Tokenized Properties: Managing Rental Income, Capital Events, and Vacancy On-Chain

Post-issuance operations make or break tokenized properties. Here is how rental distributions, capital events, and vacancy gaps must be configured before launch.

A $12 million tokenized multifamily property in Atlanta launched last spring with 340 investors holding fractional tokens. Everything worked at issuance — onboarding, the cap table, the first distribution on the 5th of the month. Six months later, the anchor tenant's lease was not renewed, vacancy climbed to 18%, and the smart contract was still scheduled to push rental distributions on the 5th. No reserve trigger. No quorum rule for an emergency capex vote on the HVAC retrofit the new leasing strategy required.

That gap — between a clean issuance and the operational machinery needed for month 7 — is where most tokenized properties quietly fail. The issuance event gets the headlines. The post-issuance mechanics determine whether the deal still has a functioning investor base in year three.

What Tokenized Properties Actually Encode On-Chain

A token is a container for rights, and those rights have to be operationalized after the deal closes. Chainlink defines tokenized real estate as a property or its cash flows represented as a blockchain token to increase liquidity and enable digital ownership. The phrase "or its cash flows" is the operational hinge — the token can encode an equity claim, a debt claim, a revenue share, or some hybrid of the three.

Each token represents a defined slice of value or ownership based on how the deal is structured. That definition is doing heavy lifting. A token holder in a stabilized residential deal expects a monthly distribution from net rent. A token holder in a value-add asset expects no distribution for 18 months, then a refinance event. A token holder in an anchor-tenant commercial property expects quarterly distributions tied to a CAM reconciliation cycle.

The smart contract must reflect that legal claim. So must the distribution waterfall, the governance module, and the reserve account logic. None of this happens automatically because the token was minted. The operative classification is whether the post-issuance machinery — distribution cadence, governance triggers, reserve refill rules — is configured before the first investor wires funds.

Market Scale and Why Post-Issuance Mechanics Matter Now

The deal volume coming on-chain over the next decade makes the operational gap a sector-wide risk, not a one-off concern. In Chainlink's market framing, the global real-estate market was valued at roughly $29 trillion in 2021, while Savills estimates the total value of all global real estate at around $379 trillion. Those numbers set the addressable base.

The tokenized share is what concentrates the operational stakes. Forecasts from BCG and ADDX put tokenized real-world assets near $16 trillion by 2030, while Deloitte projects tokenized real estate growing from under $300 billion today to about $4 trillion by 2035. Both are projections with methodology caveats — Deloitte's number depends on regulatory clarity in three major jurisdictions, and the $16 trillion figure aggregates several research-house assumptions on adoption velocity.

The scale-up shifts the operational risk from cottage-industry to systemic. KPMG, cited in Chainlink's research, notes that tokenization is well-suited to owners of a single asset or small portfolio because of reductions in offering time and cost. That demographic — single-asset sponsors, mid-market developers — is the segment least likely to have a structured fund administration team. The result is that a growing share of tokenized deals will be operated by sponsors who built their model around the issuance, not the 10-year hold.

Rental Income Distribution Logic Across Three Property Types

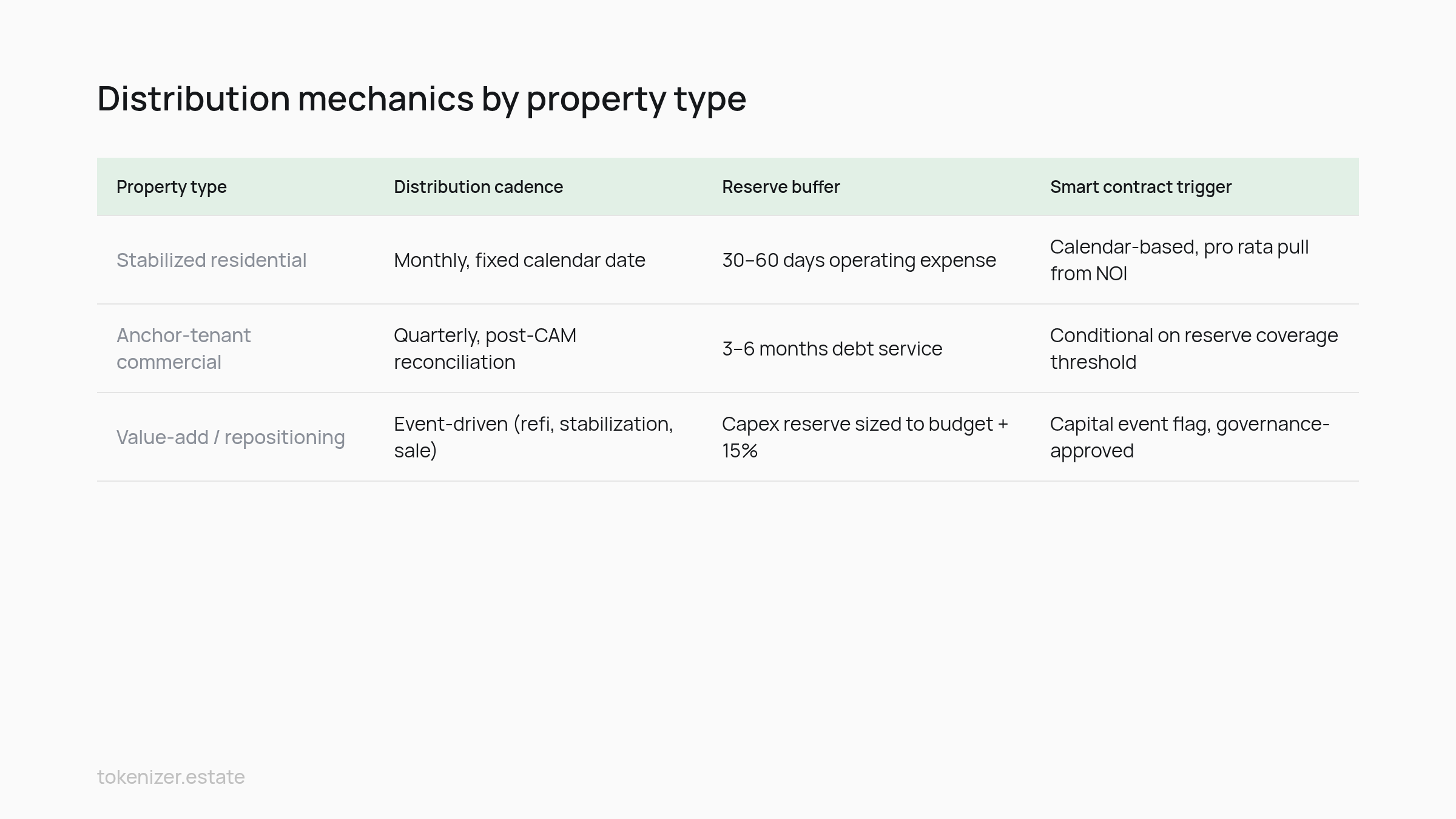

Distribution scheduling is where the legal documents, the smart contract, and the operating reality first collide. The three property archetypes — stabilized residential, anchor-tenant commercial, and value-add — each demand a different cadence, a different reserve buffer, and different smart-contract triggers. Treating them as one category is the most common configuration error.

Stabilized residential: monthly cadence, thin buffer

Stabilized residential assets generate predictable monthly rent rolls, which makes monthly distribution the default cadence for this class. The smart contract typically pulls net operating income, deducts the reserve top-up, and distributes the remainder pro rata on a fixed calendar date. A 30 to 60 day operating reserve is normal because vacancy in a 100-unit multifamily is statistically smoothed across the portfolio — a single move-out does not break the distribution.

Anchor-tenant commercial: quarterly cadence, deeper buffer

Commercial assets with one or two anchor tenants concentrate cash flow risk in a small number of leases. A quarterly distribution cycle aligns with how CAM reconciliations actually settle, and the reserve buffer needs to hold three to six months of debt service because a single anchor non-renewal can take the property to zero distributable cash. The smart contract logic should include a conditional gate: distribute only if reserve coverage exceeds the policy threshold after the payout.

Value-add: event-driven, no scheduled distribution

Value-add assets in lease-up or repositioning do not generate distributable cash for 12 to 24 months. The contractual expectation, set in offering documents, is event-driven: payouts triggered by stabilization, refinance, or partial sale. Token holders need to see this scheduling encoded explicitly in the offering documents, not assumed.

Property type | Distribution cadence | Reserve buffer | Smart contract trigger |

|---|---|---|---|

Stabilized residential | Monthly, fixed calendar date | 30–60 days operating expense | Calendar-based, pro rata pull from NOI |

Anchor-tenant commercial | Quarterly, post-CAM reconciliation | 3–6 months debt service | Conditional on reserve coverage threshold |

Value-add / repositioning | Event-driven (refi, stabilization, sale) | Capex reserve sized to budget + 15% | Capital event flag, governance-approved |

The governing pattern is simple: the contract should never push a distribution that violates the reserve policy. That single rule eliminates a class of failure modes where a calendar-driven payout depletes the buffer that the next quarter's debt service depends on.

Capital Events: Governance Procedures for Refinancing and Capex Calls

A $50 million multi-jurisdiction portfolio — three assets in the EU, two in the United States, one in Singapore — needs to refinance the senior loan in month 28. The sponsor wants to pull $4 million in equity proceeds to fund a capex program on the largest asset. Three things have to happen in sequence: a token holder vote with a verifiable quorum, a legal opinion on jurisdictional consent, and a smart-contract execution of the new debt schedule. Most platforms do not configure this sequence by default.

Why the token standard matters here

ERC-3643 is one of the token standards on Ethereum for tokenizing real-world assets, and as the ERC-3643 specification defines, it incorporates legal mechanisms governing the tokenization of managed assets. That second property — embedded legal mechanisms — is what makes capital-event governance enforceable. Chainalysis describes the standard as one of the few that natively supports the identity and permissioning layer needed for a regulated governance vote.

Without that layer, a quorum vote is a JSON file. With it, the vote is enforceable against the on-chain registry of permissioned holders. The structural implication is that the choice of token standard is itself a governance decision, not only a technical one.

Quorum, consent, and the legal trigger

Governance procedures for a capital event need three configurable thresholds. First, the quorum — what percentage of tokens must vote for the result to be valid. Second, the approval threshold — simple majority for refinancing, supermajority for partial sales or capex calls that dilute. Third, the consent override — jurisdictions where local law requires unanimous consent for an asset disposition regardless of token vote results.

Recent analysis from Pillsbury Law on tokenization developments in New Jersey and Dubai shows that jurisdictional consent rules vary enough that a one-size governance module will fail in at least one of any cross-border deal's jurisdictions. The platform must allow per-asset governance configuration, not a portfolio-level setting.

Capex calls and the dilution question

Capex calls expose the most contentious governance issue: do non-participating token holders get diluted? The legal documents must answer this before launch. The smart contract logic needs a mint function gated by governance approval and a dilution calculation tied to the call amount divided by the post-money valuation. Sponsors who skip this configuration end up running off-chain capital calls that defeat the purpose of having tokenized the asset.

This is also the natural moment to align with the broader cash-flow and exit mechanics the offering documents commit to.

Vacancy Scenarios and Cash Flow Gap Management

Return to the Atlanta multifamily. Vacancy hits 18% in month 7. The reserve has 45 days of operating expense. The next debt service payment is due in 22 days. The smart contract is scheduled to push the monthly distribution in 9 days. Without a configured override, the contract executes, the reserve drops to 15 days, and the property fails the lender's debt service coverage covenant the following quarter.

The fix is not complicated, but it must be designed in before launch. InnReg's compliance analysis identifies vacancy-driven cash flow gaps as one of the most common operational disclosure failures in tokenized real estate offerings. The offering documents must state explicitly: distributions are subject to a reserve-coverage test, and a failed test results in a zero-distribution month with a notification to token holders.

Three contractual elements have to be in place. A reserve floor policy, written into the operating agreement, that defines the minimum coverage ratio before any distribution is permitted. A zero-distribution notification protocol, with a fixed-format on-chain event that token holders' dashboards can read. And a refill trigger — whether the reserve is replenished from future distributions on a waterfall basis or from a sponsor recourse mechanism. This disclosure discipline is part of what distinguishes institutional-grade tokenized offerings from retail-quality ones.

The smart contract layer needs to handle the zero-distribution month gracefully. Hedera's reference materials on real estate tokenization describe the pattern: the contract emits a "distribution skipped" event with the policy reason, the reserve balance, and the next scheduled test date. Token holders see a clean explanation, not a silent failure. Cap table software pulls the event, the investor dashboard reflects the status, and the legal record matches the on-chain record.

The binding limit on this is that vacancy can stack — a 45-day vacancy in month 7 followed by a 60-day re-lease cycle creates a four-month gap before stable rent returns. Reserve sizing has to be matched to plausible vacancy duration for the specific property type and submarket, not to a generic 30-day rule of thumb. For a Class B office in a tertiary market, a six-month reserve floor is closer to defensible than 60 days. Offerings that misize the buffer end up either calling capital from investors mid-hold — which is reputationally costly — or breaching lender covenants, which is financially costly.

Platform Configuration Checklist Before a Tokenized Real Estate Deal Launches

A pre-launch checklist translates the operational thesis into specific platform settings and document clauses. Distribution cadence: configured per asset, not per portfolio, with the calendar date, the reserve-coverage test, and the calculation method documented in the offering memorandum. Per-asset configurability is a baseline requirement for institutional issuers.

Governance thresholds: quorum, approval threshold, and jurisdictional consent overrides set per asset and per event type. A refinancing vote and a capex call do not share the same threshold. The platform must enforce this. Per-event governance should be a standard input, not a custom build.

Reserve logic: floor policy, refill rules, and the on-chain event format for a zero-distribution month, all defined before the first token is minted. Jurisdictional documentation: KYC/AML rules per investor jurisdiction, transfer restrictions configured against the holder registry, and offering documents reviewed in each jurisdiction the asset or investors sit in. Per-jurisdiction transfer logic is non-negotiable for any deal touching more than one regulatory regime.

Cap table integration, investor reporting, and tax-form generation also belong in the pre-launch list. These belong alongside compliance setup in the sequence, because retroactively bolting them on after issuance is operationally expensive. Sponsors with an existing portfolio looking to apply this discipline at scale can reference the portfolio tokenization checklist for the broader operational sequencing.

Successful tokenized property operations depend less on the issuance event and more on how rental distribution schedules, capital event governance, and vacancy reserve logic are encoded into smart contracts and legal documentation before launch. The sponsors whose deals are still functioning cleanly in year three are the ones who treated issuance as the easy part and operations as the part that required deliberate configuration.

Operators preparing a tokenized property structure can review the per-asset configuration model and governance templates at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo