Tokenization Architecture for Real Estate: How the Standard, Chain, and Platform Fit Together

Most tokenization guides stop at the checklist. This decision guide goes deeper into the infrastructure choices that determine whether a real estate deal actually closes.

The most expensive tokenization mistakes are made in week one, in the architecture. A generic ERC-20 contract that cannot block secondary transfers to non-accredited wallets will pass testing and still fail compliance review, because the placement memorandum promised a restriction the standard cannot enforce. The fix is a redeploy on a permissioned standard, and the cost is weeks of delay that the right choice up front would have avoided.

That is the layer most checklist guides skip. The architecture, the token standard, the chain, the platform tier, and the integration scope, decides whether a deal closes cleanly long before any platform is selected.

Why Tokenization Architecture Front-Loads Deal Risk

Asset tokenization, in plain terms, is the process of taking a real-world asset or a defined right tied to it and representing it as a digital token on a blockchain. That definition sounds neutral. The infrastructure choices behind it are not.

The market projections explain why issuers keep being told to move fast. Widely cited forecasts put tokenized real-world assets near $16 trillion by 2030, drawing on figures circulated by major research firms. Deloitte, the same aggregation notes, projects tokenized real estate alone could grow from under $300 billion today to about $4 trillion by 2035. These are projection ranges built on adoption assumptions, not measured market size, they belong in the strategy deck, not the pricing model.

The structural implication is sharper than the headline numbers suggest. Once a token standard is chosen, the chain is committed, and the platform tier is signed, every downstream decision: compliance enforcement, investor onboarding, distribution mechanics, secondary transfer, runs through those rails. Switching later means redeploying the contract and re-onboarding holders. The infrastructure stack front-loads the risk. The rest of this article walks through the four decisions that define it: standard, chain, platform tier, and integration scope.

Choosing an ERC-3643 Real Estate Token Standard vs ERC-1400

Two security token standards dominate institutional real estate issuance, and they solve overlapping but distinct problems. ERC-3643 is a permissioned standard: tokens can only be held and transferred by identities that satisfy predefined compliance rules such as KYC, AML, and investor eligibility checks, per the QuickNode technical guide. Originally known as T-REX (Token for Regulated EXchanges) and initiated by Tokeny, the standard is now formalized under the ERC-3643 Association.

Mechanically, ERC-3643 is a suite of smart contracts: on-chain identity and claims through ONCHAINID, identity registries for eligible holders, modular compliance rules, and a token contract that enforces them on every transfer. The compliance check is not optional. The contract reverts if the rule fails.

ERC-1400 takes a different posture. It is a combination of new and existing standards meant to create a unified framework for all security tokens, building on the earlier ST20 protocol. Its scope is broader: publicly traded equity and bonds, private placements, real estate, fine art, synthetic baskets. The flexibility comes from a partition model: a single token can carry multiple share classes with different rights.

When ERC-3643 Fits

The fit is strongest where the cap table is institutional, the regulator is European or American, and the issuer wants compliance enforced at the protocol layer rather than at the wallet layer. EU issuers under MiCA, US Reg D offerings, and Middle East deals routed through DIFC or ADGM map cleanly to ERC-3643 because the identity claims system handles cross-jurisdictional eligibility without custom code.

When ERC-1400 Fits

ERC-1400 fits issuers with multi-class structures, preferred and common share classes in one entity, debt and equity tranches in the same SPV (Special Purpose Vehicle), or planned conversion mechanics. The partition model handles these natively. The trade-off is implementation cost: ERC-1400 has fewer turnkey vendors and more bespoke deployment work.

Side-by-Side Decision Table

Dimension | ERC-3643 (T-REX) | ERC-1400 |

|---|---|---|

Governance body | ERC-3643 Association | Polymath, community fork |

Compliance enforcement | On-chain via ONCHAINID and identity registry | Partition-level, document-linked |

Multi-class support | Single class, modular rules | Native partitions for share classes |

Best-fit deal profile | Single-asset SPV, institutional cap table, EU/US/ME | Multi-tranche structures, hybrid debt/equity |

Vendor availability | Multiple white-label operators | Narrower, more bespoke builds |

Transfer restriction model | Reverts on failed compliance check | Partition-level rules per share class |

The classification that matters is whether the deal needs one share class with strict transfer rules, or multiple classes with different economic rights. The first case maps to ERC-3643. The second case is where ERC-1400 earns its complexity. For most single-asset real estate SPVs, the answer is ERC-3643, which is why it is increasingly described as the standard driving institutional finance flows.Readers comparing vendor stacks can also work through the platform comparison for 2026.

Matching Blockchain Selection to Deal Size and Investor Base

Chain choice is downstream of standard choice, but the constraints are different. The binding limit on this is settlement cost per transfer relative to deal economics, plus the regulatory posture of the chain itself.

Ethereum mainnet remains the default for institutional cap tables. ERC-3643 deployments dominate there, settlement is final, and custody integrations with Fireblocks, Anchorage, and BitGo are mature. The trade-off is gas cost: a transfer that costs $8 in fees is acceptable on a $250,000 institutional ticket and absurd on a $500 retail one. Above roughly $100,000 average ticket size, Ethereum mainnet is generally the cleanest choice.

Polygon is where fractional retail issuance has concentrated. The economics flip — transfers cost cents, secondary trading is viable, and the EVM compatibility means ERC-3643 contracts deploy with no rewrite. Issuers running a 1,000-investor retail tranche on a single residential building typically land here. The trade-off is institutional optics: some custodians still treat Polygon balances as a secondary-chain exposure, which can slow onboarding for larger LPs.

Purpose-built chains take a third posture. Polymesh is built specifically for regulated security tokens — the network markets itself as infrastructure to tokenize real estate. Polymesh has had regular third-party audits and zero security exploits since launch, and node operators are known and licensed, not anonymous. That last point matters for regulators reviewing the chain itself as part of the deal.

A working chain-selection rule looks like this. Institutional deal, fewer than 100 holders, ticket size above $100K — Ethereum mainnet. Retail or fractional deal, hundreds to thousands of holders, ticket size below $25K — Polygon or another low-fee EVM chain. Regulated issuer wanting protocol-level identity guarantees and licensed validators — Polymesh or a comparable permissioned chain.

The token model also matters. The CAIA framing distinguishes fungible tokens — interchangeable units where each token represents, say, one share out of 1,000 in the asset — from non-fungible tokens that represent unique rights or specific units. For most real estate equity tokenization, the fungible model is the default; non-fungible structures appear when individual units (a specific apartment, a specific parking space) need distinct identifiers on-chain.

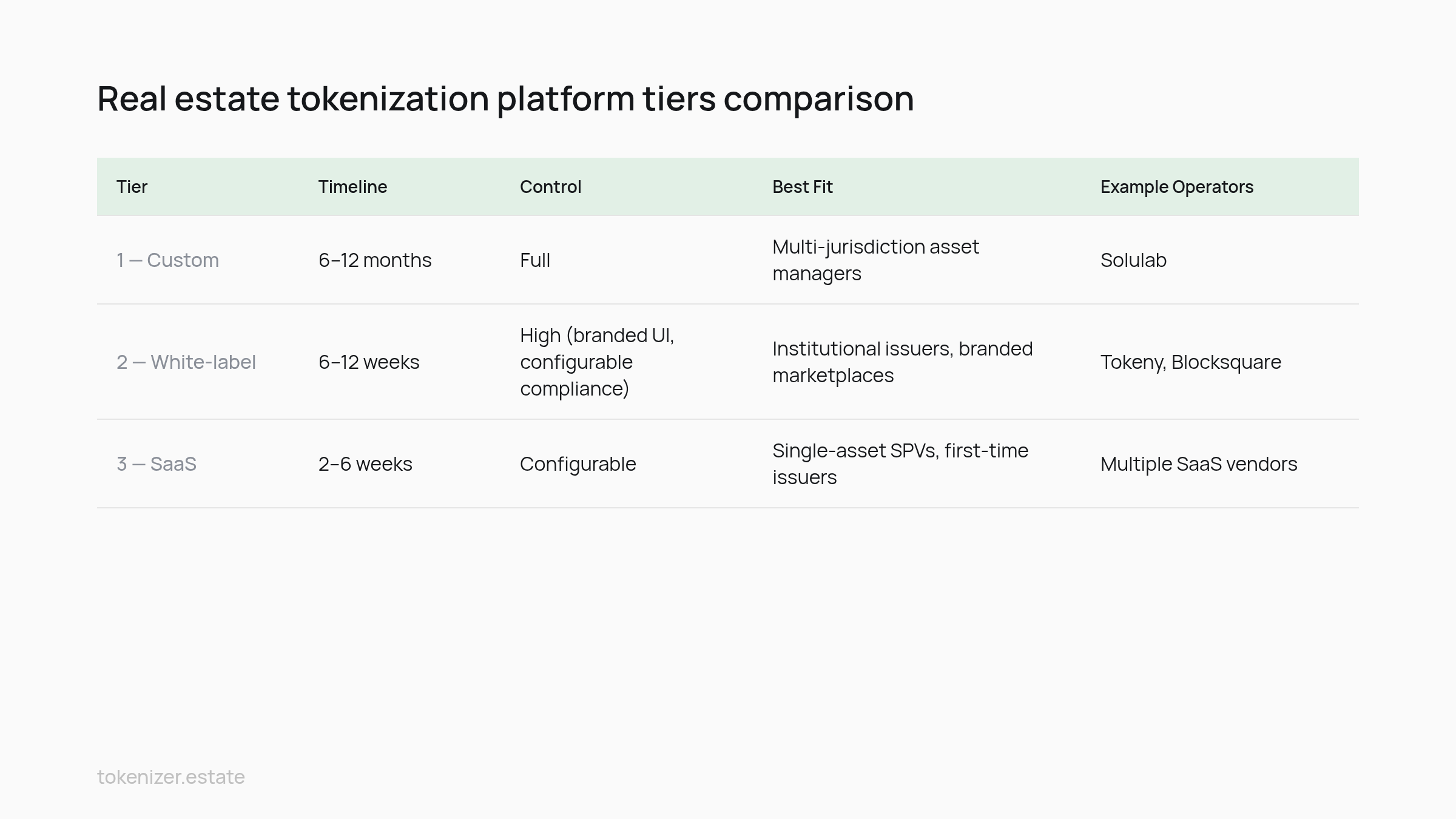

White Label Tokenization Platform vs Custom Build: The Tier Decision

The platform decision is where most issuer budgets actually go. Providers group into three engagement tiers based on how much of the stack the issuer controls.

Tier 1: Custom Build

Tier 1 is a full platform built to the issuer's specification: maximum flexibility, longer timeline. Enterprise-build vendors in this tier typically support both ERC-3643 and ERC-1400 across multiple chains and jurisdictions. Custom builds make sense when the issuer is a large asset manager planning recurring issuance across several markets and wants the IP in-house. The cost is six to twelve months of build time and a development budget that starts at seven figures.

Tier 2: White-Label

Tier 2 is proven infrastructure rebranded for the issuer. Institutional white-label operators in this tier run ERC-3643 with banking-grade compliance for issuers who want the brand and the investor relationship without owning the code; marketplace-oriented white-label platforms run on Ethereum with document storage layers for operators launching a branded venue quickly. The white-label tier compresses launch timelines to weeks rather than months and shifts compliance engineering risk to the vendor.

Tier 3: SaaS

Tier 3 is shared-tenant SaaS. The issuer configures jurisdiction, eligibility rules, and branding on an existing platform without touching code. Launch is fastest. Control is lowest — the issuer cannot change the compliance engine or the chain. For a single-asset SPV testing the model, this is often the right entry point.

Tier Comparison

Tier | Timeline | Control | Best Fit | Operator type |

|---|---|---|---|---|

1 — Custom | 6–12 months | Full | Multi-jurisdiction asset managers | Enterprise-build vendors |

2 — White-label | 6–12 weeks | High (branded UI, configurable compliance) | Institutional issuers, branded marketplaces | Institutional white-label operators |

3 — SaaS | 2–6 weeks | Configurable | Single-asset SPVs, first-time issuers | Shared-tenant SaaS platforms |

The real constraint here is whether the issuer plans one deal or twenty. One deal does not justify Tier 1 economics. Twenty deals do not survive Tier 3 constraints. Most fund managers landing in this market sit in Tier 2 — which is also where the broader vendor field is most competitive. A deeper read on the operator landscape sits in the companies comparison.

Three Integration Points Issuers Underestimate When They Tokenize Real Estate

The token is the easy part. The integration layer is where deals leak. Real estate tokenization means turning property rights into digital tokens on a blockchain, each token representing a defined slice of value or ownership based on how the deal is structured. That definition implies three integrations the smart contract alone does not handle.

Cap Table Sync

The on-chain holder registry is the cap table — or it should be. In practice, most issuers run a parallel off-chain cap table in spreadsheets or a registrar tool, then reconcile to the chain monthly. The reconciliation breaks the first time a holder transfers tokens to a new wallet without notifying the registrar. This is the most common operational failure in tokenized cap-table management: the chain shows one holder list, the corporate registry shows another, and distributions go to the wrong addresses. The fix is treating the on-chain registry as the source of truth, with the off-chain record derived from it, not the reverse.

Payment Rail for Distributions

The rental income arrives in fiat — euros or dollars from the property manager into the SPV's bank account. Distributing it to token holders means choosing the rail: stablecoin distribution on-chain, fiat distribution via bank transfer keyed to the on-chain registry, or a hybrid. Polymesh's framing of what real estate tokens actually represent — ownership of part of a property, ownership of an entire property, equity interest in a controlling entity, or interest in debt secured by the property — matters here because each ownership type has a different cash flow profile. Equity distributions are quarterly and variable; debt coupons are monthly and fixed. The payment rail must match the cash flow rhythm or the operations team rebuilds the distribution logic every quarter.

Investor Portal and Reporting

Holders want to see their balance, their distribution history, their tax documents, and the underlying asset performance. The smart contract exposes the balance. Everything else is portal work — and the portal needs to read both on-chain state and off-chain operational data (occupancy, rent roll, expenses). End-to-end platforms bundle the portal with the issuance stack precisely because issuers who skip this layer end up emailing PDF reports to hundreds of wallets every quarter. The cost of building the portal late is always higher than building it during launch.

A Decision Sequence for Selecting Your Tokenization Stack

The decisions stack in a specific order, and reordering them creates rework. First, jurisdiction: the legal wrapper and applicable regulator constrain everything downstream. Second, token standard: ERC-3643 for single-class permissioned, ERC-1400 for multi-class structures. Third, chain: driven by ticket size and investor profile. Fourth, platform tier: custom, white-label, or SaaS based on issuance frequency. Fifth, integration scope: cap table, payment rail, portal.

The market context for these decisions is large enough that the marginal cost of getting them right is small relative to the asset value at stake. The global property market reached about $379 trillion in 2022 by widely cited estimates. Even a fractional share of that flowing on-chain rewards issuers who built the stack correctly the first time. The ones who skip the sequence end up redeploying contracts, re-onboarding holders, and explaining to investors why distributions are late.

The architecture decided before the smart contract is deployed, the token standard, the chain, the platform tier, and the integration scope, together determine whether a deal closes cleanly or leaks at every handoff. Tokenizer.Estate provides the software layer for this, and can help you think through how the pieces fit together before you commit to a build.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo