Security Token Offering vs Traditional Private Placement: A Compliance and Cost Comparison for Real Estate Developers

Real estate developers raising capital face a pivotal structural choice. We compare STOs and Regulation D placements on cost, compliance, and reach.

A developer holds a $12M mixed-use asset in Miami and a $50M portfolio spread across Lisbon, Dubai, and Singapore. The same question lands on the desk twice: run a Regulation D private placement the firm has closed a dozen times, or issue a security token offering. The math diverges sharply after month four.

Setup invoices, investor reach, transfer-agent duties, and secondary liquidity all behave differently once the deal crosses jurisdictions or pushes past $25M. The comparison below traces those divergence points using both scenarios as fixed reference deals.

Two Reference Deals: $12M Asset vs $50M Portfolio

The Miami asset is straightforward. One building, one US SPV, one accredited investor list the developer has already mailed three times this decade. A Reg D 506(c) close in eight weeks is a known quantity, and the secondary market for the LP interests is whatever the sponsor decides to honor at year five.

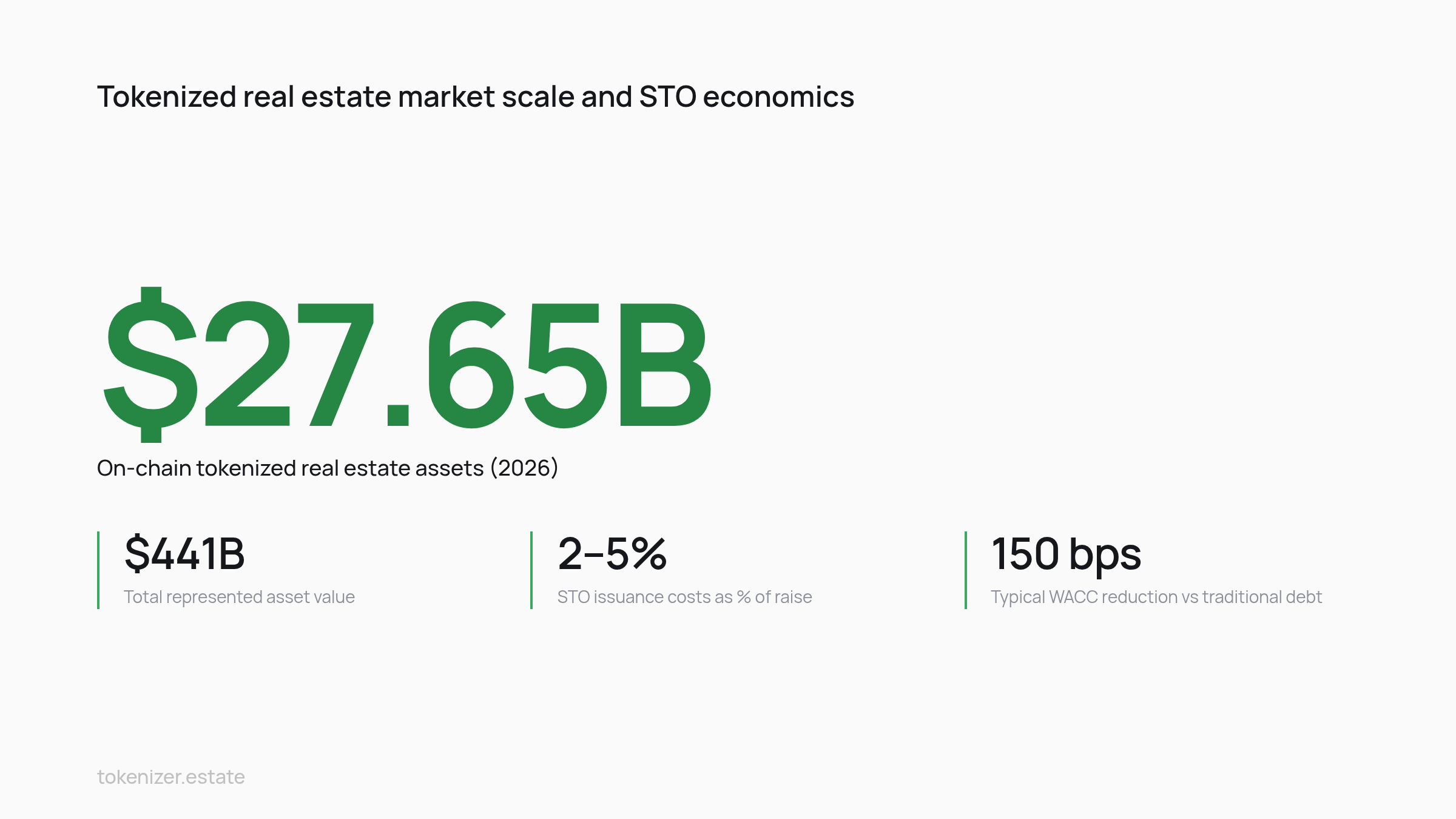

The $50M portfolio is not the same animal. Three properties, three regulators, and an investor base the developer would need to assemble from scratch if the goal is to reach beyond a domestic accredited list. The tokenized real estate market is growing but still small in absolute terms: the real estate tokenization segment was around $3.5 billion in 2024 (Custom Market Insights), within a total tokenized-RWA market that reached $31.9 billion by June 2026 (RWA.xyz). Real estate still trails Treasuries, private credit, and commodities by an order of magnitude.

That depth matters because it changes the distribution question for the $50M deal. Liquidity venues, custodians, and compliant transfer rails for security tokens are no longer experimental. Forward projections vary by methodology: Deloitte projects tokenized real estate could reach roughly $4 trillion by 2035, up from under $300 billion in 2024, a long-horizon estimate that varies widely across reputable researchers.

The Miami deal will not benefit from any of that infrastructure in a way the sponsor cannot already replicate cheaper through a wire transfer and a sub-doc. The Lisbon-Dubai-Singapore portfolio cannot be efficiently closed without it. Holding those two reference points fixed for the remainder of the article lets every cost and friction line be tested against a real scenario instead of an abstraction.

Legal Setup Cost: Security Token Offering vs Private Placement

The cost gap between the two structures is real but smaller than most developers assume, once the platform line item is treated as a one-time amortization across multiple deals rather than charged in full to a single raise.

Private Placement Setup

A US Reg D 506(c) close on a single-asset deal runs a predictable cost stack: a Delaware SPV, a private placement memorandum, a Form D filing, blue-sky notices, and a subscription agreement package. The Gofaizen & Sherle legal model for tokenized property uses the same primary wrapper, a Special Purpose Vehicle (SPV) or equivalent holding structure, so the entity formation cost is broadly comparable across both structures. The divergence is in everything that hangs off the SPV.

STO Setup: Platform, Smart Contracts, and Banking

Issuance technology is where the additional spend concentrates. Industry build-cost estimates put basic MVPs around $15,000, with enterprise platform builds exceeding $300,000 for institutional feature sets. Smart contracts sit inside that range: basic ERC-20 implementations are quoted at $8,000 to $25,000, with advanced features (lockup periods, automated distributions, transfer restrictions) adding to the cost on top.

Hidden expenses, compliance integrations, and ongoing maintenance can push total budgets meaningfully above the headline platform figure. The structural implication is that the platform cost is only defensible across a portfolio or a multi-deal pipeline. Amortized across the portfolio's three properties, a mid-range platform build lands at a few basis points of raise. Charged in full to the Miami asset, the same number becomes a much larger drag and a hard sell against a private placement that needs none of it.

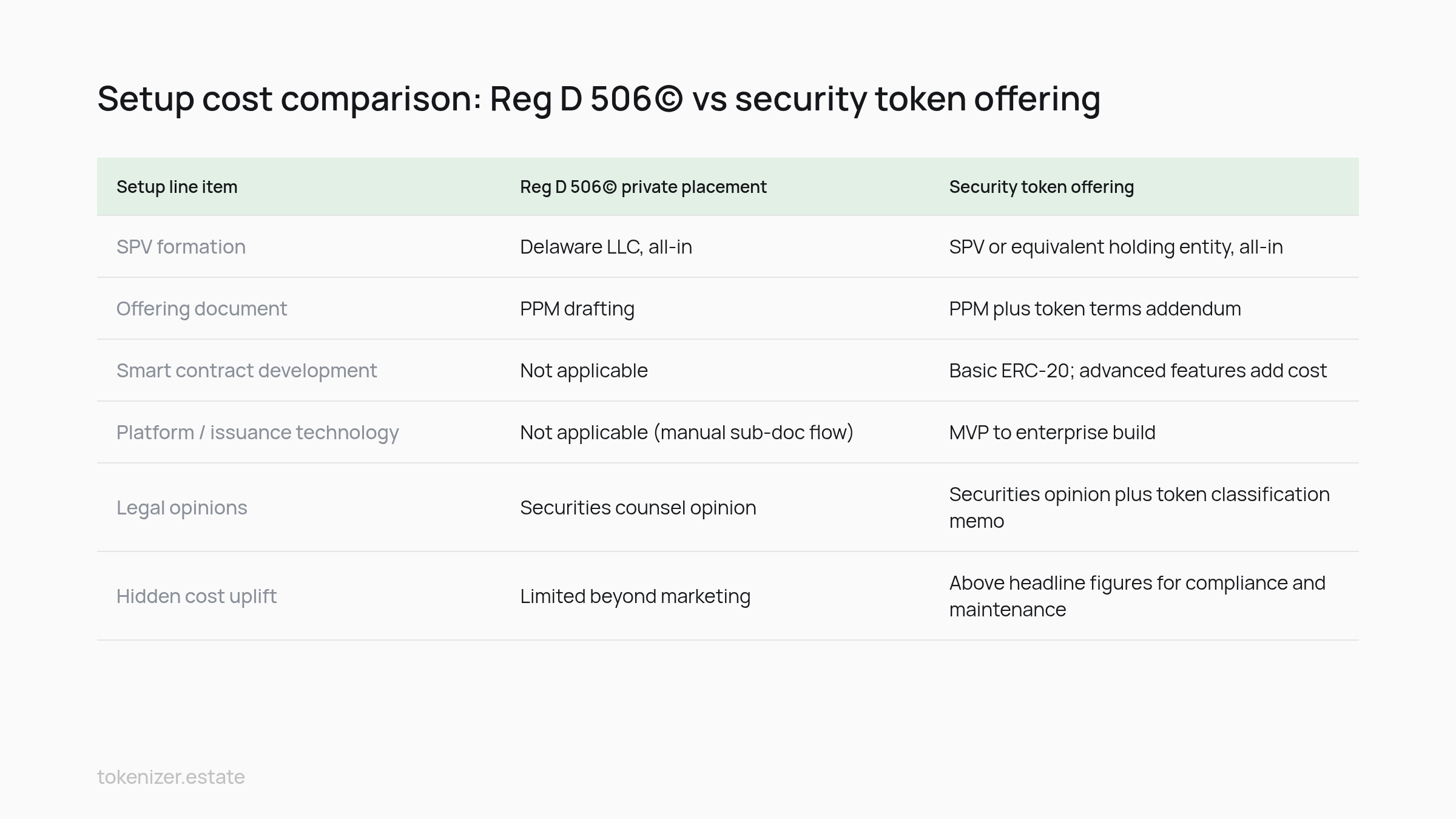

Side-by-Side Setup Cost Comparison

Setup line item | Reg D 506(c) private placement | Security token offering |

|---|---|---|

SPV formation | Delaware LLC, all-in | SPV or equivalent holding entity, all-in |

Offering document | PPM drafting | PPM plus token terms addendum |

Smart contract development | Not applicable | Basic ERC-20; advanced features add cost |

Platform / issuance technology | Not applicable (manual sub-doc flow) | MVP to enterprise build |

Legal opinions | Securities counsel opinion | Securities opinion plus token classification memo |

Hidden cost uplift | Limited beyond marketing | Above headline figures for compliance and maintenance |

For the Miami asset, the all-in setup differential favors the private placement depending on platform choice. For the Lisbon-Dubai-Singapore portfolio, the differential narrows once the same platform is reused across three closes and three jurisdictions; the binding constraint there is whether legal opinions need to be drafted in three regulatory regimes regardless of structure. Reading frameworks for both wrappers in securities counsel guidance confirms the SPV substrate is the constant.

Investor Onboarding Friction and KYC Reach

The Miami deal closes through a Google Drive folder. The developer's existing accredited investor list receives a PPM, returns signed subscription documents, wires funds, and is added to a manual cap table maintained in a spreadsheet by the sponsor's controller. Total touch time per investor: roughly 90 minutes of sponsor labor across the close.

That model works at 15 investors. It does not scale to 400. The $50M portfolio, sold to a broader investor base spread across three regions, runs into a wall the moment the subscription queue exceeds what one paralegal can process in a week. The operative classification here is whether the offering is built for a relationship-driven domestic close or for a cross-border distribution that touches multiple jurisdictions of investor residency.

Automated identity verification was built for the second case. Signzy reports that its STO compliance workflow verifies identities across 180+ countries and screens against 1,000+ sanctions lists, replacing the manual due-diligence file each Reg D placement currently builds by hand. The pattern in private-markets onboarding is well documented: manual processes consume sponsor and investor time in roughly equal measure, and the friction compounds as deal count rises across a portfolio sponsor's pipeline.

The token standard governing transfer eligibility carries the compliance state forward after onboarding. The ERC-3643 standard, now the de facto standard for permissioned security tokens, embeds identity claims directly into the token, so a wallet that has not passed the issuer's KYC cannot receive a transfer. That property is what makes a true secondary market possible without recreating the sub-doc process on every resale. A Reg D 506(c) interest, by contrast, requires the sponsor or transfer agent to approve and document each transfer manually, which is why most LP interests do not trade at all in practice.

For the $12M Miami asset, the onboarding friction of a private placement is absorbable. For the $50M cross-jurisdiction portfolio, it is the determinant of whether the deal can be sold at all in the timeline the developer needs.

Ongoing Real Estate STO Compliance Obligations

Closing is not the end of compliance work: it is the beginning of a different kind of compliance work. The structural difference between the two wrappers shows up in who maintains the cap table, who files what to which regulator, and how long the operational tail runs after issuance.

Transfer Agent and Cap Table Duties

A Reg D placement typically uses the sponsor's outside counsel or an administrator to maintain the cap table, log transfers (rare), and issue K-1s annually. An STO requires a registered transfer agent in the US, or the jurisdictional equivalent in Portugal, the UAE, or Singapore, to maintain the on-chain register as the authoritative record of ownership. The transfer agent function is more codified for tokenized securities precisely because the secondary market is a real possibility rather than a theoretical one. ComplyCube's guidance on STO compliance frames the transfer-agent obligation as a continuing duty, not a one-time setup task.

Jurisdictional Reporting and the Banking Bottleneck

The Lisbon-Dubai-Singapore portfolio carries three sets of ongoing filings regardless of wrapper choice. Where the wrappers diverge is in the time-to-operational status. Gofaizen & Sherle reports project timelines of 4 to 8 months for tokenized property issuances, with banking onboarding as the main bottleneck. That timeline applies to opening operating accounts capable of receiving fiat proceeds from token sales and remitting distributions back to token holders.

The bottleneck does not disappear in a private placement, but it is shorter because the universe of banks willing to host a domestic SPV with no tokenized component is wider. For the Miami asset, banking is a two-week problem. For a cross-jurisdiction tokenized issuance, it is a six-month problem, and the operational tail begins before the first investor wires a dollar.

Why Jurisdiction Choice Compresses the Timeline

The regulatory environment for digital securities has matured fastest in jurisdictions with established frameworks. North America holds the largest share of the tokenized-assets market, around 38.8% (Market.us), supported by the SEC's evolving digital-securities posture. The practical effect for the Miami asset is that even if the developer chose to tokenize it, the supervisory infrastructure is in place. The same is true in increasingly granular form across selected European and Gulf venues, see analysis of the MiCA framework for what the Lisbon leg of the portfolio inherits.

Ongoing obligations are heavier under the STO wrapper, but they are also more automated. Annual investor communications, distribution waterfalls, and transfer approvals run through the same rail that handled the initial issuance. In a private placement, each of those touchpoints is a fresh manual workflow.

Distribution Reach and Cost of Capital

The economic case for an STO on the $50M portfolio rests on three lines: cost of capital, issuance cost as a percentage of raise, and the prospective secondary-market liquidity that could compress both.

Industry cost-of-capital analyses point to a meaningful reduction in weighted average cost of capital compared to traditional bank debt. The figure that matters most for the $50M portfolio is the WACC delta, because it compounds across the holding period. On a five-year hold, a hypothetical 150 basis point WACC reduction translates into meaningful retained equity value before any premium for distribution reach.

Industry estimates put STO issuance costs at 2% to 5% of raise (covering technology and legal), with near-instant atomic settlement. For the Miami asset, an issuance cost in that range is hard to justify against a private placement setup. For the $50M portfolio, the same percentage is defensible against a private placement that would still cost substantially less in cross-jurisdictional legal work, and the gap closes further once the WACC saving is netted against it.

The compliance-overhead reduction is the second-order effect that makes the issuance cost defensible. The operational tail of a tokenized issuance is automated; the operational tail of a multi-hundred-investor private placement is not.

Academic work on real estate security token offerings is more cautious: a Journal of Banking & Finance study of 173 US real estate tokens found that tokenization delivers broad fractional ownership and low entry barriers, but that secondary trading remains thin and pricing is partly driven by crypto-market sentiment. The distribution-reach case for STOs currently rests on primary-market access, not on proven secondary liquidity.

For the $50M portfolio, distribution reach is the value proposition. For the Miami asset, the same reach is overcapacity the developer is paying for and does not need.

Decision Matrix: When STO Real Estate Beats Private Placement

The decision turns on three variables: deal size, jurisdiction count, and whether the investor base needs to be assembled or already exists. The matrix below maps those variables back to the two reference deals.

Deal profile | Recommended structure | Why |

|---|---|---|

Sub-$15M single-asset, single jurisdiction, existing accredited list | Reg D 506(c) private placement | Setup cost differential cannot be recovered; the Miami asset fits here. |

Mid-size single-asset, single jurisdiction, expanding investor base | Reg D 506(c) with optional secondary tokenization at year 2–3 | Primary close cheaper as private placement; tokenize later if liquidity becomes the constraint. |

Larger single-asset, two or more jurisdictions of investor residency | Security token offering | Cross-border investor reach and automated transfer eligibility justify issuance cost. |

Multi-asset portfolio across two or more property jurisdictions | Security token offering | Platform cost amortizes across deals; the Lisbon-Dubai-Singapore portfolio fits here. |

Any deal with retail-eligible jurisdiction and lower minimum tickets | Security token offering | Manual sub-doc workflow cannot scale to retail volumes. |

Forward market data reinforces the larger-deal bias. Boston Consulting Group has projected the broader tokenized-asset market could reach roughly $16 trillion by 2030, with some scenarios running to about $18.9 trillion by 2033, figures that should be read as aggregator projections rather than measured outcomes, but that nonetheless signal where infrastructure investment is concentrating. Operational checklists for portfolio-scale issuance are covered in more detail in portfolio tokenization work elsewhere on this site.

STOs reward larger, multi-jurisdiction deals with broader investor reach and lower long-term capital costs. Traditional private placements remain the pragmatic choice for sub-$15M single-asset raises with established accredited investor networks. The Miami asset belongs in a private placement; the Lisbon-Dubai-Singapore portfolio does not.

The mechanical question for a developer holding both kinds of deals is not which structure is better in the abstract: it is which structure matches the distribution requirement and operational shape of each specific raise. Issuers preparing to map their own portfolio against this matrix can review jurisdiction configuration and SPV setup options at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo