How to Tokenize Real Estate: The Compliance Configuration Decisions That Determine Investor Access

Before a single token is minted, issuers must resolve a sequence of compliance decisions that shape who can invest, where, and under what rules. This guide walks through that decision chain.

In 2025, Dubai's first tokenized property sold in under 24 hours to 224 investors from 40 countries. To tokenize real estate at that speed and scale, the issuer had already resolved dozens of compliance configuration decisions — eligibility gates, transfer rules, jurisdiction filings, KYC tiers — before a single token contract touched the blockchain. The technology carried the transaction; the configuration made the transaction legal.

The binding limit on any tokenized offering is the smaller of two numbers: how many investors the legal wrapper permits, and how many the technical whitelist can admit. Everything below sequences that decision into an operational plan.

Why Compliance Configuration Precedes Token Design

Real estate tokenization has an eight-year track record and a short list of instructive precedents. The first noteworthy deployment happened in 2017, when a Manhattan property was fractionalized into digital tokens, according to Legal Nodes. A year later, the St. Regis Aspen Resort in Colorado sold nearly 19% of its equity as a tokenized security and raised $18 million on Ethereum. Both deals cleared because the compliance perimeter — accredited-investor gating, disclosure filings, transfer restrictions — was defined before the tokens were minted.

The Dubai 2025 sale, documented by Kayrouz & Associates, closed in under 24 hours with 224 investors from 40 countries because eligibility, jurisdiction, and transfer parameters were locked in advance. Deals that stall in regulatory review almost never stall on smart contract bugs. They stall because the issuer treated compliance as a wrapper layer after token design, when the correct sequence runs the other way: the compliance decisions determine what the token can be.

Across all four venues this guide covers — the EU, the US, the UAE, and Singapore — a real estate token is treated as a security token, not a utility or payment token. That single classification decides which regulator applies, which investor categories are eligible, and which transfer restrictions must be encoded on-chain from day one.

Jurisdiction Selection Logic for Real Estate Tokenization

Jurisdiction is the first configuration decision because every downstream parameter — investor eligibility, disclosure format, transfer restrictions, filing calendar — inherits from it. Four venues cover the majority of institutional real estate tokenization activity: the EU under MiCA, the US under Regulation D and Regulation S, the UAE under the VARA/DLD/ADGM matrix, and Singapore under the Monetary Authority of Singapore's securities regime.

MiCA, formally Regulation (EU) 2023/1114, was adopted in May 2023 and entered into force on June 29, 2023, per Cryptoverse Lawyers. Security tokens for real estate largely sit outside MiCA and are governed by the Prospectus Regulation and MiFID II, but service providers may still fall inside MiCA's Crypto-Asset Service Provider (CASP) perimeter.

The UAE runs a multi-regulator model. Various authorities — VARA, DLD, SCA, DIFC, and ADGM — oversee aspects of virtual assets, securities, and property law, making the regime complex but internally consistent once the issuer picks a lane. Dubai's DLD projects that tokenized real estate could reach AED 60 billion (about USD 16 billion) by 2033, roughly 7% of the emirate's total real estate transactions — a scale that anchors the UAE as a primary venue rather than an experimental one.

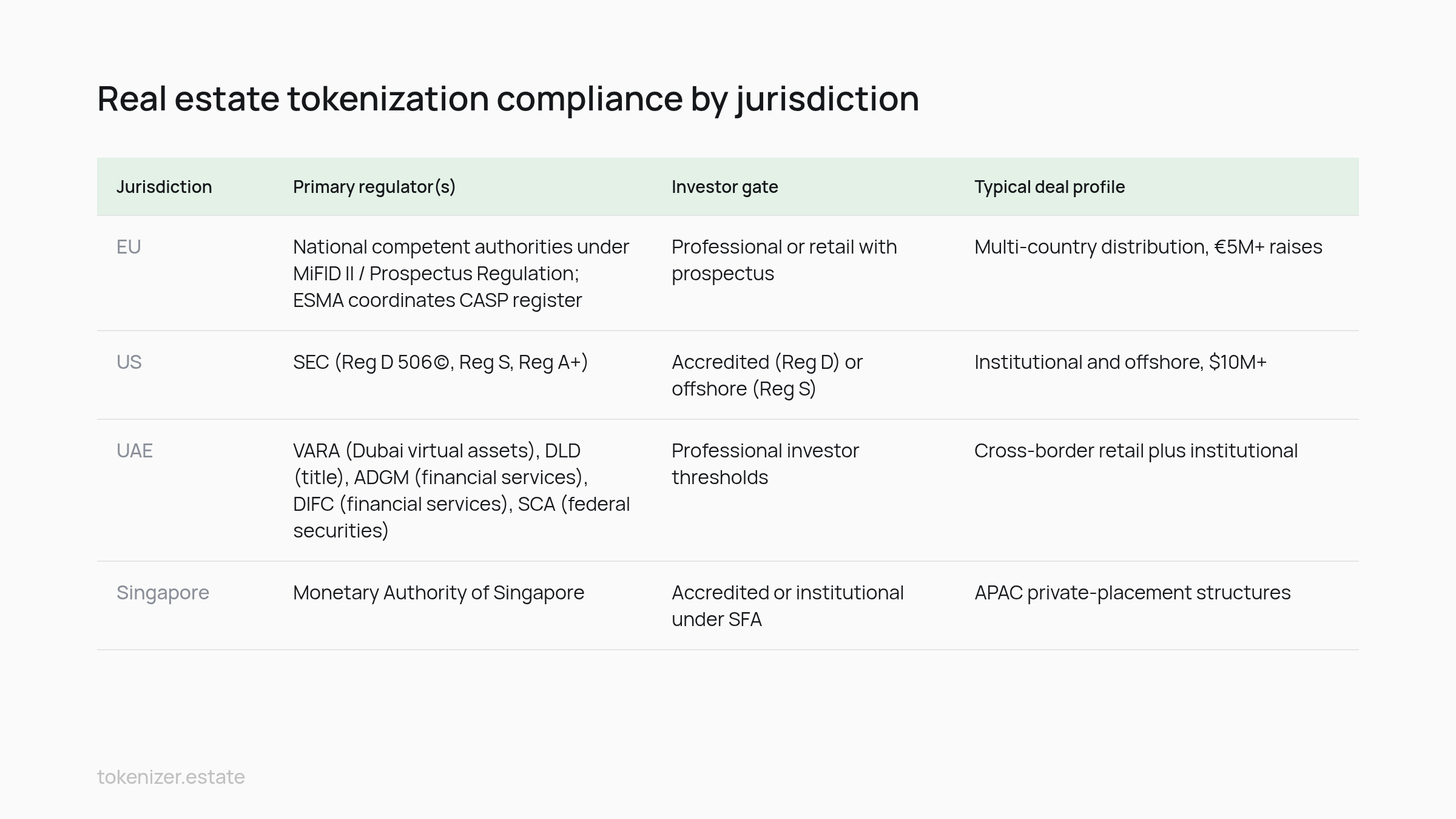

Comparative jurisdiction table

Jurisdiction | Primary regulator(s) | Investor gate | Typical deal profile |

|---|---|---|---|

EU | National competent authorities under MiFID II / Prospectus Regulation; ESMA coordinates CASP register | Professional or retail with prospectus | Multi-country distribution, €5M+ raises |

US | SEC (Reg D 506(c), Reg S, Reg A+) | Accredited (Reg D) or offshore (Reg S) | Institutional and offshore, $10M+ |

UAE | VARA (Dubai virtual assets), DLD (title), ADGM (financial services), DIFC (financial services), SCA (federal securities) | Professional investor thresholds | Cross-border retail plus institutional |

Singapore | Monetary Authority of Singapore | Accredited or institutional under SFA | APAC private-placement structures |

Deal-size logic

For deals under $20M with a US-heavy investor base, Reg D 506(c) paired with Reg S remains the most efficient dual-track structure — a point developed in the comparative analysis by SoluLab. For pan-European retail distribution, an EU prospectus-approved offering pays for itself above €8–10M. Cross-border retail deals with GCC and Asian investors sit most cleanly under a Dubai VARA or ADGM structure, as the comparative Dubai–Singapore analysis by Advomi makes clear.

Issuers with a specific UAE mandate should review the ADGM vs VARA comparison, which resolves the sub-jurisdiction choice inside the Emirates.

EU MiCA Filings and the Real Estate Tokenization Perimeter

MiCA's scope is narrower for real estate issuers than most first-time readers assume. The regulation covers crypto-assets that are not already financial instruments; tokenized real estate structured as a security token falls under MiFID II and the Prospectus Regulation instead. What MiCA does regulate — for real estate issuers — is the service providers they use.

MiCA started enforcing stablecoin rules in June 2024, and rules for Crypto-Asset Service Providers (CASPs) became fully active on December 30, 2024, according to Cryptoverse Lawyers. As of November 2025, more than 53 companies have received CASP licenses. Any exchange, custodian, or transfer agent an issuer plans to use for a tokenized property deal distributed in the EU must either hold a CASP license or fall inside a security-token exemption. The interim MiCA register is published by ESMA as a set of csv files until mid-2026, when it will be formally integrated into ESMA's central register.

The practical implication is that a real estate security token issuer runs two parallel compliance tracks: the securities track (prospectus, professional-investor documentation, MiFID II conduct rules) and the service-provider track (checking that each counterparty is CASP-licensed or exempt). The analysis by Tokeny confirms that tokenized securities themselves are unaffected by MiCA's substantive rules — but the service-provider perimeter still binds them.

Industry aggregators, including Cryptoverse Lawyers, cite projections of a €2 trillion regulated token market by 2028; the figure reflects secondary compilation rather than primary tracking, and should be read as a directional signal on institutional appetite rather than a measured forecast. For issuers, the operational takeaway is that MiCA-adjacent infrastructure is filling out fast enough to make EU-passported tokenized real estate a viable primary market, not a boutique one: the CASP register grew past 53 licensed providers within roughly eleven months of the regime taking full effect at the end of 2024, so the exchanges, custodians, and transfer agents an EU deal depends on now exist in number rather than in pilot. Issuers building an EU structure should also review the MiCA-regulated markets playbook for prospectus-vs-exemption sequencing.

Investor Accreditation Tokenization Rules by Jurisdiction

Accreditation is where compliance policy becomes token code. Each jurisdiction defines investor categories differently, and the token contract's whitelist must mirror the category the issuer has chosen — no exceptions, no discretionary overrides. The categories are not interchangeable across borders.

United States: accredited vs. non-accredited

Under Regulation D 506(c), only accredited investors — individuals with $1M+ net worth excluding primary residence, or $200K+ annual income ($300K joint) — may participate, with verification required. Regulation S permits offshore investors under a US-issuer offering but bars US persons for a distribution period. Reg A+ opens the door to non-accredited retail up to $75M per year, at the cost of a Form 1-A qualification with the SEC, according to the framework laid out by Honeybricks. Reg D combined with Reg S remains the standard structure for pairing accredited US buyers with offshore subscribers under a single token, as documented in the IR Global 2024 analysis of tokenized real estate as a gateway for international investors into US markets.

EU: professional vs. retail under MiFID II

MiFID II splits investors into professional and retail categories, with an elective professional path for high-net-worth retail investors who meet at least two of three tests: a financial-instrument portfolio above €500,000, at least a year of relevant financial-sector work experience, or a record of ten significant transactions per quarter over the prior four quarters. A professional-only offering can proceed under a private-placement carve-out with reduced disclosure — typically a term sheet and risk statement rather than an approved prospectus. A retail-inclusive offering triggers full prospectus approval by a national competent authority.

UAE and Singapore

The UAE uses a professional investor definition (AED 4M net assets, or AED 1M with financial-industry experience) at the federal SCA level, with variations at ADGM and DIFC. Singapore's accredited investor test under the Securities and Futures Act requires SGD 2M net personal assets or SGD 300K income. Structuring under Reg D, Reg S, and MiFID II compliant frameworks is standard practice among specialized STO advisors, as InnReg documents in its regulatory guide.

The token contract enforces these categories through an on-chain identity registry: an investor's verified category is written to their identity claim, and the transfer function checks the claim before allowing any movement. A wallet without the correct claim cannot receive the token — not through the primary sale, not through a secondary trade.

Configuring KYC AML Tokenized Securities Workflows

The configuration question precedes vendor selection: what checks must pass at what investment threshold, and what evidence must be retained for how long. Once those parameters are set, the vendor stack becomes a procurement exercise.

RWA.xyz reports more than one million holders of real-world asset tokens as of July 2026, up sharply over the prior year. That figure is not a clean headcount of investors — one investor may hold multiple wallets, and institutional custody wallets aggregate many beneficial owners — but it does indicate the scale at which KYC infrastructure must operate. A tokenized real estate deal targeting even a fraction of that base needs a tiered onboarding model.

A workable tier structure has three bands. Tier 1 covers subscriptions below a jurisdictional threshold (commonly USD/EUR 15,000 in the EU): identity document, liveness check, sanctions screening, PEP screening. Tier 2 covers subscriptions between the threshold and roughly USD/EUR 100,000: adds proof of address, source-of-funds declaration, and enhanced sanctions review. Tier 3 covers larger investments and any subscription flagged by risk scoring: adds documentary source-of-funds evidence, beneficial-ownership tracing for corporate subscribers, and manual compliance officer sign-off.

The iDenfy compliance guide covers the identity-verification mechanics; property-industry-specific KYC tool comparisons appear in the 2026 review by Agora. Ongoing monitoring is the piece most issuers underweight: sanctions lists update daily, and a token that was compliant at subscription can carry a sanctioned holder six months later if periodic rescreening is not automated. The compliance officer's mandate must include a defined rescreening cadence — quarterly at minimum, monthly for higher-risk jurisdictions — with an on-chain freeze function available if a match is confirmed.

Programming Transfer Restrictions with ERC-3643

Transfer restrictions are where compliance policy becomes executable code. A whitelist maintained in a spreadsheet is not a compliance system; a whitelist enforced by the token contract at every transfer is. The ERC-3643 standard is built for this enforcement model.

ERC-3643 is an Ethereum token standard for permissioned tokens — tokens that can only be held and transferred by identities that satisfy predefined compliance rules such as KYC/AML, investor eligibility, and jurisdiction, per the QuickNode guide. Originally known as T-REX (Token for Regulated EXchanges) and initiated by Tokeny, it is now formalized as ERC-3643 and governed by the ERC-3643 Association. The Chainalysis primer describes the identity-registry architecture in detail.

Illustrative configuration: a Frankfurt office building tokenized under a Reg D 506(c) plus Reg S dual track. The compliance rulebook programmed into the token contract enforces four rules on every transfer. First, the sender and receiver must both hold valid identity claims from an approved claim issuer. Second, receivers with a US claim must carry an accredited-investor verification not older than 12 months. Third, transfers to any wallet flagged with a sanctioned jurisdiction claim revert. Fourth, transfers within the Reg S distribution compliance period (typically 40 days or one year, depending on issuer category) are blocked between US and offshore wallets.

Specialized development shops build ERC-3643-based infrastructure that verifies investor eligibility, accreditation, and transfer restrictions inside the token itself, as described by OmiSoft. The consequence for the issuer is that the compliance rulebook must be finalized before the contract deployment transaction is signed. Rules can be updated post-deployment through the compliance module — but only if the update mechanism was written in from the start. Retrofitting a whitelist onto a plain ERC-20 token is not an option; the contract has no transfer-hook to enforce the check. For a deeper walkthrough of what happens after this configuration is deployed, the post-issuance operations guide covers register maintenance, distributions, and secondary trading.

Tokenizing real estate is a sequenced compliance configuration exercise before it is a technology exercise. Jurisdiction, investor eligibility, KYC tiering, transfer logic, and filings must be locked before the token contract is deployed — retrofitting any of these after launch either fails outright or requires a fresh issuance. The single most common — and most expensive — sequencing error is choosing a token standard or blockchain first, then discovering the chosen investor category demands transfer rules the deployed contract cannot enforce. The fix is not technical; it is a fresh issuance. The order that works does not change: jurisdiction first, then investor category, then the KYC tiers and transfer rulebook those two dictate, and only then the token standard that can encode all of it. An issuer who can answer "which investors, in which jurisdictions, under which transfer restrictions" before writing a line of contract code has already removed the failure mode that stalls most deals.

Issuers preparing an offering can access the ERC-3643 rulebook template and jurisdiction configuration checklist at Tokenizer.Estate — both are available without a sales call.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo