Post-Issuance Operations: What Actually Happens After You Tokenize a Building

Issuance is the easy part. The real work begins when the token goes live and operations must keep pace with investors, regulators, and reality.

A $40M multifamily property tokenizes on a Tuesday. By Friday, the operations team realizes nobody configured the quarterly rental distribution waterfall, two investors failed a re-KYC check, and the on-chain holder list no longer matches the SPV's official share register. This is where tokenized real estate operations actually begin, not at the token sale, but the morning after.

The issuance gets the press release. The post-issuance phase decides whether the deal still works in month twelve.

Why Post-Issuance Breaks Tokenized Real Estate Deals

Issuance is a discrete event with a clear endpoint. Post-issuance is an open-ended operational regime with no off-switch. Most teams staff for the first and improvise the second, which is why year-one failures cluster around missed distributions, governance disputes, and cap-table drift rather than around the token sale itself.

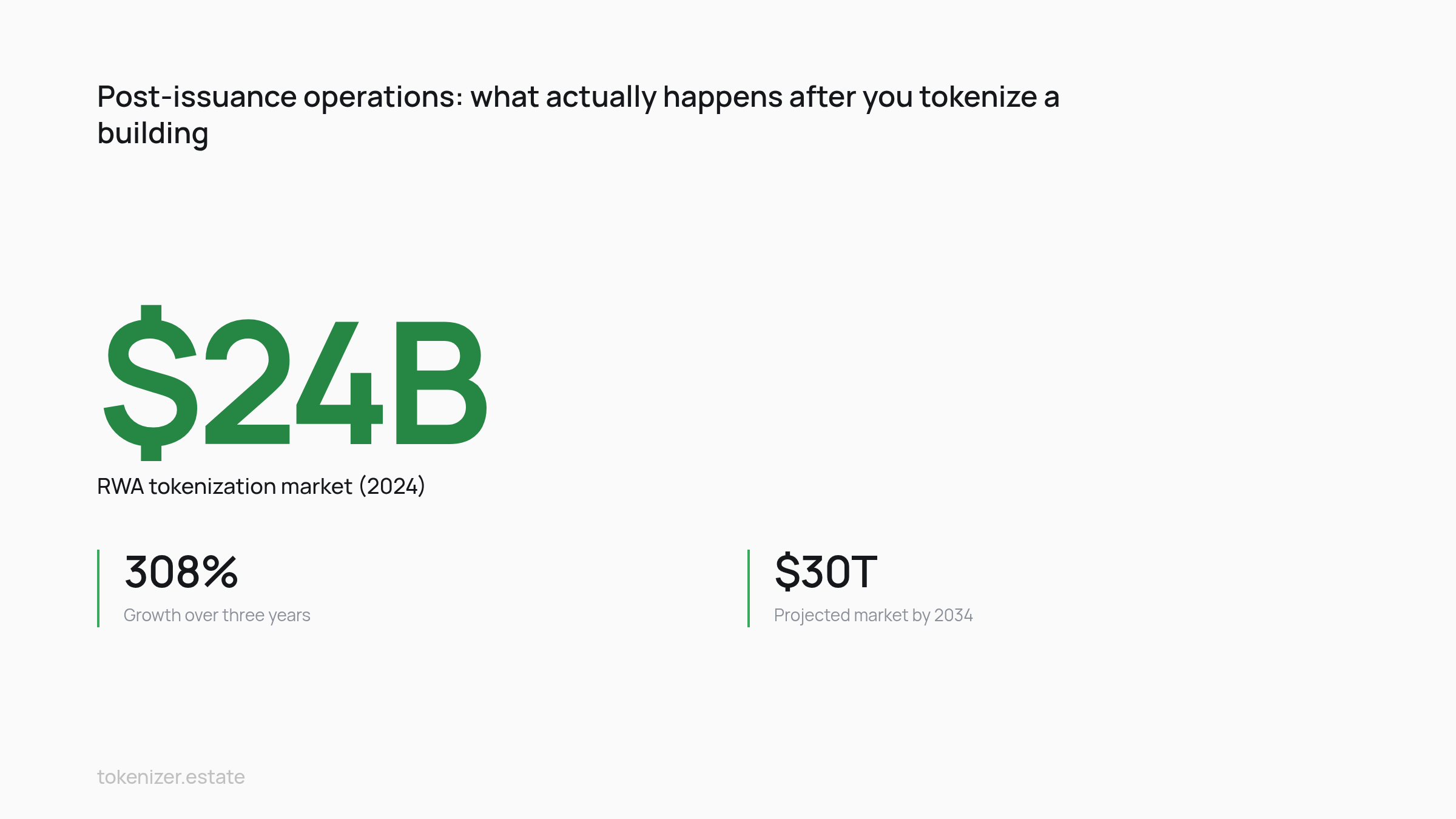

The stakes have grown with the market. The tokenized RWA market has more than tripled since early 2025, reaching $31.9 billion by June 2026, per RWA.xyz data cited in InvestaX's liquidity review. Katten's Tokenization of Real-World Assets review cites Standard Chartered's projection of up to $30 trillion by 2034. Even discounted for projection optimism, the implication is direct: more issuers, more holders per deal, more jurisdictions per holder, and more operational surface area where things can go wrong silently for weeks before anyone notices.

Repeat capital follows operational track record. The Adventures in CRE practitioner review of execution-stage tokenization notes that governance and execution are where sophisticated LPs evaluate tokenized vehicles most closely. In practice, re-up decisions track distribution reliability and reporting cadence far more closely than headline IRR: a missed quarterly distribution in month four costs less in dollars than in the lost ability to raise the next vehicle from the same investor base.

Rental Distributions and NAV Updates in Tokenized Real Estate Operations

Distributions and NAV are the two recurring obligations every tokenized property owes its holders. Both look like accounting questions and turn out to be reconciliation problems between three ledgers: the property management system, the SPV's books, and the on-chain holder snapshot.

The distribution cadence and waterfall logic

A monthly or quarterly distribution starts with net operating cash at the property, runs through the SPV's waterfall (debt service, reserves, preferred returns, promote) and arrives at a per-token amount payable to whoever held the token at the snapshot block. The operating agreement defines the waterfall in legal prose. The smart contract enforces only what the issuer programmed. Gaps between the two surface the first time a holder disputes a payment.

Stablecoin rails compress the settlement cycle from days to minutes, but they do not remove the upstream work: rent collection, expense reconciliation, reserve top-ups, and tax withholding still happen in conventional systems. The NAV Fund Services operational guidance on tokenized fund administration describes the pattern most issuers settle into: fiat in at the property level, stablecoin out at the holder level, with the SPV bank account as the bridge and the fund administrator as the controller of the cutoff.

NAV cadence and the appraisal lag

Real estate NAV moves slowly. Appraisals run annually for most private vehicles, quarterly for institutional ones, and almost never monthly. Tokenized vehicles inherit that cadence whether the market wants them to or not. The lag is the operative constraint on secondary pricing: when the last published NAV is six months old, the bid-ask on any secondary venue prices in stale-data risk on top of liquidity risk. The appraisal cadence analysis on this site walks through how listed REIT pricing, broker opinions of value, and rolling capex adjustments are used to keep an interim NAV defensible between formal appraisals.

Deloitte's Digital Dividends outlook on tokenized real estate projects that tokenized property on blockchain networks could exceed US$4 trillion by 2035, up from under US$300 billion in 2024. A methodology caveat applies, since the figure includes mortgage-backed instruments and tokenized fund wrappers alongside direct property tokens. The operational implication of that growth is administrative: NAV calculation, distribution reconciliation, and holder reporting are the three workflows that need to scale before the dollar volume does.

Reconciliation as the daily job

The fund administrator's actual day-to-day work on a tokenized vehicle is reconciliation. Property-level cash needs to match SPV bank balances. SPV register needs to match on-chain holders. Distribution amounts paid need to match the waterfall calculation. When any pair drifts, the next distribution will be wrong, and the wrong distribution is harder to claw back from a self-custody wallet than from a brokerage account.

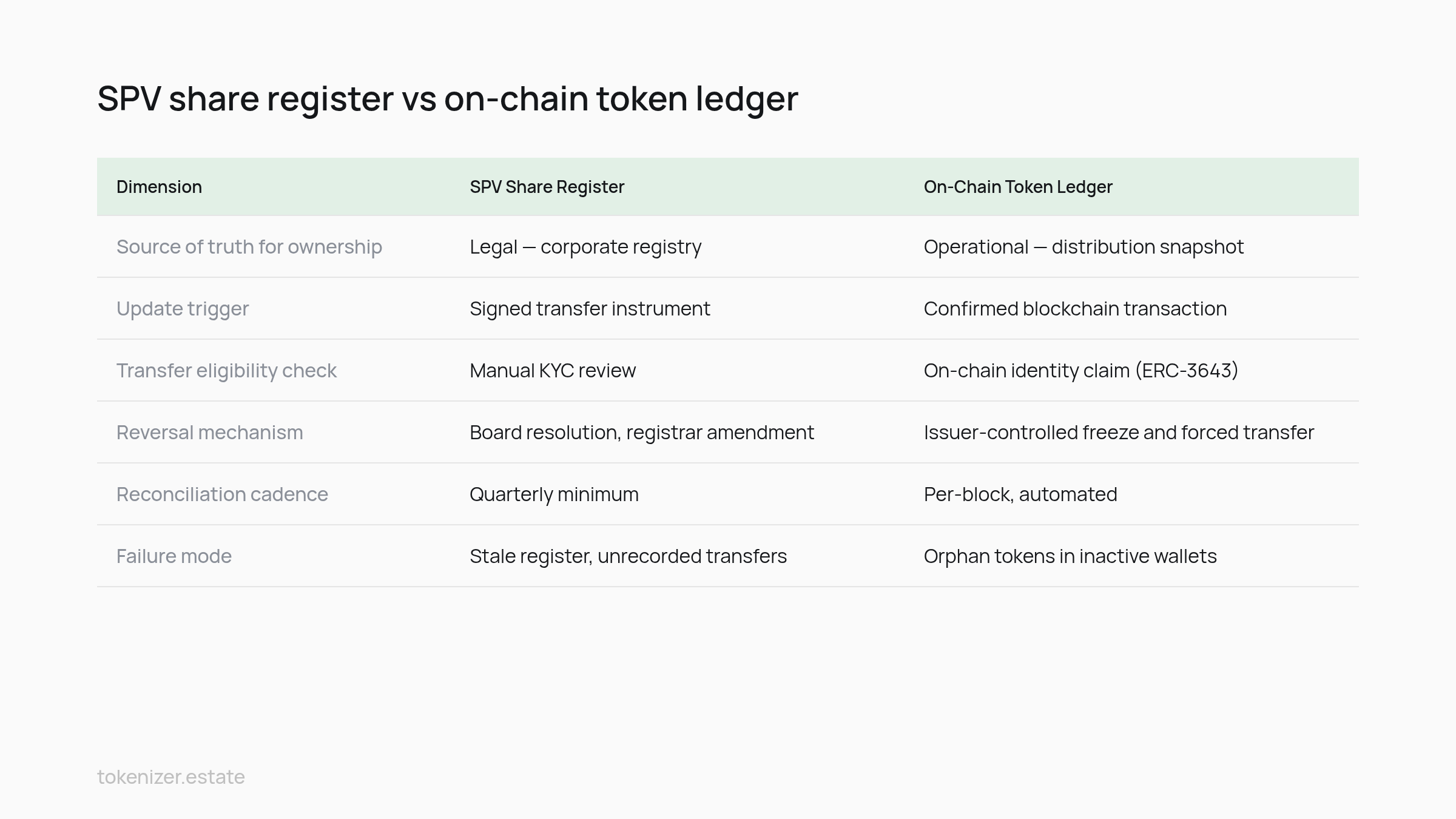

Cap Table Sync Between SPV Register and Token Ledger

Every tokenized real estate deal runs two cap tables. The legal one sits with the company secretary or transfer agent and defines who actually owns the SPV's shares. The on-chain one sits in the token contract and defines who can receive the next distribution. These two ledgers must agree after every transfer, redemption, forced reversal, and corporate action, and they often do not, because they update on different triggers.

The dual-ledger problem in practice

CAIA's mini-course on crypto tokenization of real assets describes the standard fungibility model: each ERC-20-style token represents one share out of a fixed total: for example, one token equals one share out of 1,000 shares of the asset. That is clean on paper. The reconciliation problem arrives the first time a holder transfers to a wallet the SPV register does not recognize, or the first time a court-ordered reversal needs to unwind a transfer that has already settled on-chain.

Permissioned standards and enforced parity

Permissioned token standards like ERC-3643 push the transfer-eligibility check on-chain, so a transfer to an unverified wallet reverts at the protocol level rather than at the registrar's desk after the fact. That changes the reconciliation job from forensic to preventive.

Dimension | SPV Share Register | On-Chain Token Ledger |

|---|---|---|

Source of truth for ownership | Legal, corporate registry | Operational, distribution snapshot |

Update trigger | Signed transfer instrument | Confirmed blockchain transaction |

Transfer eligibility check | Manual KYC review | On-chain identity claim (ERC-3643) |

Reversal mechanism | Board resolution, registrar amendment | Issuer-controlled freeze and forced transfer |

Reconciliation cadence | Quarterly minimum | Per-block, automated |

Failure mode | Stale register, unrecorded transfers | Orphan tokens in inactive wallets |

What breaks when the two drift

The most common drift scenario is a secondary transfer that clears on-chain before the registrar updates the share register. For one or two days, the on-chain holder is entitled to distribution and the registered shareholder is the seller of record. If a distribution snapshot lands in that window, the wrong wallet receives funds. The fix is a forced freeze, a manual recovery, and an apology to two holders. Cap-table tooling that ties transfer authorization to register update (single-instruction, two-ledger) is the only way to keep the gap closed at scale, and most fund administrators have not repriced their service fees to reflect that work.

Corporate Actions and Capital-Event Governance

Refinancings, capex calls, lease renegotiations, and asset sales are the moments when fragmented ownership stops being a marketing line and becomes an operational constraint. A 200-holder cap table across multiple jurisdictions cannot vote the same way a five-LP fund votes, and the operating agreement has to acknowledge that before the first holder shows up.

Consider an illustrative scenario based on a structure several European issuers have adopted: a €50M portfolio of four assets held through a Luxembourg master SPV with local property-holding subsidiaries in Germany, Portugal, and outside the EU. The token sits at the master SPV level. A refinancing of the German asset requires lender approval, board consent, and, under the operating agreement, a 60 percent holder vote because it changes the debt service profile of the portfolio. The on-chain voting module collects signatures from 312 wallets across 22 countries. Three holders have lost access to their signing keys. Two are in jurisdictions where the original subscription has lapsed under local re-verification rules. The vote closes at 58 percent participation, below the quorum. The refinancing window expires.

The governance section of the operating agreement is the actual failure point, not the underlying protocol. Quorum thresholds written for institutional LP structures break when applied to retail-scale holder lists where, in practice, a meaningful share of wallets goes dark within the first year of issuance. CAIA's framing of asset tokenization as the representation of a real-world asset as a digital token on a blockchain understates one operational consequence: the digital token can be voted, but the human behind the wallet must still be reachable.

Workable governance designs follow three patterns. First, quorum is set against active wallets, those that have transacted or signed in the past 12 months, rather than against the full holder list. Second, routine operational decisions (lease renewals under a defined threshold, ordinary capex, insurance renewals) are delegated to the manager under the operating agreement and do not go to a token vote at all. Third, capital events with binding economic consequences carry extended voting windows, multiple notification channels, and a fallback to the registered SPV shareholder if the on-chain vote fails to reach quorum. This layered model is the one that survives a contested refinancing in year two.

Investor Reporting, Re-KYC, and Compliance Drift

Compliance does not freeze at the close of the issuance. Holder status changes, sanctions lists update, tax residency shifts, and accredited investor verifications expire. The compliance regime that approved the holder at subscription is not the compliance regime that governs the holder at month eighteen.

Periodic re-KYC and the silent expiry problem

Most jurisdictions require re-verification of holders at intervals defined by risk category, typically 12 to 36 months for standard retail and shorter for higher-risk profiles. Gofaizen & Sherle's guidance on commercial real estate tokenization stresses that the obligation falls on the issuer or its delegated administrator, not on the holder. A holder who ignores a re-KYC request is still on the cap table and still owns the token; the issuer is the one who fails its AML obligations if the verification lapses. The operational answer is to wire re-KYC into the same transfer-eligibility check that ERC-3643 uses for new transfers: an expired verification automatically disables the wallet's ability to receive new transfers and triggers a managed remediation flow before the next distribution.

Tax documentation across jurisdictions

Tokenized real estate generates US 1099 forms for US holders, K-1s where partnership structures are used, CRS reports for participating jurisdictions, and a long list of local equivalents. InnReg's compliance review of tokenized real estate documents how the same holder can require three or four parallel tax outputs depending on residency and the structure of the SPV. Generating those documents requires holder data that the on-chain ledger does not contain (tax IDs, residency declarations, beneficial ownership statements), and that data has to be refreshed at the same cadence as the KYC file.

Compliance drift

The slow failure mode is drift: each individual lapse looks minor, but eighteen months of accumulated lapses can produce a cap table where a double-digit share of holders has stale verification, missing tax forms, or undeclared residency changes. Legal Nodes' practitioner notes on real estate tokenization treat this as the dominant year-two risk for issuers who treat compliance as a one-time setup rather than a continuous workflow. The cure is staffing, not technology: a named operations owner with a calendar, not a dashboard.

Liquidity, Secondary Transfers, and Year-One Failure Modes

The InvestaX review of liquidity in tokenized assets puts the total tokenized RWA market at $31.9 billion by early June 2026, more than tripling since early 2025. The composition of that growth matters: tokenized US Treasuries lead at roughly $15 billion, followed by private credit at around $12 billion, with tokenized commodities (mostly gold) at about $5.5 billion, per RWA.xyz data cited in the same review. Real estate is a long way behind on both volume and turnover.

Tokenized gold spot trading hit $90.7 billion in Q1 2026, surpassing the $84.6 billion traded for all of 2025, and tokenized stocks reached $15.1 billion in spot trading volume in the same quarter, both per the CoinGecko 2026 RWA Report cited by InvestaX. Real estate does not have a daily mark, which is why secondary order books on most platforms remain thin and bid-ask spreads run wide enough to make small-ticket exits expensive.

The year-one failure modes follow from that liquidity gap. Holders who were told they could exit in 30 days discover the order book has two bids, both at a meaningful discount to NAV. At some venues, transfer agent capacity caps clear-throughput well below the pace promised at issuance. Atomic settlement between two whitelisted wallets fails when one wallet's KYC has silently expired. None of these breaks the deal economically, but each one breaks trust with the investor base, and trust is what funds the next vehicle. Issuers preparing for launch can review jurisdiction and lifecycle configuration options at Tokenizer.Estate and should treat the choice of fund administrator with post-issuance operational depth as the single most important pre-launch decision, ahead of platform, ahead of jurisdiction, ahead of token standard.

Tokenization success is measured in year one, where disciplined post-issuance operations separate functioning digital securities from broken ones. The issuance gets the announcement. The distribution that lands on schedule in month nine, on the right wallets, after a clean reconciliation against the share register: that is what gets the next allocation.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo