific framework depends on where the SPV sits and where the investors are.

In the European Union, these instruments fall under the Markets in Financial Instruments Directive II (MiFID II) and the Prospectus Regulation, not under MiCA. This is one of the most common points of confusion for issuers entering EU markets. MiCA explicitly excludes crypto-assets that qualify as financial instruments under MiFID II. It governs stablecoins and utility tokens. Security tokens, including the debt and equity instruments used in tokenized real estate, are regulated under the existing financial services framework.

In practice, equity token issuers in the EU may need a full prospectus plus authorization under the Alternative Investment Fund Managers Directive (AIFMD) if the structure looks like a collective investment scheme. Debt token issuers face the same prospectus framework, but the disclosures are usually narrower and the review faster, because credit-risk disclosures follow established bond-market patterns.

In Japan, the Financial Instruments and Exchange Act (FIEA) treats both as securities. Equity tokens that resemble collective investment schemes can trigger J-REIT regulations, which require a licensed investment corporation structure. Debt tokens structured as corporate bonds have a more defined registration path, which is why most early Japanese tokenization projects start with debt.

In Singapore, the Monetary Authority of Singapore allows both debt and equity tokens to be distributed to accredited investors, but each requires jurisdiction-specific configuration of investor eligibility checks before onboarding begins. Pakistan recently told tokenization pilots to seek approval before launch, which signals the same direction in emerging markets across Asia and the Gulf.

The pattern is consistent. Wherever you are, the regulatory rules of the underlying instrument still apply. Tokenization adds a digital layer on top of the same securities framework that has governed debt and equity for decades.

What this means for your platform choice

The technical work behind a debt token is different from the work behind an equity token, and any platform that supports tokenization has to handle both.

Debt tokens require coupon distribution logic. The smart contract has to encode the payment schedule, calculate accrued interest, handle early repayment, and manage default conditions. These are deterministic workflows. The contract pays or it does not, based on rules written into the code.

Equity tokens require more complex logic. NAV calculation has to be triggered on a schedule, usually quarterly, and the result has to flow through to token pricing and distribution amounts. Cap tables have to track fractional ownership across thousands of holders, with transfer restrictions enforced at the contract level for accredited-only offerings. Governance modules, if included, need voting contracts. The most common failure points in equity deployments are not the issuance itself but the ongoing management layer.

KYC and AML onboarding also differs by instrument. Debt offerings to accredited investors need identity verification, accreditation status, and sanctions screening. Equity offerings often need source-of-funds documentation and, in some jurisdictions, suitability assessments. The onboarding flow has to be configured before the first investor is invited, not retrofitted after the first compliance query.

For fund managers running multi-asset portfolios, parallel legal setups and separate onboarding flows for each instrument type erase most of the efficiency that tokenization is supposed to deliver. A single platform that handles both inside one compliance and deployment layer is the only way the math works at portfolio scale. We covered how this fits together at the contract level in our piece on KYC and AML for tokenized securities.

The bottom line

The choice between debt and equity tokens is structural. It defines who can buy, what they get paid, where they sit in the capital stack, and how they exit. It has to be made before the legal wrapper is formed, before the smart contract is configured, and before the first investor is invited.

For most diversified portfolios, the answer is not one or the other. It is both, layered on the same property, separated cleanly in the SPV and on-chain. That structure gives the income investor what they want and the growth investor what they want, from the same asset, without one cannibalizing the other.

For owners and fund managers looking at tokenization, the first question is the same as it always is: what is the asset, who is the investor, and which instrument fits between them. Get that right and the rest of the deal follows a defined path. Get it wrong and you spend the next six months rebuilding what should have been settled in week one.

This article is for informational purposes only and does not constitute investment, legal, or tax advice. Always conduct your own due diligence and consult qualified professionals before structuring a tokenization project or investing in a tokenized offering.