Tokenized Real Estate: How Ownership Rights, Cash Flow Distribution, and Exit Mechanics Actually Work

Beyond the glossary definitions, tokenized real estate involves SPV chains, on-chain distribution logic, and encoded exit clauses that fund managers need to understand before structuring a deal.

A $12M multifamily property gets tokenized across 240 investor wallets spread between Switzerland, Singapore, and the UAE. Six months later, tenants still pay rent in USD to the property manager's bank account. But every 30 days, USDC lands in 240 wallets — pro-rata, after withholding, with the on-chain reconciliation matching the off-chain ledger to the cent. Then one investor in Geneva wants out. The tokenized real estate sitting in their wallet is suddenly a problem: who buys it, at what price, and what happens to their claim on the SPV?

That is where most explainers stop. The mechanics of ownership claims, distribution rails, and exit clauses are the operational core of property tokenization — and the gap between a working setup and a stuck one. This article walks through that gap, section by section, for fund managers and developers evaluating whether tokenization fits an existing portfolio.

What Tokenized Real Estate Ownership Actually Represents

A property token is not a deed. It is a claim on a legal entity that holds the deed. The token lives on a blockchain; the title lives in a land registry. The bridge between them is an SPV — usually a Special Purpose Vehicle (SPV) structured as an LLC or equivalent — which owns the property and issues tokens against its equity, debt, or income rights.

This distinction matters because every operational question downstream — rent flow, voting rights, exit redemption — runs through the SPV, not through the property itself. Innreg's analysis of tokenized real estate frames it directly: tokens convert real-world property rights into digital instruments that can represent ownership, income rights, equity in a legal entity, or debt secured against the asset. The token does not hold the property. The entity does.

The Pension Real Estate Association describes the same architecture from the legal-document side. Token issuance documents can be drafted so that each token represents an ownership interest in the underlying real property, equity in the entity that owns the property, or a debt claim secured by the asset. The choice changes everything that follows — tax treatment, investor disclosures, transfer restrictions, and what happens at exit.

The operative classification here is the legal interest the token encodes. An equity token in the SPV gives the holder a residual claim on cash flow and capital events. A debt token gives a fixed claim with priority. An NFT representing whole-property ownership puts the holder directly on title through a single-purpose entity. Each path requires different legal drafting, different tax filings, and different compliance gates on transfer.

What most issuers skip in the early-design phase is that the token's smart contract is downstream of the SPV's operating agreement. If the operating agreement does not authorize fractional membership interests, the smart contract cannot create them. The legal entity is the source of truth. The chain is the settlement layer.

SPV Ownership Chains and Token Class Design

The structural choice between fungible tokens and NFTs maps directly onto how the underlying asset is being divided. Chainlink's framing is useful here: NFTs work when a property — or a portfolio — is treated as a single indivisible unit (one or more properties, one token). Fungible tokens work when a whole asset is being split into interchangeable parts, each representing pro-rata economic exposure.

The choice is not aesthetic. It drives the SPV's cap table, the secondary-market mechanics, and the way distributions are calculated.

SPV-to-Token Architecture

The standard chain looks like this: a property is held by an SPV. The SPV's equity or membership interests are issued as tokens to investor wallets. Each wallet's token balance corresponds to a pro-rata claim on the SPV's net cash flow and residual value. The blockchain records ownership transfers; the SPV's registry mirrors them; the trustee or administrator reconciles the two.

The underlying ledger logic is straightforward: a blockchain records transactions across a decentralized network of computers, where each transaction is verified, recorded in a block, and broadcast across the network. For property tokens, every transfer becomes an immutable ownership record — but only at the token layer. The land registry still requires off-chain updates when the SPV itself changes hands.

Fungible vs NFT Structures

Dimension | Fungible Token (ERC-20 / ERC-1400) | NFT (ERC-721) |

|---|---|---|

Use case | Fractional equity in single asset or pool | Whole-asset claim, single owner per token |

Investor count | Hundreds to thousands | One per property, or one per portfolio |

Cash flow logic | Pro-rata by token balance | Full cash flow to token holder |

Secondary trading | Order-book or AMM-style venues | Bilateral or auction-based transfer |

Compliance encoding | Whitelist + transfer rules at contract level | KYC tied to single wallet |

Typical SPV form | Multi-member LLC or fund vehicle | Single-member LLC or trust |

Most institutional issuers default to fungible standards because they support transfer restrictions natively — the contract can block a transfer to a non-whitelisted wallet, freeze tokens under court order, or force-redeem under SPV dissolution. NFT-based whole-asset structures are simpler legally but harder to fractionalize later without restructuring the SPV itself.

The token class also dictates how new investors are admitted. Fungible-token cap tables can accept hundreds of holders without amending the SPV's operating agreement each time. NFT structures usually require the SPV to be sold or assigned, which is a heavier legal event. For developers planning to tokenize an existing portfolio, fungible token classes covering pooled equity are the default starting point.

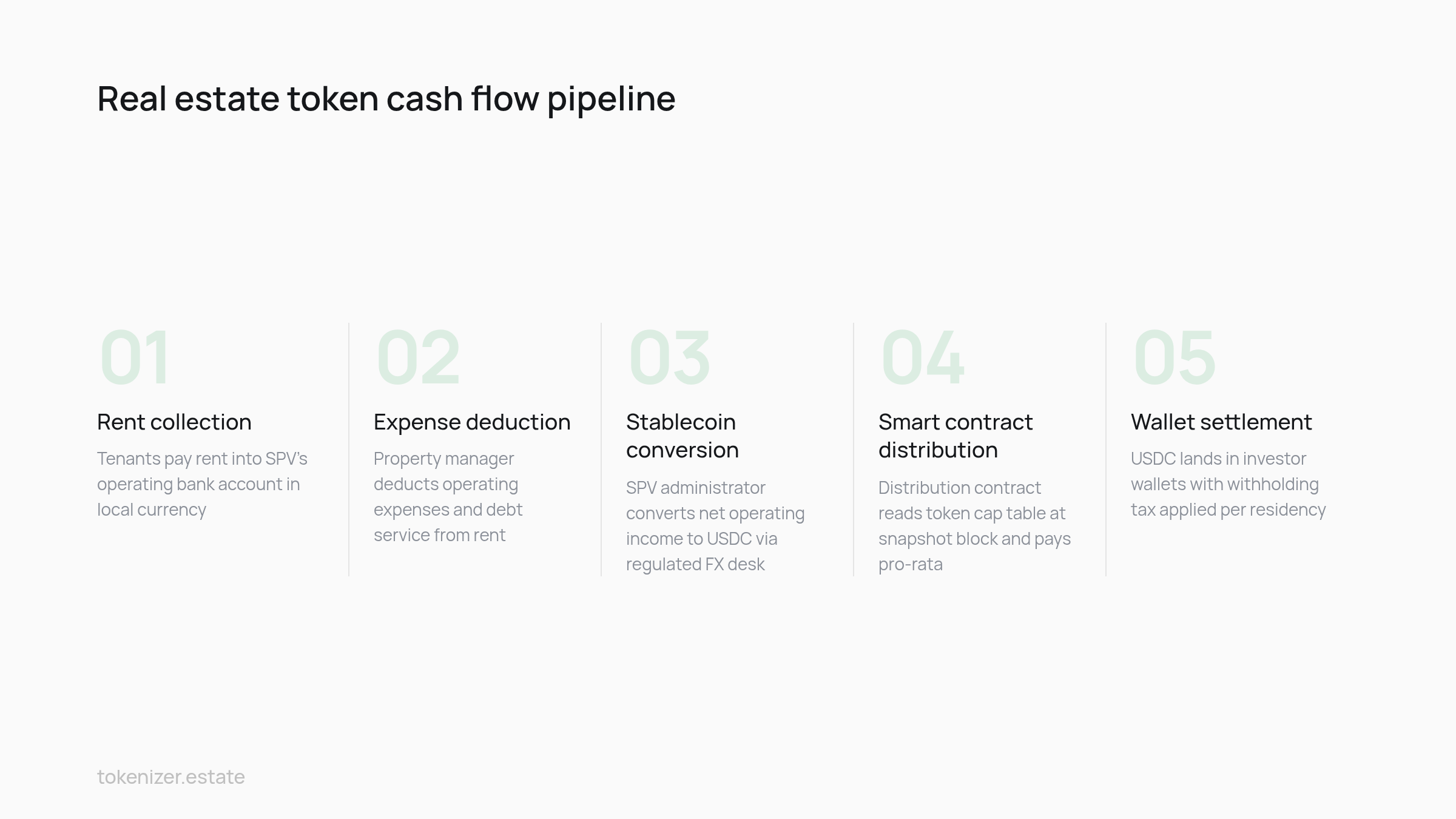

How Real Estate Token Cash Flow Reaches the Wallet

Tenant rent does not flow through a smart contract. It flows through a bank account. The smart contract sits at the end of the pipeline, distributing what the SPV has already collected, converted, and net of expenses. Understanding this off-chain-to-on-chain handoff is where most token-holder confusion lives.

The Distribution Pipeline

Take the $12M multifamily example. Tenants pay rent into the SPV's operating bank account in local currency. The property manager deducts operating expenses — utilities, repairs, insurance, management fees, debt service — and transfers net operating income to a distribution account on a monthly or quarterly cadence.

From there, the SPV's administrator converts the net amount into a stablecoin (typically USDC) through a regulated FX desk or treasury partner. The stablecoin is sent to a distribution smart contract, which reads the token cap table at a snapshot block and pays out pro-rata to every wallet holding tokens at that snapshot.

The mechanics save cost at the distribution layer, but the savings sit downstream of the bigger settlement gap. AWS's overview of tokenization cites a Consumer Federation of America study noting that intermediary costs in traditional home sales — agents, lenders, title, insurers — accumulate into a meaningful drag on transaction efficiency. Tokenized distributions do not remove those intermediaries from the sale; they remove them from the recurring payment cycle.

Pro-Rata Math and Withholding

The pro-rata calculation is straightforward in principle: if an investor holds 0.5% of the SPV's tokens at the snapshot block, they receive 0.5% of the distributable amount. In practice, withholding tax adds a layer. If the SPV is in Luxembourg and the investor is a US tax resident, the SPV may need to withhold at a treaty rate before sending USDC to that wallet.

This is where smart contracts diverge from naive equal-payout logic. Production-grade distribution contracts read a per-wallet tax-residency tag set during KYC, apply the correct withholding rate, and pay the net amount on-chain. The withheld portion sits in a separate SPV account for tax remittance.

Reconciliation

Every distribution generates two records: the on-chain transfer event and the off-chain accounting entry in the SPV's books. The administrator reconciles them monthly. If a wallet is unreachable or a transfer fails (compliance freeze, sanctioned address), the amount is held back and recorded as a payable to that holder.

The Chainlink Education Hub notes that real-estate transactions take weeks to close — and that latency carries into the tokenized layer at the SPV setup and exit stages, even when the distribution cadence itself is monthly or quarterly. The chain compresses settlement, not the underlying property workflow.

Property Token Exit Mechanics: Secondary Trading vs Capital Events

Two exit paths exist for a token holder, and the operational difference between them is total. One is a peer-to-peer transfer on a secondary venue while the SPV continues to operate. The other is a capital event — sale or refinance of the underlying property — that dissolves or recapitalizes the SPV and redeems all token holders pro-rata. Both must be encoded in the smart contract before issuance, because retrofitting exit logic after token distribution is legally messy.

Secondary Trading: Wallet-to-Wallet Transfer

An investor wanting to exit before the SPV's life ends sells their tokens to another whitelisted investor on a compliant secondary venue. The price is set by the venue (order book, AMM, or RFQ), the seller's wallet sends tokens, the buyer's wallet sends payment, and the smart contract validates that the buyer is on the SPV's whitelist before allowing the transfer.

The token's NAV is recalculated periodically against appraisal updates. Secondary trades typically clear at a discount or premium to NAV based on liquidity, holding period, and market sentiment. The SPV does not need to do anything — title does not move, only the token does. This is the lightest-touch exit and the one tokenization most directly enables in a market historically valued at around $29 trillion globally as of 2021, where bilateral fractional sales were previously impractical.

Capital Events: SPV-Level Redemption

The second path is the underlying property being sold or refinanced. The SPV receives the sale proceeds, settles its debts, and distributes the residual to token holders pro-rata. The smart contract's redemption function is triggered by the SPV's authorized signer, the cap table is snapshotted at the redemption block, and USDC is sent to every wallet in proportion to their holding.

After redemption, the tokens are burned or marked as non-transferable. The SPV is wound down or repurposed. This is the equivalent of a fund's terminal distribution — clean, final, and irreversible.

The trickier case is a partial capital event: refinancing pulls equity out of the property without selling it. The SPV distributes the refinance proceeds as a return of capital, but the tokens remain outstanding against the now-leveraged property. Smart-contract logic must distinguish between income distributions, return-of-capital events, and full redemptions for tax-reporting purposes.

Encoding the Exit Clause

Production-grade contracts include exit clauses covering forced redemption (SPV dissolution by majority vote), mandatory tender (sponsor buys out minority below a threshold), and drag-along rights (if 75% vote to sell, all token holders must accept the sale). These are not blockchain-native concepts. They come from the SPV's operating agreement and must be mirrored exactly in the contract logic.

The binding limit on exit flexibility is the operating agreement. If it does not authorize a buyback, the contract cannot execute one. Fund managers designing the structure should write the exit waterfall in legal prose first, then encode it — not the other way around. The same logic governs how investors evaluate secondary-market liquidity before subscribing.

Compliance Layers: MiCA, Transfer Restrictions, and Investor Eligibility

Jurisdictional compliance is encoded as code-enforced rules at the smart-contract level. A token cannot transfer to a wallet that has not passed KYC. It cannot transfer to a wallet flagged as resident in a restricted jurisdiction. It cannot transfer during a lockup period. Every rule that lives in the offering memorandum has a parallel rule in the contract.

In the EU, the Markets in Crypto-Assets Regulation (MiCA) framework distinguishes asset-referenced tokens, e-money tokens, and other crypto-assets — and real estate tokens classified as financial instruments fall under MiFID II rather than MiCA itself. The classification determines which prospectus rules apply, which disclosure regime governs distributions, and which authority supervises secondary trading. For issuers preparing structures during the MiCA phase-in period, the operational implication is that real estate equity tokens generally route through national securities law rather than MiCA's crypto-asset regime, with MiCA reserved for utility tokens, stablecoin payment rails, and asset-referenced products used in the wider structure.

In the US, Regulation D Rule 506(c) allows issuance to accredited investors with verification, while Regulation S handles offshore distribution. The smart contract enforces both by reading per-wallet tags: accreditation status, residency, and lockup expiry. A transfer attempt that violates any tag reverts. The contract becomes the first compliance gate, not the last.

Whitelist logic typically sits in a separate registry contract that the token contract reads on every transfer. This separation lets the administrator update investor eligibility — adding new approved wallets, freezing sanctioned ones — without touching the token contract itself. Practical guidance on how this maps to issuer onboarding sits in the KYC/AML obligations for tokenized securities.

Market Sizing and Where Tokenized Real Estate Adoption Sits in 2026

The market projections cluster in a wide range, and the methodology behind each number matters more than the headline. A Citibank forecast from March 2023 projected the total addressable market for tokenized real estate at $1.5 trillion by 2030 — a top-down estimate based on percentage capture of global property AUM, not on observed on-chain volume.

Bottom-up estimates land lower. InsightAce Analytic values the real estate tokenization market at USD 3.73 Bn in 2025, projecting growth to USD 23.99 Bn by 2035 at a 21.0% CAGR across the 2026-2035 forecast period. That figure measures actual tokenized AUM and platform revenue, not theoretical addressable opportunity — which explains the order-of-magnitude gap from top-down forecasts.

InsightAce's segmentation splits the market into residential, commercial, and industrial categories, with North America leading regional adoption. The concentration reflects where SPV structuring is most mature, where accredited-investor pools are deepest, and where secondary venues have been operating longest. European adoption lags but is accelerating as MiCA-adjacent regimes clarify the path for real-estate-backed instruments.

The structural implication for fund managers is that 2026 sits in the early-deployment phase — large enough for operational benchmarks to exist, small enough that the issuer designs the standard for their own structure rather than inheriting one.

Tokenization overlays a programmable settlement layer on top of the SPV-and-title stack real estate has always used. It does not replace deeds, operating agreements, or property managers. The token is the cap-table entry and the distribution channel — the legal architecture underneath stays familiar to anyone who has run a fund.

The managers who deploy this productively are the ones who understand the seams: where off-chain title meets on-chain transfer, where USD rent becomes USDC distribution, where the operating agreement's exit clause becomes the smart contract's redemption function. Fund managers and developers ready to map these seams against a specific portfolio can review the jurisdiction and structuring configuration options at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo