How to Tokenize a Real Estate Portfolio: Operational Checklist for Developers with Existing Assets

A sequential execution guide for developers ready to tokenize an existing property portfolio, walking through every operational step using a 12-asset mixed-use scenario.

A developer walks into the boardroom with a portfolio binder: 12 mixed-use properties across three jurisdictions — eight residential buildings in Lisbon, three commercial assets in Frankfurt, one logistics facility in Rotterdam. Combined book value $84M. The rent rolls are stable, the titles are clean enough, and the question on the table is not whether to tokenize but how to tokenize real estate when the assets already exist on a balance sheet. The conceptual phase is over. What remains is execution sequence.

This is the operational checklist for that moment — the developer who holds the portfolio and needs to know which step locks in before the next can start. Skip the order and the issuance stalls at the regulator gate. Follow it, and the same $84M can hit the market with a premium of up to 20% over private-sale comparables.

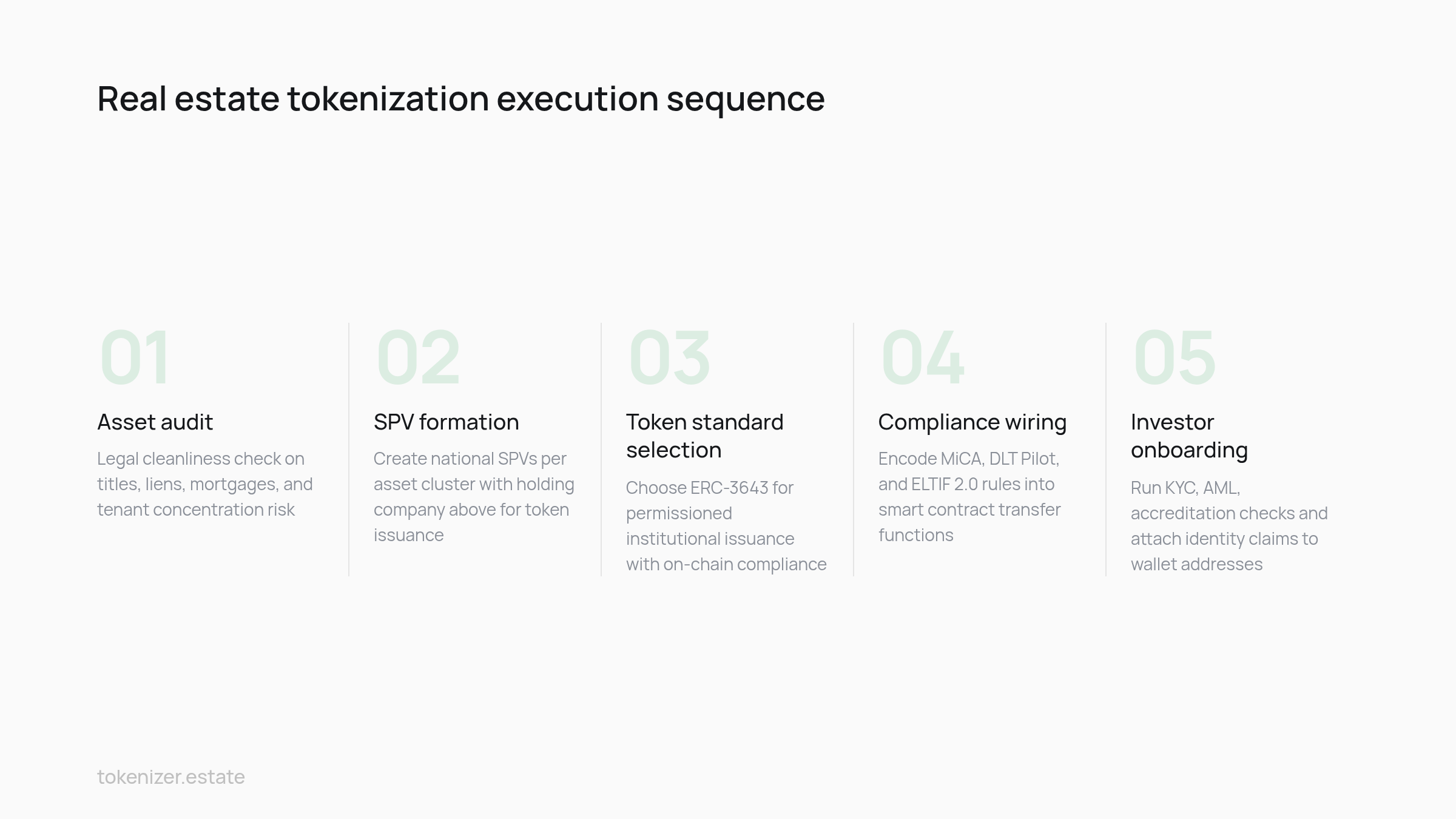

Asset Structuring Audit Before Token Issuance

Before a single smart contract gets drafted, the 12 assets need a structuring audit. Not a valuation refresh — a legal cleanliness check. Are titles registered without contested liens? Are existing mortgages assignable to a new holding entity? Do the rent rolls show tenant concentration risk that will trigger investor disclosure obligations? Each property generates its own answer, and the answers determine which assets enter the first issuance tranche and which get deferred.

In the working portfolio, the eight Lisbon residential buildings have clean Portuguese land registry entries and standard residential leases — first-tranche material. The three Frankfurt commercial assets carry one cross-collateralized loan covering two of the buildings; that loan needs refinancing or partial release before tokenization. The Rotterdam logistics facility has a 15-year single-tenant lease — strong cashflow but a counterparty concentration that demands its own disclosure layer.

The Blocsys checklist frames the execution path across asset selection, legal structuring, token economics, standard selection, custody, oracle design, investor onboarding, launch planning, and long-term platform operations. The order matters because each decision constrains the next. A commentary from Adventures in CRE reinforces the same point from the sponsor side: concept-to-execution failures cluster at the audit stage, not the technology stage.

The output of this phase is a tranching memo — which assets issue first, which wait, and which get carved out entirely. For the $84M portfolio, a realistic first tranche covers the eight Lisbon buildings plus the Rotterdam logistics facility, leaving Frankfurt for phase two after the loan release.

SPV Formation and Jurisdictional Layering

The legal architecture for a three-country portfolio cannot rest on a single entity. The structuring rule is one Special Purpose Vehicle (SPV) per asset cluster, with a holding company above them that issues the token at the consolidated level. An SPV is a legal entity created to hold a specific asset and isolate its liabilities from the parent. For the Lisbon cluster, that means a Portuguese SPV holding the eight buildings; for Rotterdam, a Dutch SPV holding the logistics facility; for Frankfurt (phase two), a German SPV.

Above these national SPVs sits a holding entity in a jurisdiction chosen for token issuance, treaty network, and regulatory clarity. For EU-anchored real estate, Luxembourg and Liechtenstein are the working defaults. Luxembourg offers the securitization vehicle (SV) regime and a deep base of regulated service providers. Liechtenstein offers the Token and Trusted Technology Service Provider Act, which gives explicit legal classification for tokenized rights — a benefit the LegalNodes jurisdictional review repeatedly flags as the cleanest path for EU issuers in 2026.

The standard mechanic is the one Quill Audits describes: in most implementations, an SPV holds the property title and issues security tokens that mirror equity shares. For the 12-asset portfolio, the implementation runs at two layers. The national SPVs hold title. The holding company owns 100% of each SPV. The token issued by the holding company represents a fractional economic interest in the consolidated portfolio, with cashflow distributed up from the SPVs through the holding entity to token holders.

A guide from Antier Solutions details the operational tradeoff: more SPVs mean more administrative cost but cleaner liability isolation; fewer SPVs cut overhead but expose investors to cross-asset risk. For a $84M portfolio with mixed-use exposure across three jurisdictions, the per-cluster SPV structure pays for itself in the first investor due-diligence cycle.

Tax structuring runs in parallel with this work. The holding company location affects withholding tax on distributions, corporate tax on SPV profits, and treaty access for foreign investors. For a portfolio with a mixed investor base — EU institutionals, family offices, qualified retail — the determinant in practice is treaty network depth, not headline corporate tax rate. Developers comparing entity choices can review the trade-offs in this debt vs equity framework alongside the SPV decision.

Token Architecture: Selecting the Standard

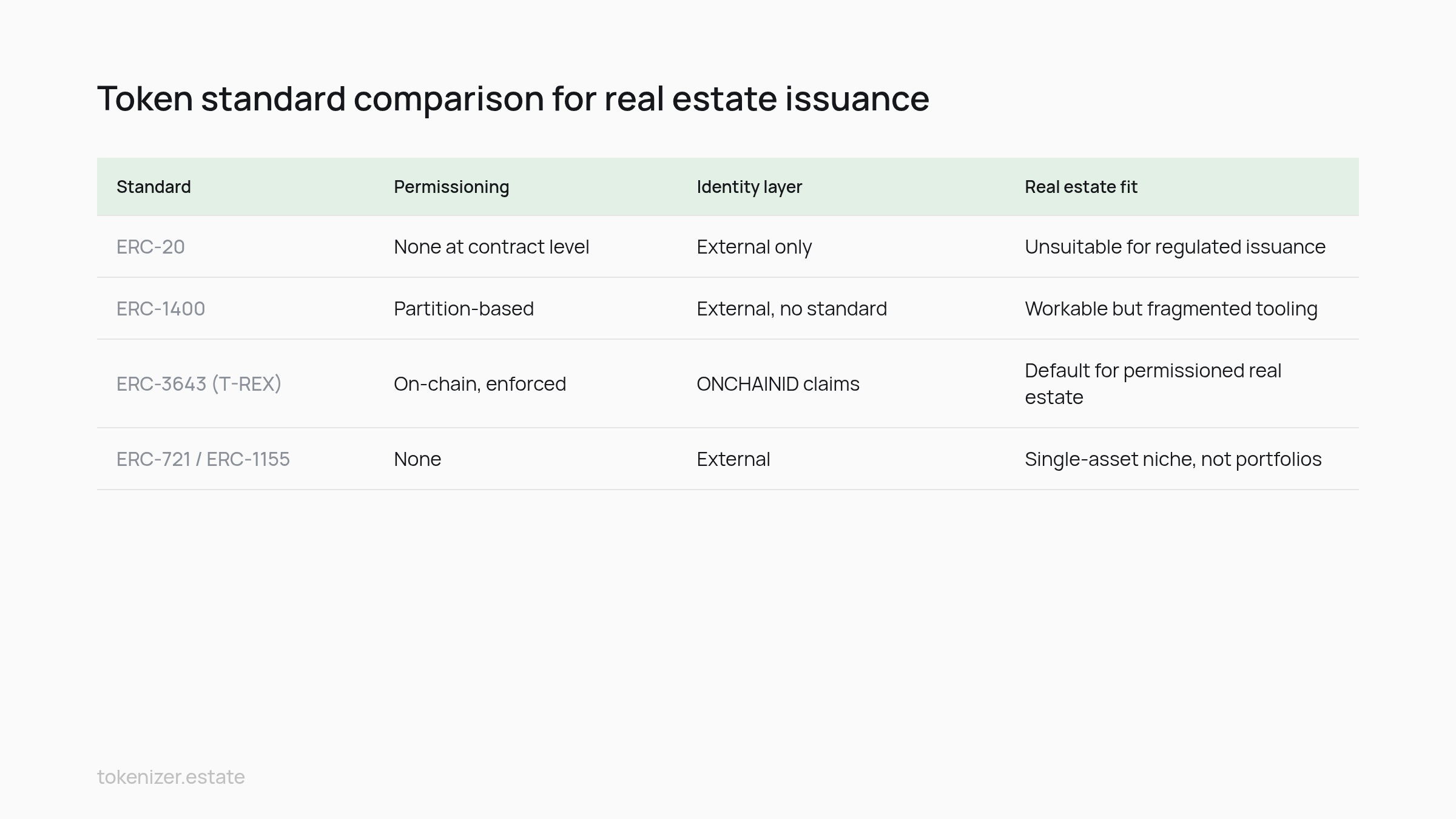

The token standard is not a cosmetic choice. It determines which compliance rules can be enforced on-chain, which wallets can hold the token, and which secondary venues will list it. For institutional real estate, the convergence point is ERC-3643.

Why ERC-3643 Anchors Institutional Issuance

The ERC-3643 protocol is an open-source suite of smart contracts that enables the issuance, management, and transfer of permissioned tokens. Permissioned means the token enforces identity and eligibility rules at the contract level — not at the platform layer that sits above it. A wallet that has not passed the issuer's identity claims cannot receive the token, full stop.

QuickNode's technical breakdown puts it concretely: ERC-3643 is an Ethereum token standard for permissioned tokens, meaning tokens that can only be held and transferred by identities that satisfy predefined compliance rules such as KYC/AML and investor eligibility checks. The standard was originally known as T-REX (Token for Regulated EXchanges) and initiated by Tokeny; it is now formalized as ERC-3643 and governed by the ERC-3643 Association.

Comparison Against Alternatives

Standard | Permissioning | Identity layer | Real estate fit |

|---|---|---|---|

ERC-20 | None at contract level | External only | Unsuitable for regulated issuance |

ERC-1400 | Partition-based | External, no standard | Workable but fragmented tooling |

ERC-3643 (T-REX) | On-chain, enforced | ONCHAINID claims | Default for permissioned real estate |

ERC-721 / ERC-1155 | None | External | Single-asset niche, not portfolios |

For the 12-asset portfolio, ERC-3643 handles three jobs that older standards push to the platform layer. It enforces jurisdictional whitelists (a German retail investor blocked from a Reg D tranche, for example). It enforces holding-period restrictions. And it propagates compliance to secondary transfers — a token sold peer-to-peer still checks the recipient's identity claims before settling. A QuickNode guide walks through the modular compliance contracts that make this possible.

Implementation Reality

The ERC-3643 contract set is not light. It includes the token contract, an identity registry, a claim topics registry, a trusted issuers registry, and a compliance contract with pluggable modules. Deploying this from scratch is a six- to ten-week engineering exercise; deploying it through a configured infrastructure layer compresses to days. Either way, the audit cost and ongoing upgrade governance are real line items in the issuance budget. For deeper mechanics of what runs underneath, see the breakdown of smart contracts behind regulated tokens.

Compliance Configuration for the Real Estate Tokenization Process

Lisbon, Portugal

Once the standard is chosen, the compliance modules need to be wired to the actual regulatory regime the token will live under. For an EU-anchored portfolio in 2026, that means three frameworks in parallel: MiCA, the DLT Pilot Regime, and ELTIF 2.0.

LegalNodes summarizes the architecture this way: the Markets in Crypto-Assets Regulation (MiCA) introduces the first EU-wide regime for crypto-asset issuance and service provision, while the DLT Pilot Regime allows regulated institutions to test trading and settlement of tokenized securities on distributed ledger market infrastructures. For a real estate token classified as a security — which is the operative classification for the 12-asset issuance — MiCA does not apply directly to the instrument; it applies to crypto-asset service providers in the surrounding stack. The token itself sits under MiFID II and prospectus law. The DLT Pilot Regime gives the issuer a path to use DLT-based market infrastructures for trading and settlement without the full legacy CSD requirements.

ELTIF 2.0 enters where the issuer wants to package the tokenized portfolio as a long-term investment fund accessible to retail investors across the EU. The updated European Long-Term Investment Fund (ELTIF 2.0) rules and national reforms are paving the way for tokenized funds, bonds, and other asset-backed instruments — a point the same LegalNodes analysis treats as the practical retail-access route for tokenized real estate.

At smart-contract level, these regimes translate into specific compliance modules: a jurisdictional whitelist (which countries' residents may hold), a qualification module (retail vs professional under MiFID II), a transfer-restriction module (lock-ups during prospectus periods), and a claim-expiry rule (KYC must be refreshed annually or the token freezes). A practitioner overview from Braumiller Law sets out how these rulebook elements get assembled before launch rather than retrofitted after.

The structural implication is that compliance is not a wrapper around the token. It is encoded inside the token's transfer function. Every secondary trade re-runs the checks. That is the binding requirement institutional buyers test for in due diligence.

Investor Onboarding and Custody Setup

Compliance modules need data to act on. That data comes from the onboarding flow. For the 12-asset issuance, the onboarding stack runs four checks per investor: identity verification (passport or ID document with liveness check), AML screening (sanctions, PEP, adverse media), accredited or qualified investor status per the investor's home jurisdiction, and tax residency declaration for distribution withholding.

The output of onboarding is a set of identity claims attached to the investor's wallet address through the ONCHAINID registry. Once those claims are in place, the token contract will accept transfers to that wallet — and refuse transfers to any wallet without them. A retail investor in Portugal qualified under an ELTIF 2.0 tranche gets a different claim set than a professional investor in Germany participating in the Reg S sleeve. The contract reads both.

Fractional entry points as low as $25 open the market to retail investors, according to Quill Audits — a figure that matters less as a literal minimum than as a signal of how granular the cap-table mechanics can run. In the working portfolio, the issuer is unlikely to set the minimum that low; a more realistic minimum sits in the €500–€5,000 range depending on the jurisdiction's investor protection rules. But the technology does not constrain the choice.

Custody splits into two models. Self-custody pushes the wallet to the investor — the issuer never holds keys, the investor signs every transaction. Qualified custodian model pushes keys to a regulated custodian who holds tokens on behalf of investors, often the only acceptable structure for institutional buyers under their internal mandates. Most portfolios offer both, segmenting by investor type. A platform walkthrough from Innowise shows the dual-track onboarding logic in practice.

Distribution Channels and Real Estate Token Issuance Steps at Launch

The market the portfolio enters in 2026 is materially larger than the one developers studied in 2023. By early 2026, tokenized real-world assets had already reached meaningful scale, per the Blocsys checklist. Estimates from Quill Audits' technical analysis put total value locked across RWA protocols at over $18 billion, with projections of $4 trillion in tokenized real estate by 2035 — a long-dated projection that carries the usual methodology caveats around adoption curve assumptions. The ERC-3643 Association frames the addressable opportunity at the asset-class level: securities represent a global market of 100+ trillions of dollars, of which tokenized real estate is one segment.

For the 12-asset portfolio, distribution runs on two tracks. Primary placement uses a private placement memorandum (PPM) distributed through regulated platforms — broker-dealers in jurisdictions where required, MiFID II investment firms in the EU. The PPM names the SPVs, discloses the asset-level financials, and sets the subscription terms. Subscription orders flow to the issuer; allocated tokens mint directly to investor wallets after onboarding completes.

Secondary liquidity is the harder problem. A token can technically transfer on day one of issuance, but a venue with order flow is what makes the transfer meaningful. The DLT Pilot Regime venues are the regulated answer in the EU. Alternative trading systems in the US are the equivalent for Reg D and Reg S tranches. A Chainalysis analysis notes that ERC-3643 tokens carry their compliance rules into any venue, which is what makes multi-venue listing structurally possible for an issuer.

The launch sequence the issuer commits to publicly is the one investors price against. A clean sequence — audit, SPV, contracts, compliance, onboarding, primary, secondary — signals the operational discipline that supports the 20% pricing premium real estate tokens have shown over private-sale comparables. Issuers planning the secondary phase in detail can review the mechanics in this overview of secondary market trading for property tokens. A case-study compilation from RWA Paris documents the launch patterns that have closed in the past 18 months.

The real constraint here is not technology readiness. It is the sequence — primary distribution that closes the subscription book before secondary liquidity goes live, and a venue strategy decided before the PPM is printed, not after.

Tokenizing an existing portfolio runs as a sequenced operational program: asset audit, SPV layering, standard selection, compliance wiring, onboarding setup, and distribution activation, locked in that order. Reverse any two steps and the issuance hits the regulator gate without the documentation to clear it. Follow the order and a $84M portfolio that today sits on a balance sheet can convert into a permissioned token issuance — with the same assets, the same cashflows, and a distribution channel that institutional and qualified retail capital can actually buy through.

Developers ready to map this sequence against their own portfolio can review the jurisdiction and standard configuration paths at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo