How to Tokenize Real Estate: Four Infrastructure Decisions That Determine Deal Success

Most failed real estate tokenization deals trace back to four infrastructure decisions made too late. Here is how to get them right before you pick a platform.

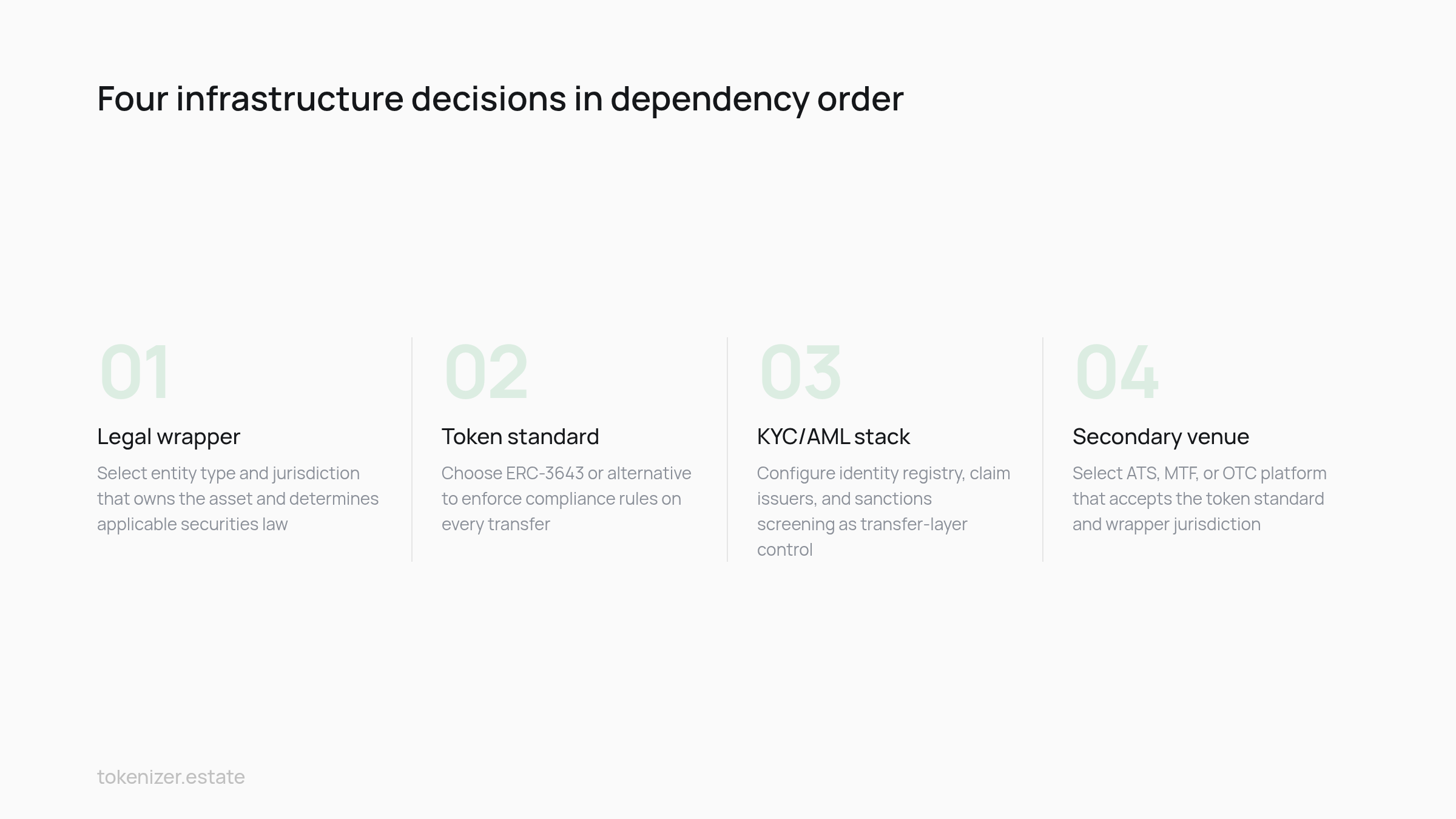

Four infrastructure decisions determine whether a tokenized real estate deal closes cleanly or stalls in legal review: legal wrapper, token standard, KYC/AML stack, and secondary venue. They are not independent choices made in parallel. They sit in a dependency chain, and getting the order wrong forces a rewrite of every earlier choice.

The deals that stall rarely fail on the platform. They fail because these four decisions were treated as procurement line items, resolved late and in the wrong sequence, instead of as one structural design problem settled before the first RFP.

Why Most Attempts to Tokenize Real Estate Stall

Tokenization of real-world assets is now part of how serious portfolios are built, per the 2026 legal guide from Maheshwari & Co. Issuers no longer need to argue the concept. They need to ship deals that clear regulatory review, attract qualified buyers, and trade after issuance.

The deals that stall almost always share a pattern. The issuer treated tokenization as a procurement exercise: pick a platform, sign a contract, push the asset on-chain, rather than a structural design problem. Securities sit inside a market measured in hundreds of trillions of dollars, as the ERC-3643 protocol documentation notes, and that scale exists because every security has a coherent legal, operational, and transfer layer behind it. Skipping any of those layers does not make the deal faster. It moves the cost into legal review and post-issuance disputes.

Decision One: Legal Wrapper Selection and Jurisdiction Fit

The wrapper is the entity that actually owns the building. Tokens represent claims against that entity, never against the bricks. Picking the wrong wrapper does not just create tax friction, it determines whether transfers are legally enforceable at all.

The wrapper choice sets which securities law applies to the token, which regulator supervises the issuer, and which transfer mechanics are recognized on-chain. A Luxembourg SPV holding an EU property through a local subsidiary maps cleanly to MiFID II and clears review quickly when counsel confirms the framework before signing.

Wrapper options by jurisdiction

Wrapper | Jurisdiction | Primary regulator | Best fit |

|---|---|---|---|

SPV (Lux/Ireland) | EU | National securities authority + MiCA for custody | Single-asset or small portfolio, EU-domiciled investors |

Delaware Series LLC | US | SEC (Reg D / Reg S) | US issuers using UCC Article 12 control rules |

SM REIT | India | SEBI | Rent-generating completed assets, retail access |

Cayman / BVI SPV | Offshore | Local + market-of-listing rules | Cross-border investors, no retail distribution |

For Indian assets the choice is now narrower. Following the SEBI amendment regulations of 2024, fractional ownership platforms must register as Small and Medium REITs, and at least 95% of the scheme's assets must be in completed, rent-generating properties. Construction-stage assets do not fit.

The EU complication

EU issuers face a dual-framework reality. MiCA is now fully operational and handles digital asset custody, while tokenized properties typically fall under MiFID II as financial instruments. The classification splits: MiFID II for the security itself, MiCA for custody and crypto-asset service providers. Mapping both before contract signing is what keeps EU review short. A broader picture of the same trade-off is set out in the EU framework analysis.

The US transfer-layer question

For US wrappers, the binding question is whether the state has adopted the 2022 amendments to the Uniform Commercial Code. Over 30 US states have enacted those amendments as of 2026, creating Article 12 and giving a legal definition of "controllable electronic records". Without that, on-chain transfers of investment tokens sit in commercial-law limbo.

The failure mode here is picking an offshore wrapper, such as a BVI SPV, without first checking whether the intended secondary venue accepts tokens issued from that jurisdiction. When it does not, the mismatch can add months to the timeline.

Decision Two: Token Standard Choice and Why ERC-3643 Dominates

The token standard is the rulebook the smart contract enforces on every transfer. Pick a permissionless standard and the issuer is left to bolt compliance on top in off-chain agreements that no validator checks. Pick ERC-3643 and compliance lives inside the contract itself.

What ERC-3643 actually does

ERC-3643 is an Ethereum standard for permissioned tokens: tokens that can only be held and transferred by identities meeting predefined compliance rules such as KYC/AML and investor eligibility. The standard was originally developed as T-REX (Token for Regulated EXchanges) and reached "Final" status as an Ethereum Improvement Proposal in December 2023, approved by the Ethereum community.

It is now formalized as ERC-3643 and governed by the ERC-3643 Association. The protocol is an open-source suite of smart contracts that handles issuance, management, and transfer of permissioned tokens.

Why permissioned transfer logic matters

Every ERC-3643 transfer call checks the recipient against an on-chain identity registry before it executes. If the recipient is not whitelisted, or if the transfer would breach holder caps or volume limits, the contract reverts. The standard has two levels of permissions for security and compliance, with limits on daily token volume and the number of holders. The same lock applies in primary issuance and on every secondary trade, there is no way to "forget" KYC mid-cycle.

This is enforced through a built-in decentralized identity framework, ONCHAINID, which means only users meeting predefined conditions can become token holders, even on permissionless blockchains. The framework also handles claim revocation, when an investor loses qualified status, the registry updates and the contract refuses further inbound transfers.

The alternatives and their cost

ERC-20 with off-chain transfer agent: workable for closed-end vehicles with no secondary trading, but every secondary transfer needs a manual cap-table update. ERC-1400: an earlier security-token standard, partially superseded, interoperable with fewer venues in 2026. Polygon-native or Polymesh-native security tokens: viable, but the issuer locks itself into a single chain ecosystem.

Where a secondary venue only accepts ERC-3643 for retail-eligible tokens, that standard is not optional. A common and costly misstep is deploying a custom ERC-20 with a transfer-agent overlay, then discovering that a qualified buyer's compliance desk rejects it because the eligibility check lives in a human process rather than in the contract. The fix is a rewrite to ERC-3643 and a redeploy, which the correct standard choice at the start would have avoided. The smart-contract layer behind a real estate token is examined in more depth in the smart contracts guide.

Decision Three: KYC/AML Configuration as a Transfer-Layer Control

Most issuers still treat KYC as an onboarding form. The investor fills it in once, gets approved, and the platform moves on. That model breaks the moment tokens trade.

The correct framing, and the one ERC-3643 enforces, is that KYC/AML is a transfer-layer control. Every transfer asks the identity registry: is this recipient still a qualified investor in this jurisdiction, holding under the cap, and not under sanctions screening? If any answer changes, the next transfer fails. That is the structural point most RWA compliance analyses converge on.

The configuration choices an issuer must make before deploying the registry are concrete. Which claim issuers are trusted to attest accreditation? How is residency verified: passport plus utility bill, or a regulated identity provider? How are jurisdiction-specific holder caps encoded (US 99-investor Reg D limit, EU prospectus exemption thresholds)? How are sanctions screening updates propagated to the on-chain registry? Each question maps to a specific module in the compliance stack. Configuring the registry wrong, or treating KYC as a one-time onboarding step, is what freezes a deal when the first secondary buyer applies and a holder cap turns out to be breached on paper. This reconfiguration overlaps tightly with the wrapper decision in Section 2.

Decision Four: Secondary Market Architecture for Tokenized Real Estate

Liquidity is the variable issuers most often promise and least often design for. A tokenized real estate position only trades if a venue exists that accepts the token standard, recognizes the wrapper's jurisdiction, and can settle against the issuer's transfer agent. Choosing that venue last, after wrapper, standard, and KYC are locked, is how deals end up in legal review for a second time.

Venue types and their constraints

Three architectures are available in 2026 for tokenized real estate secondary trading.

Regulated Alternative Trading System (ATS) in the US: operates under SEC and FINRA oversight, accepts Reg D and Reg S tokens, requires the issuer to appoint a registered transfer agent. Liquidity is concentrated but accessible only to US-qualified investors. Multilateral Trading Facility (MTF) in the EU: operates under MiFID II, accepts MiCA-compatible custody arrangements, supports cross-border EU distribution. Bilateral OTC: no order book, trades arranged between known counterparties, viable for institutional blocks, useless for fractionalized retail positions.

The venue choice should be made jointly with the token standard, because some venues only list tokens with on-chain compliance hooks. ERC-3643 clears most regulated venues; bespoke ERC-20 structures do not.

The dependency chain in action

The order holds up under real conditions. A Luxembourg SPV (MiFID II-recognized), an ERC-3643 token (venue-accepted), and a KYC registry supporting EU-wide passporting route cleanly to an EU MTF, because each layer was chosen to fit the next.

Reverse the order and the cost is concrete. An offshore SPV that qualifies for neither a Monetary Authority of Singapore-recognized issuer entity nor a CMS license cannot list on a Singapore venue that requires one. Restructuring into a compliant vehicle after commitments are in place can reprice the deal against the original NAV, a direct cost of leaving the venue decision until after issuance.

Sequencing the Four Decisions Before Platform Selection

The order matters and is not interchangeable. Wrapper first, because it sets the securities law and the regulator. Token standard second, because the standard must be compatible with both the wrapper's jurisdiction and the planned venue. KYC/AML configuration third, because the registry's claim structure depends on which investor categories the wrapper and standard permit. Secondary venue fourth, but designed in parallel from the start, because venue acceptance criteria feed back into the first three decisions.

Before any platform RFP, an issuer should be able to answer in writing: what entity owns the asset and under which law; which token standard the asset will issue and why; which claim issuers will populate the identity registry; which venue or venues will list the token at issuance and at month twelve. Platforms then become an execution choice, not a structural one. The same sequencing order maps cleanly onto the 2026 vendor landscape: platforms differ mainly in which of these four layers they handle for the issuer and which they leave to external counsel.

An issuer who answers the four questions before the RFP has already made the structural decisions; the platform is just execution. An issuer who skips them and treats the platform as the structural choice inherits the rework, redeploying contracts and re-onboarding holders after the fact.

Successful tokenization is decided before token issuance, with the wrapper, the standard, the KYC stack, and the venue acting as one dependent system rather than four procurement decisions. Tokenizer.Estate provides the software layer for this, and can help you think through how the four decisions fit together before you commit to a build.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo