Tokenized Real Estate in MiCA-Regulated Markets: What the EU Framework Means for Property Token Issuers

A practical guide for EU real estate developers structuring property token offerings under MiCA, using a 20M euro residential portfolio as the reference case.

A Frankfurt-based fund manager opens a structuring memo on a €20M residential portfolio split across Germany, France, and Luxembourg. The first decision on the page — security token under MiFID II or asset-referenced token under MiCA real estate tokenization rules — sets the licensing cost, the distribution scope across the EU, and whether rental yield can legally flow to token holders at all.

That single classification call, made in week one, determines whether the deal closes in six months or stalls in a regulator's queue for two years. The rest of the cap table waits on it.

Why MiCA Reshapes Real Estate Tokenization in 2026

The regulatory ground under European property tokenization shifted decisively in late 2024. The Markets in Crypto-Assets Regulation entered into force in June 2023, but force-of-law and applicability are different milestones. The second one is what changes deal structuring.

As of 30 December 2024, the second phase of MiCA became directly applicable across every EU member state, as K&L Gates documents. Any property token offered to EU investors from that date forward must be classified against MiCA's definitions before it touches a primary distribution channel.

That classification step is exactly what the Frankfurt fund manager is doing this week. The €20M residential portfolio can be structured as a security token under MiFID II, an asset-referenced token under MiCA, or — in the wrong hands — as an unregistered crypto-asset that ends up on a non-compliant register published by ESMA. The three routes carry different capital requirements, different distribution rights, and different rules on whether yield is permitted at all.

The structural implication is plain: the regime no longer rewards waiting. Issuers who delay the classification decision push every downstream workstream — SPV setup, custody, white paper drafting, CASP onboarding — into a compressed quarter with no slack.

SPV (Special Purpose Vehicle): a separate legal company created only to hold the property, so investors own shares in that company rather than the building directly. Custody: a licensed service that holds and safeguards digital tokens on behalf of investors.

MiCA Scope vs MiFID II: Where Property Tokens Actually Land

Most real estate tokens issued in the EU fall outside MiCA entirely and into MiFID II as financial instruments. The classification logic is straightforward: if the token represents an ownership or debt claim on a property-holding entity, it is a transferable security, and MiFID II governs it. Headline coverage of MiCA tends to bury this point.

MiCA defines a crypto-asset as a digital representation of value or a right that can be transferred and stored electronically using distributed ledger technology, per AMF France. The regulation then carves out anything that already qualifies as a financial instrument under MiFID II. Security tokens — the dominant structure for real estate — sit in that carve-out. Analyses from Tokeny, Solidus Labs, and Merkle Science converge on the same conclusion: tokenized securities are largely unaffected by MiCA's authorization and white paper regime.

The phased rollout matters here. The first MiCA phase applied from 30 June 2024, covering asset-referenced and e-money tokens. The broader CASP regime followed at the end of that year, as K&L Gates documents. The DLT Pilot Regime, separate from MiCA, lets regulated institutions test trading and settlement of tokenized securities under a sandbox framework, per Legal Nodes.

Smart contract: a piece of code stored on a blockchain that runs automatically when set conditions are met — for example, sending rental income to token holders each month without a bank in the middle.

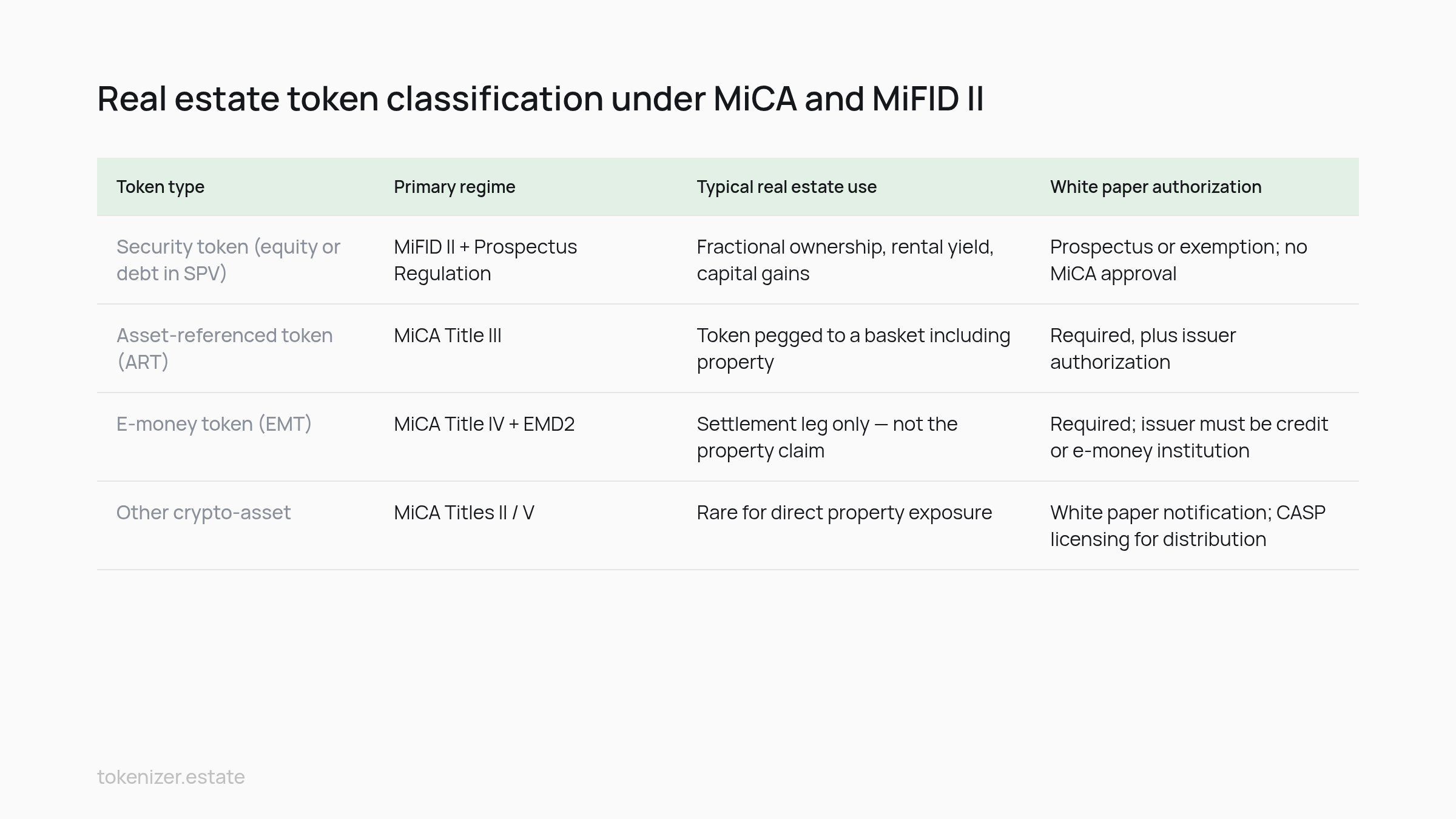

Classification at a glance

Token type | Primary regime | Typical real estate use | White paper authorization |

|---|---|---|---|

Security token (equity or debt in SPV) | MiFID II + Prospectus Regulation | Fractional ownership, rental yield, capital gains | Prospectus or exemption; no MiCA approval |

Asset-referenced token (ART) | MiCA Title III | Token pegged to a basket including property | Required, plus issuer authorization |

E-money token (EMT) | MiCA Title IV + EMD2 | Settlement leg only — not the property claim | Required; issuer must be credit or e-money institution |

Other crypto-asset | MiCA Titles II / V | Rare for direct property exposure | White paper notification; CASP licensing for distribution |

The operative classification

For a €20M residential portfolio with rental distributions, the operative classification is almost always a security token under MiFID II. The token gives the holder a claim on an SPV that owns the buildings, and that claim is transferable on a DLT — a textbook transferable security in digital form. MiCA enters the structure only at the edges: a euro-denominated EMT used to settle distributions, or a stablecoin rail for cross-border subscriptions. Issuers building this stack typically follow a sequenced tokenization checklist that locks classification first, before any technical work begins.

The Asset-Referenced Token Trap for Property Issuers

Some issuers — usually those who arrive at tokenization from the crypto side rather than from real estate — try to structure a property token as an asset-referenced token. The thinking is that an ART can reference a basket of real-world assets, including buildings, and therefore offers a cleaner regulatory wrapper than securities law. The structure breaks on contact with MiCA's actual obligations.

ART issuance under MiCA requires the issuer to be an EU-registered legal entity, to get authorization from the competent national authority, and to publish a white paper approved by that authority, per Manimama. Minimum capital sits at €350,000 or 2% of the reserve assets, whichever is higher. The issuer must also hold a segregated reserve covering the token's value at all times. For a €20M residential portfolio, that reserve requirement would force the issuer to hold the buildings inside a structure that mirrors the token supply — operationally indistinguishable from a regulated fund, but without the corresponding distribution benefits.

The harder rule comes next. MiCA prohibits ART issuers from granting interest on the tokens. In tokenization terms, this prohibition reaches further than coupon payments. Rental yield distributed proportionally to token holders sits inside the same prohibition zone if the distribution looks like a return on the held position rather than a dividend from a corporate entity.

This is where the ART route breaks economically. A residential portfolio generates rental income; that income is the entire investor case. A structure that legally cannot pass through yield to token holders turns an income asset into a pure capital-appreciation play. It mis-prices the deal and shrinks the addressable investor base. Compliance commentary from Aurum Law and RWA.io reaches the same operational conclusion: ARTs suit stablecoin-like instruments. They do not suit cash-flowing property exposure.

The binding limit on this route is the interest-prohibition rule. Everything else — capital, reserve, white paper — can be engineered around with enough budget. Rental yield cannot.

EU Jurisdictions for MiCA Real Estate Tokenization

Once the classification settles on a security token under MiFID II, the next question is jurisdiction. Three EU member states — Luxembourg, France, and Germany — currently offer the most workable paths for real estate token issuers, each with a distinct interface between national DLT law, the local financial regulator, and land registry practice.

Luxembourg: the DLT-first route

Luxembourg moved aggressively to position itself as the EU's tokenization hub. The country adopted Blockchain Law IV in December 2024 to strengthen DLT use within financial and tokenization frameworks, per FIBREE. In February 2025, Blocksquare launched an EU-compliant real estate tokenization framework in Luxembourg, integrating with land registries and relying on notarized agreements to enforce economic rights, also per FIBREE. EY Luxembourg documents how the country's securitization vehicle (SV) regime pairs with DLT to create issuance structures that are both bankable and tokenizable.

France: AMF supervision and the PACTE transition

France took a different path. The French framework introduced by the PACTE Law of 22 May 2019 — which set up a specific regime for Initial Coin Offerings and digital asset service providers — is being phased out as MiCA takes over, per AMF France. For security tokens, AMF supervision under the Prospectus Regulation and MiFID II remains the operative regime, and France's DLT pilot regime participation gives institutional issuers a sandbox for trading venues.

Germany: BaFin and the eWpG

Germany's Electronic Securities Act (eWpG) lets issuers create electronic securities — including crypto securities — on a DLT register without a physical certificate. BaFin supervises both the crypto custody license and the CASP authorization process, with detailed implementation notes published by Bundesbank. A comparative analysis from Antier Solutions notes that German issuers benefit from explicit statutory recognition of tokenized securities, which simplifies the legal opinion stack at deal closing.

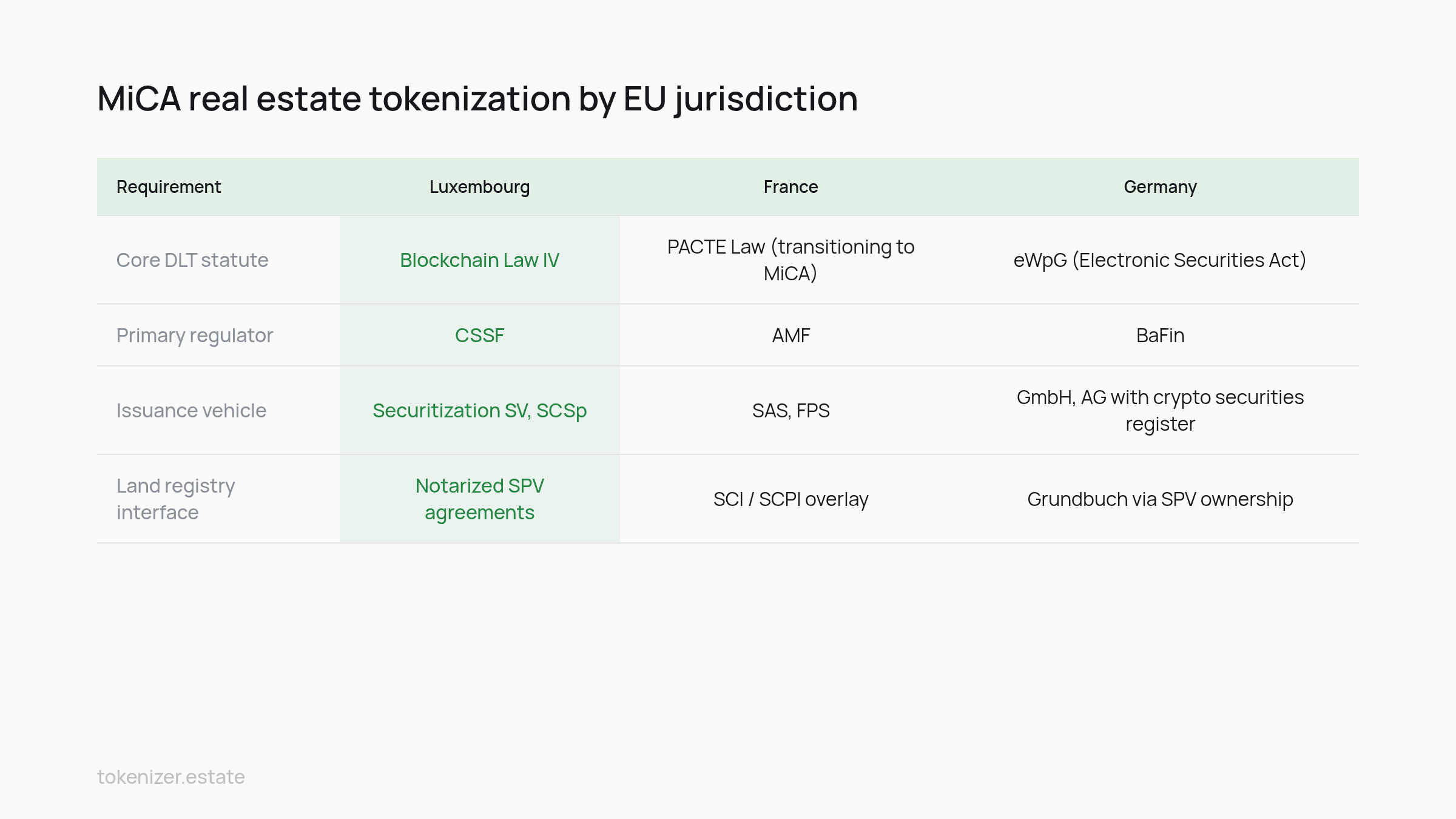

Jurisdiction comparison

Dimension | Luxembourg | France | Germany |

|---|---|---|---|

Core DLT statute | Blockchain Law IV | PACTE Law (transitioning to MiCA) | eWpG (Electronic Securities Act) |

Primary regulator | CSSF | AMF | BaFin |

Issuance vehicle | Securitization SV, SCSp | SAS, FPS | GmbH, AG with crypto securities register |

Land registry interface | Notarized SPV agreements | SCI / SCPI overlay | Grundbuch via SPV ownership |

MiCA Property Tokens: Practical Compliance Stack

For the €20M Frankfurt portfolio, the compliance stack splits cleanly into two layers. The property claim — the security token itself — runs through MiFID II, Prospectus Regulation exemptions, and national securities law. MiCA enters only at the distribution and settlement layer, where any crypto-asset service provider touching the token must hold a CASP license, and where any euro-denominated stablecoin used for subscription or distribution falls under MiCA Title IV.

The CASP licensing pathway is the operationally heavy piece. AMLBot documents the full authorization process — governance, capital, AML, custody segregation, and complaint handling — and confirms that a CASP license passports across all member states once granted. That passporting is the operational upside that justifies the licensing cost for any issuer planning multi-country distribution.

The transparency layer sits with ESMA. Articles 109 and 110 of MiCA give ESMA the power to publish a central register of crypto-asset white papers, authorized crypto-asset service providers, and non-compliant entities. The interim register is available on the MiCA webpage as a collection of CSV files until mid-2026, when it will be formally integrated into ESMA's main register infrastructure. Issuers should expect their CASP and any notified white papers to appear there.

For the white paper itself, MiCA notification (where applicable) is procedural rather than approval-based for non-ART, non-EMT crypto-assets. Security tokens skip this step entirely and run through Prospectus Regulation mechanics instead, with national exemption thresholds doing most of the work for sub-€8M tranches, per Decta. The KYC and AML stack for tokenized securities stays the same on both layers — investor onboarding, source-of-funds checks, ongoing screening — and reuses across the security token and any stablecoin rail.

KYC (Know Your Customer) and AML (Anti-Money Laundering): checks that verify who an investor is and where their money comes from, required by law before any token can be sold to them.

EU Real Estate Token Compliance: Market Signals and Structuring Verdict

The market data points clearly in one direction. Europe held approximately 23.6% of the global tokenization market in 2024, with its real estate tokenized segment valued at USD 1.23 billion and projected to grow strongly toward 2034, per FIBREE — methodology caveats apply, as the figure aggregates issuance volumes across heterogeneous platforms. Platform-level traction reinforces the picture: by mid-2025, Blocksquare had surpassed USD 200 million in tokenized real estate assets across 66 properties in 29 countries, while DigiShares reported surpassing USD 1 billion of tokenized assets volume on its platform, both per FIBREE.

Both platforms route real estate primarily through security token structures, with MiCA components confined to settlement rails. CryptoVerse Lawyers identifies this as the dominant 2026 model — and the structuring logic behind it is consistent with everything the classification analysis shows.

The verdict for the Frankfurt fund manager, and for most EU real estate issuers in 2026, is to route the property claim through MiFID II as a security token, anchor the issuance in a jurisdiction with a working DLT statute, and limit MiCA to the payment and stablecoin layer of the deal. That is not a workaround. It is the structure the regulation was built to support. Issuers preparing this stack can review the jurisdiction configuration options and white-label compliance modules at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo