Fractional Real Estate Ownership via Tokens: Legal Structures, Investor Rights, and Platform Requirements

Explore how equity, debt, and hybrid token structures shape fractional real estate ownership, investor rights, and the platform infrastructure required to operate them.

A $12M mixed-use property in Lisbon is offered to 240 investors at $50,000 minimums through a Luxembourg SPV issuing ERC-3643 equity tokens. The same building, financed instead through a debt token paying 7.2% fixed yield, would demand a different legal architecture, a different disclosure regime, and a different compliance stack on the platform side. Fractional real estate ownership is one phrase, but it covers at least three distinct legal animals, and confusing them costs months of restructuring.

Developers and fund managers tend to treat the choice between equity, debt, and hybrid tokens as a financing question. It is a legal commitment that shapes investor rights, jurisdictional exposure, transfer mechanics, and what the issuance platform must enforce on every secondary trade for the life of the asset.

What Fractional Property Tokens Actually Represent

A property token is rarely a deed. In nearly every jurisdiction where real estate tokenization has matured, the token is a digital record of economic rights tied to an entity that holds the asset, not the asset itself. CAIA describes tokenization as the process of taking a real-world asset, or a specific right related to that asset, and representing it as a digital token on a blockchain. The asset stays put. What moves is the claim.

The claim moves through a wrapper. Tokenization typically involves a legal entity or contract that holds the property, most often a Special Purpose Vehicle (SPV), a single-purpose company set up to own one asset and issue securities backed by it. The token records a share in that SPV, or a debt claim against it, but the SPV remains the named owner on the land registry.

This distinction matters more than most issuers admit. As Gofaizen & Sherle put it, tokenized real estate represents economic rights, not direct title ownership. A token holder in a Frankfurt office building does not appear at the German land registry. The SPV does. The operative classification, then, is contractual: whatever rights the token confers, they flow through the corporate structure of the SPV and the offering documents that govern it. Get the wrapper wrong and the token gives investors less than the marketing claimed.

Three Legal Structures for Fractional Real Estate Ownership

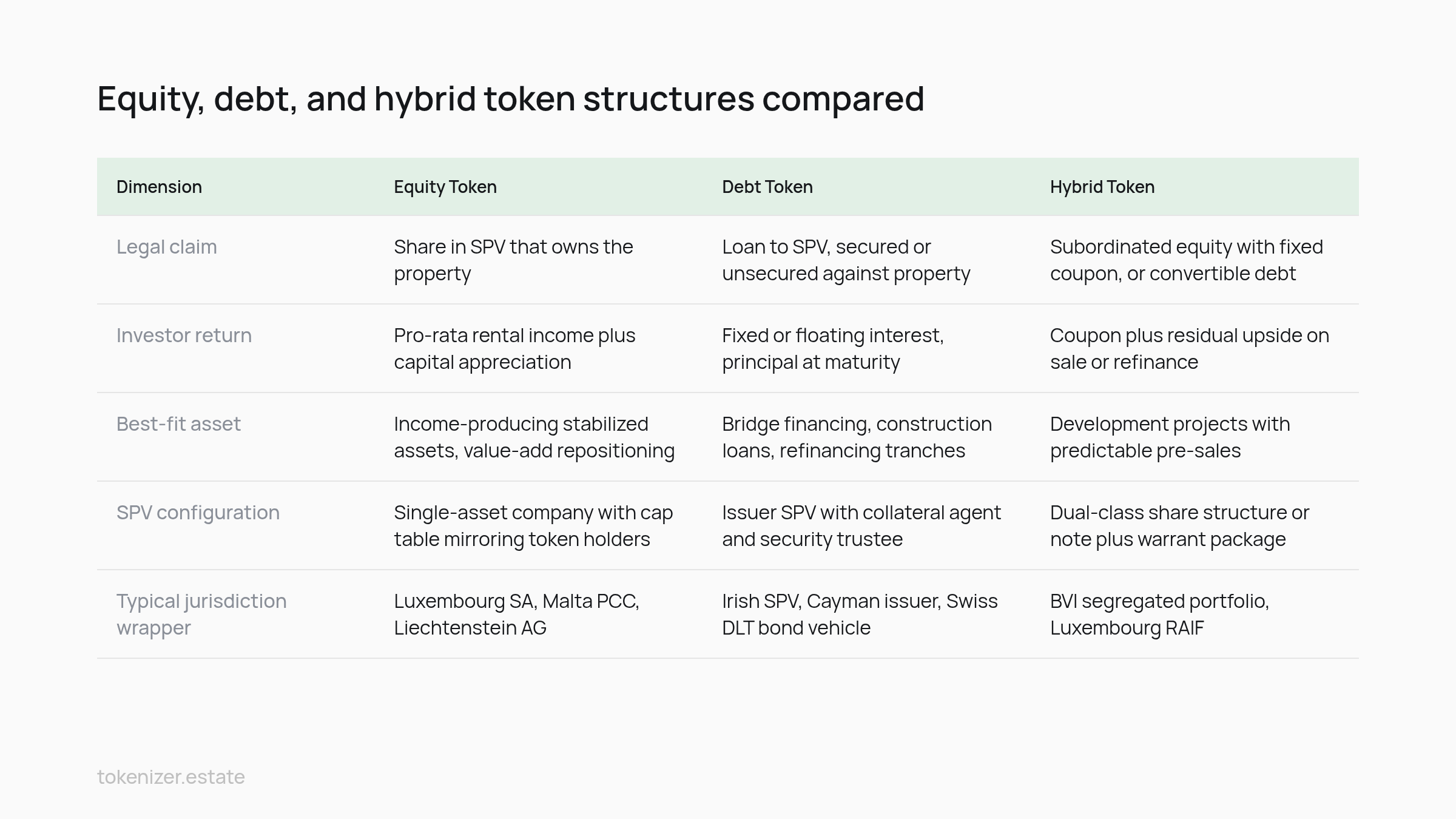

Equity, debt, and hybrid models are not interchangeable. Each one binds the issuer to a different set of obligations, fits a different asset profile, and demands a different SPV configuration. The table below sets the three side by side.

Dimension | Equity Token | Debt Token | Hybrid Token |

|---|---|---|---|

Legal claim | Share in SPV that owns the property | Loan to SPV, secured or unsecured against property | Subordinated equity with fixed coupon, or convertible debt |

Investor return | Pro-rata rental income plus capital appreciation | Fixed or floating interest, principal at maturity | Coupon plus residual upside on sale or refinance |

Best-fit asset | Income-producing stabilized assets, value-add repositioning | Bridge financing, construction loans, refinancing tranches | Development projects with predictable pre-sales |

SPV configuration | Single-asset company with cap table mirroring token holders | Issuer SPV with collateral agent and security trustee | Dual-class share structure or note plus warrant package |

Typical jurisdiction wrapper | Luxembourg SA, Malta PCC, Liechtenstein AG | Irish SPV, Cayman issuer, Swiss DLT bond vehicle | BVI segregated portfolio, Luxembourg RAIF |

Equity tokens: direct exposure to the asset's economics

Equity structures pass through everything, the rent, the vacancy, the cap-ex bills, the eventual sale price. Equity holders most resemble traditional shareholders, with voting rights, dividend rights, and residual claims on liquidation. The fit is strongest for stabilized income property, where investors want both yield and the optionality of appreciation. The cost is volatility: token NAV moves with the property's performance, and distributions can drop to zero in a bad quarter.

Debt tokens: yield instruments backed by property

Debt token structures convert a property into collateral, not into a shared ownership pool. The investor lends to the SPV at a defined rate, receives periodic coupons, and is repaid at maturity (or, in default, has recourse to the security package). LegalNodes notes that this model often suits bridge financing and construction tranches, where the underlying cash flows are predictable and the issuer wants to avoid diluting equity. Investors get bond-like behavior. They give up the upside.

For developers, this is often the right answer when refinancing a stabilized asset or funding a discrete tranche of construction. Token holders are creditors. The platform side has to handle interest accruals, redemption schedules, and default waterfalls, closer to a bond administrator than an equity registrar. The decision logic between debt and equity tokens is unpacked in detail in debt vs equity sequencing.

Hybrid tokens: structured returns for transitional assets

Hybrid instruments fit the awkward middle, assets that aren't yet stabilized but will produce predictable cash flow once leased. A typical structure pairs a fixed coupon during a stabilization period with conversion or participation rights once the asset hits target occupancy. The complexity is real, and the documentation burden grows with each contingent right.

Investor Rights Attached to Each Token Type

Rights diverge sharply at the moment something goes wrong. In normal operations, an equity token holder and a debt token holder both receive distributions on schedule and rarely interact with the issuer. The differences appear at refinancing, sale, default, or governance vote.

Consider a 50-unit residential building in Porto held by a Maltese SPV. Equity token holders typically have voting rights on major actions (sale of the asset, replacement of the property manager, amendment of the operating agreement), usually weighted by token holdings and triggered by supermajority thresholds. Legal analysis from Pence Firm highlights that information rights also attach: annual audited financials, quarterly performance reports, notice of material events. Debt token holders in the same building would have none of these. Their right is to be paid. If they are paid, they have no standing to object to the property manager or the sale price.

The picture shifts when the building is sold for less than expected. Debt holders are paid first from the proceeds, up to principal plus accrued interest. Equity holders take what remains, which may be nothing. In a forced sale, debt holders can typically accelerate and trigger enforcement against the collateral; equity holders cannot.

Distribution mechanics differ structurally. Equity distributions are discretionary, the SPV board declares a distribution, often quarterly, based on net cash flow after reserves. Debt coupons are mandatory; missing one is an event of default. Chainlink's overview of fractional ownership infrastructure notes that smart contract design must reflect this: equity distribution contracts allow variable amounts and discretionary timing, while debt contracts enforce fixed schedules with default triggers.

Redemption is where hybrid structures show their value. Pure equity tokens have no contractual redemption, the only exit is secondary sale or asset disposal. Pure debt tokens redeem at maturity. Hybrids can build in scheduled partial redemptions, put options exercisable after stabilization, or call rights for the issuer. Each redemption mechanic creates platform requirements: identity-verified payout addresses, tax withholding logic, and on-chain burn of redeemed tokens.

Jurisdictional Treatment of Fractional Token Holders

A 50-unit residential building in Porto, Portugal.

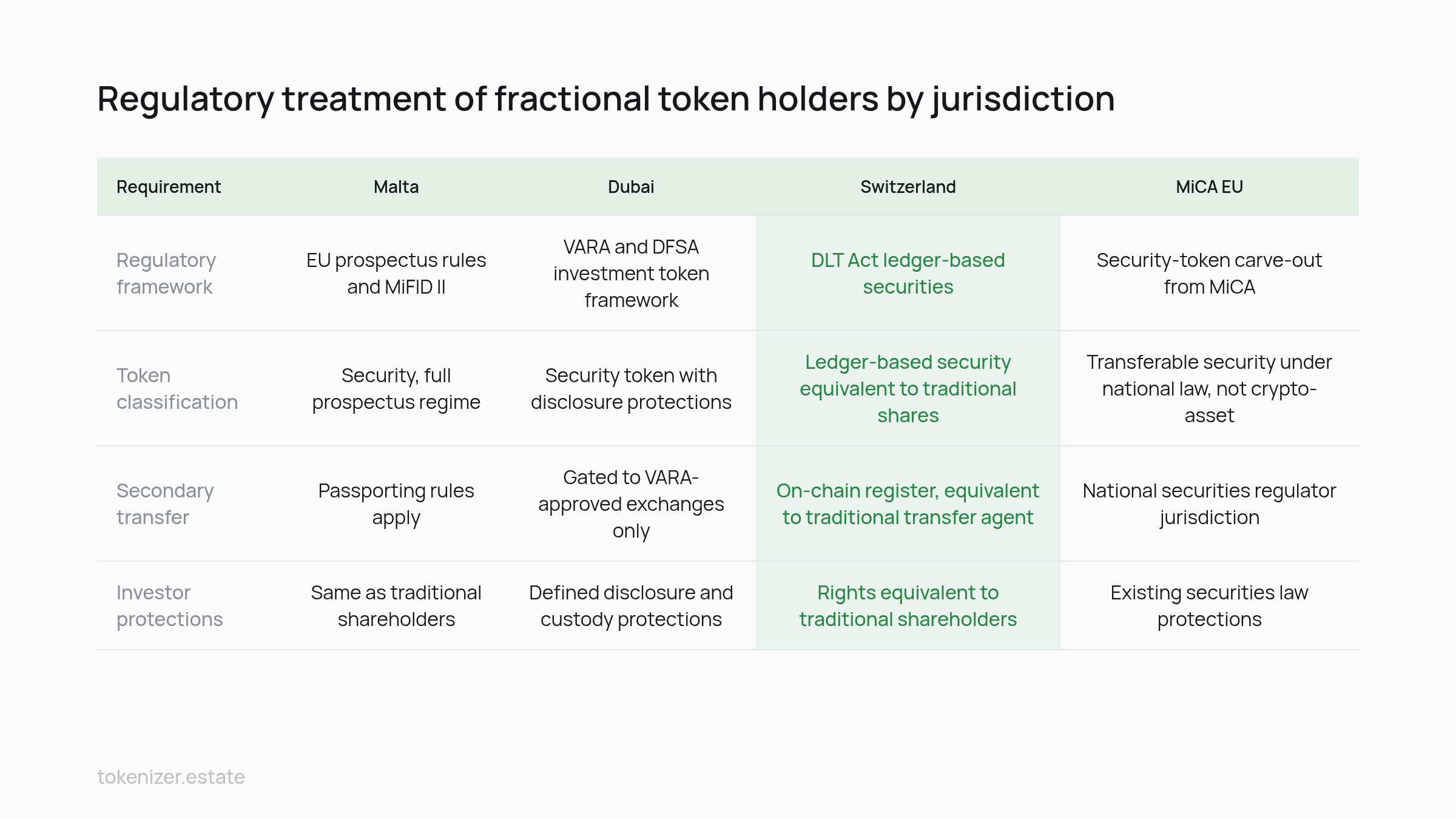

Where the SPV sits determines what fractional token holders actually own, and what protections they get. Gofaizen & Sherle identify Malta, Dubai, and Switzerland as the three jurisdictions where structure determines the regulatory outcome, alongside the EU's MiCA-regulated markets where the classification logic is more rigid.

Malta and the EU security token path

Maltese SPVs issuing equity tokens fall under EU prospectus rules and MiFID II investor protections. The token is a security, full stop, and fractional holders get the same disclosure rights as shareholders in a traditional Maltese private company. MiCA does not change this: Tokeny's analysis confirms that tokenized securities remain governed by existing securities law, not by MiCA's crypto-asset regime. The implication is workflow continuity: prospectus exemptions, qualified investor thresholds, and passporting rules apply unchanged. The detailed mechanics of MiCA's reach into property token issuance are covered in the MiCA-regulated markets analysis.

Dubai's VARA framework

Dubai treats fractional real estate tokens through the Virtual Assets Regulatory Authority (VARA) and, for the DIFC, through the DFSA's investment token framework. Fractional holders here are recognized as security token holders with defined disclosure and custody protections, but transferability is gated by VARA-approved exchanges. The structural implication: secondary liquidity is permitted only through licensed venues, which constrains the global trading pattern many issuers initially imagine.

Switzerland's DLT Act

Switzerland's DLT Act recognizes ledger-based securities as a distinct legal category. Fractional token holders of a Swiss SA's tokenized shares have rights equivalent to traditional shareholders, with the register held on-chain rather than at a transfer agent. This is the cleanest legal recognition of tokenized fractional ownership in any major jurisdiction.

MiCA and the security-token carve-out

Under MiCA, security tokens are explicitly outside scope. Databird Journal's review of MiCA's security-token carve-out makes the point sharply: a fractional property token classified as a transferable security under MiFID II remains under national securities regulators, not under MiCA's crypto-asset rules. This creates a clean dividing line for issuers but a messy one for platforms, which must handle both regimes.

One operational constant cuts across all four jurisdictions: timing. Gofaizen & Sherle put typical project timelines at 4–8 months, with banking onboarding most often the bottleneck. The legal entity can be incorporated in weeks. The bank account for the SPV is what delays the launch.

Platform Infrastructure Requirements by Tokenized Fractional Ownership Model

Dubai's financial district, a hub for virtual asset regulation.

Each structure imposes a different load on the issuance platform. The compliance enforcement that worked for an equity token in Liechtenstein will not, without significant reconfiguration, handle a debt token issued from an Irish SPV under Luxembourg listing rules.

The common thread is permissioned transfer. The ERC-3643 protocol is an open-source suite of smart contracts that enables the issuance, management, and transfer of permissioned tokens, meaning every transfer is validated against an on-chain compliance layer before it settles. For fractional real estate, this is the binding requirement: a token holder in a restricted jurisdiction cannot transfer to another restricted-jurisdiction wallet, and the contract enforces this without manual intervention.

Identity is the second layer. ERC-3643 includes a built-in decentralized identity framework, ONCHAINID, that ensures only users meeting predefined conditions can become token holders, even on permissionless blockchains. Equity token holders need full accredited-investor verification with periodic re-attestation; debt token holders need KYC plus tax-residency confirmation for withholding logic; hybrid token holders need both, plus conversion-event eligibility checks. The platform stores the credentials. The contract reads them on every transfer.

Corporate actions are where models diverge most. Chainalysis's architecture review notes that ERC-3643 supports forced transfers, freezes, and recovery, non-negotiable for equity structures where court orders, inheritance, and regulatory actions must be enforceable on-chain. Debt structures also require interest-accrual contracts, redemption agents, and default-trigger logic. Hybrid structures require all of the above plus conversion mechanics.

The point is selection, not maximalism. Institutional adoption of ERC-3643 has grown precisely because the standard is modular: issuers configure only the modules their structure needs. A platform that forces equity-token infrastructure onto a debt issuance creates operational overhead and investor confusion. The infrastructure choices that distinguish a closed deal from a stalled one are outlined in the infrastructure decisions framework.

Market Trajectory and Decision Framework for Fractional Real Estate Ownership

Deloitte's market analysis projects that the global market for commercial real estate tokenization will expand significantly by 2035, with estimates reaching up to USD 4 trillion in tokenized real estate over that horizon. The figure carries a methodology caveat: it assumes continued regulatory clarity across major jurisdictions and adoption by institutional asset managers at scale, neither of which is guaranteed.

The market reference point is larger still. The ERC-3643 documentation notes that securities, as a category, represent a global market of more than 100 trillion dollars. Real estate tokenization is competing for share within that universe, not creating a separate market.

The decision framework reduces to asset profile. Stabilized income property with predictable cash flow and a 5–10 year hold suits equity tokens: investors want yield plus appreciation, and the SPV can sustain quarterly distributions. Bridge financing, construction tranches, and refinancing packages suit debt tokens: the cash flows are defined, the duration is shorter, and investors prefer fixed return over upside. Development assets with stabilization pathways suit hybrids: the coupon de-risks the early period, and conversion captures the lease-up gain.

Choosing between these is a legal commitment that locks in investor rights, jurisdictional exposure, and platform configuration for the asset's full lifecycle. Restructuring after issuance is expensive and erodes investor trust. Issuers preparing a fractional offering can review the structure-by-structure configuration options at Tokenizer.Estate before committing to a model.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo