Tokenization for family offices: why the $6 trillion market is paying attention

A family office controls $400 million. 40% is in real estate. All of it is locked. Tokenizing 15% of one property raises $6 million in eight weeks, without selling, without a bank, without losing control. This is the practical guide for family offices evaluating tokenization in 2026.

A family office in Zurich controls $400 million in assets. Roughly 40% sits in real estate: two office buildings in Frankfurt, a logistics park outside Lisbon, a hotel in Montenegro, and a development plot in Dubai. The income is solid. The assets are good. But $160 million is locked. If the family needs $20 million for a new opportunity, they have two options: sell a building (six months, broker fees, capital gains) or go to a bank (60% LTV, personal guarantees, four months of paperwork).

There is a third option now. Tokenize 15% of the logistics park. Raise $6 million from 120 investors across 11 countries in eight weeks. Keep 85% ownership, keep management control, keep the tenants. Use the capital for the new deal.

This is not a pitch. This is what family offices are actually evaluating in 2026. Real estate allocations reached 39% of family office portfolios in 2025, up from 26% two years earlier. Alternatives overall account for 42 to 45% of the average family office portfolio. The capital is concentrated, illiquid, and growing.

Tokenization does not replace any of these assets. It unlocks them.

This article explains why family offices are looking at tokenization in 2026, what problems it solves that traditional structures do not, how a tokenized deal works in practice, and where the risks are. If you run a family office or advise one, this is the practical picture.

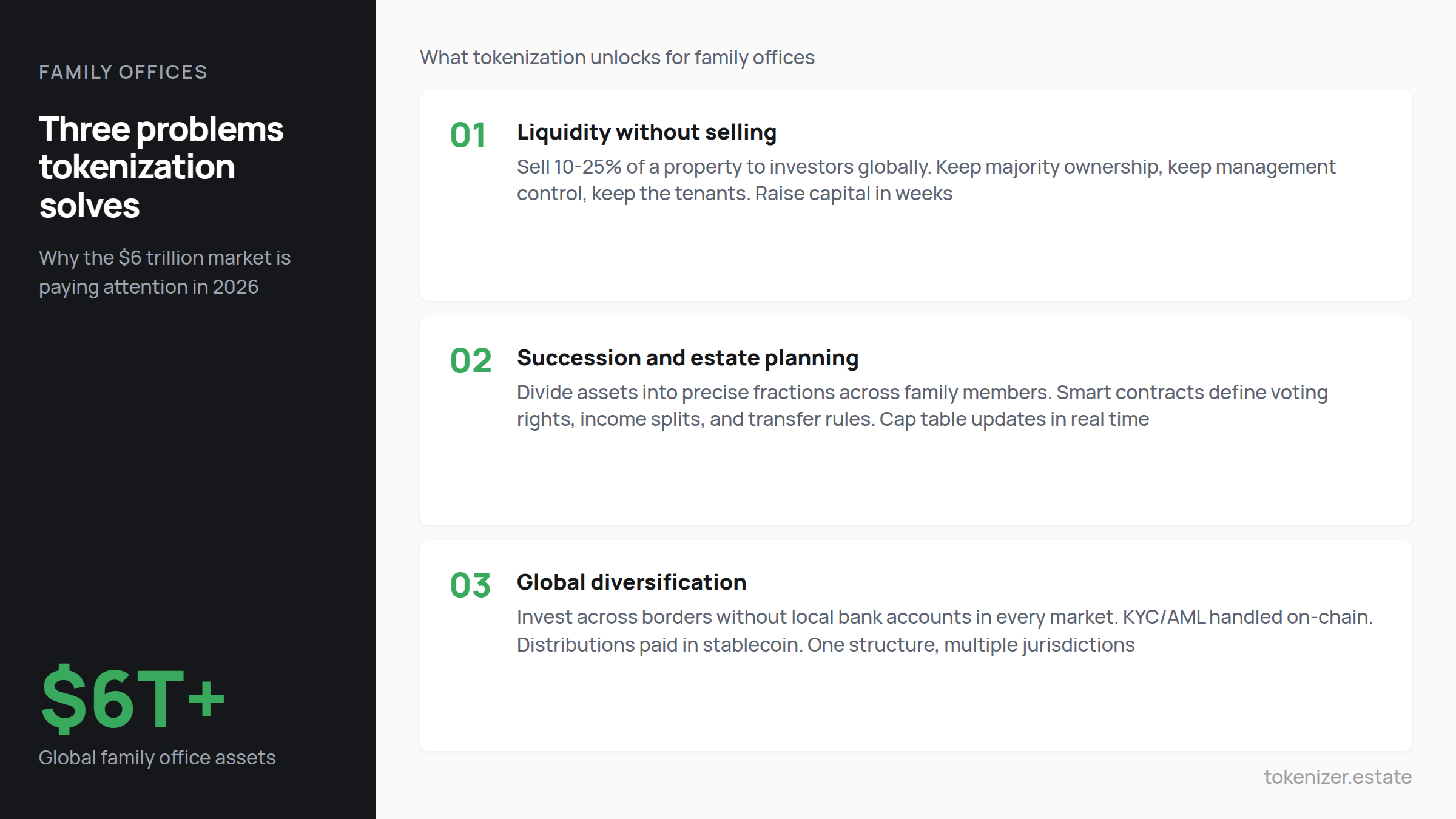

The three problems tokenization solves for family offices

Family offices are different from institutional funds. They do not answer to external LPs. They do not have quarterly reporting pressure from pension boards. They think in decades, not quarters. But they have three structural problems that tokenization addresses directly.

Liquidity without selling. A family office that holds $160 million in real estate has $160 million that cannot move. Traditional exits take 6 to 18 months. Refinancing means bank dependency and liens. Tokenization creates a middle path: sell a fraction of the asset to investors, receive capital, and keep the majority ownership. The token represents a share in the SPV that holds the property. The property stays under your control.

Succession and estate planning. Passing real estate across generations is complex. Valuations are disputed. Ownership transfers require notaries, courts, and tax optimization that takes years. Tokens are divisible, transferable, and programmable. A parent can allocate exactly 12.5% of a hotel to each of four children through token transfers, with smart contracts that define voting rights, income distribution, and transfer restrictions. The legal structure stays clean. The cap table updates in real time.

Global diversification without global complexity. A family office in Singapore that wants exposure to European logistics or American hospitality currently needs local legal counsel, local bank accounts, local tax filings, and local property management relationships in each market. Tokenization does not eliminate all of this, but it reduces the friction. A tokenized logistics portfolio in Portugal can accept investors from Singapore through a compliant digital security offering, with KYC/AML handled on-chain and distributions paid in USDC.

Why 2026 is different from 2022

Family offices have been hearing about tokenization since 2018. Most waited. The infrastructure was immature, the regulatory picture was unclear, and the deals were too small to matter for portfolios of $200 million and above.

That has changed. Three shifts make 2026 the year family offices move from watching to acting.

Regulatory clarity arrived. The US passed the GENIUS Act in July 2025, creating the first federal framework for stablecoins. Europe's MiCA regulation is fully live. The UAE, Singapore, and Saudi Arabia all have working licensing frameworks. The question is no longer "is this legal?" It is "which framework fits my deal?"

Institutional credibility is established. BlackRock launched its BUIDL tokenized money market fund through Securitize. The fund grew from $400 million to $2.9 billion in 2025. Apollo, Hamilton Lane, KKR, and VanEck all have tokenized products. When BlackRock puts its name on a tokenized fund, the conversation inside family offices changes.

The investor demand data is clear. An EY survey found that 80% of high-net-worth investors and 67% of institutional investors were already investing or planning to invest in tokenized assets. By 2026, institutional investors expect to allocate 5.6% and HNW individuals 8.6% of their portfolios to tokenized assets. Real estate ranked as the second most attractive tokenized asset class for both groups.

Family offices that waited for proof now have it. The infrastructure works, the regulations exist, and the capital wants in.

How a family office tokenization deal works in practice

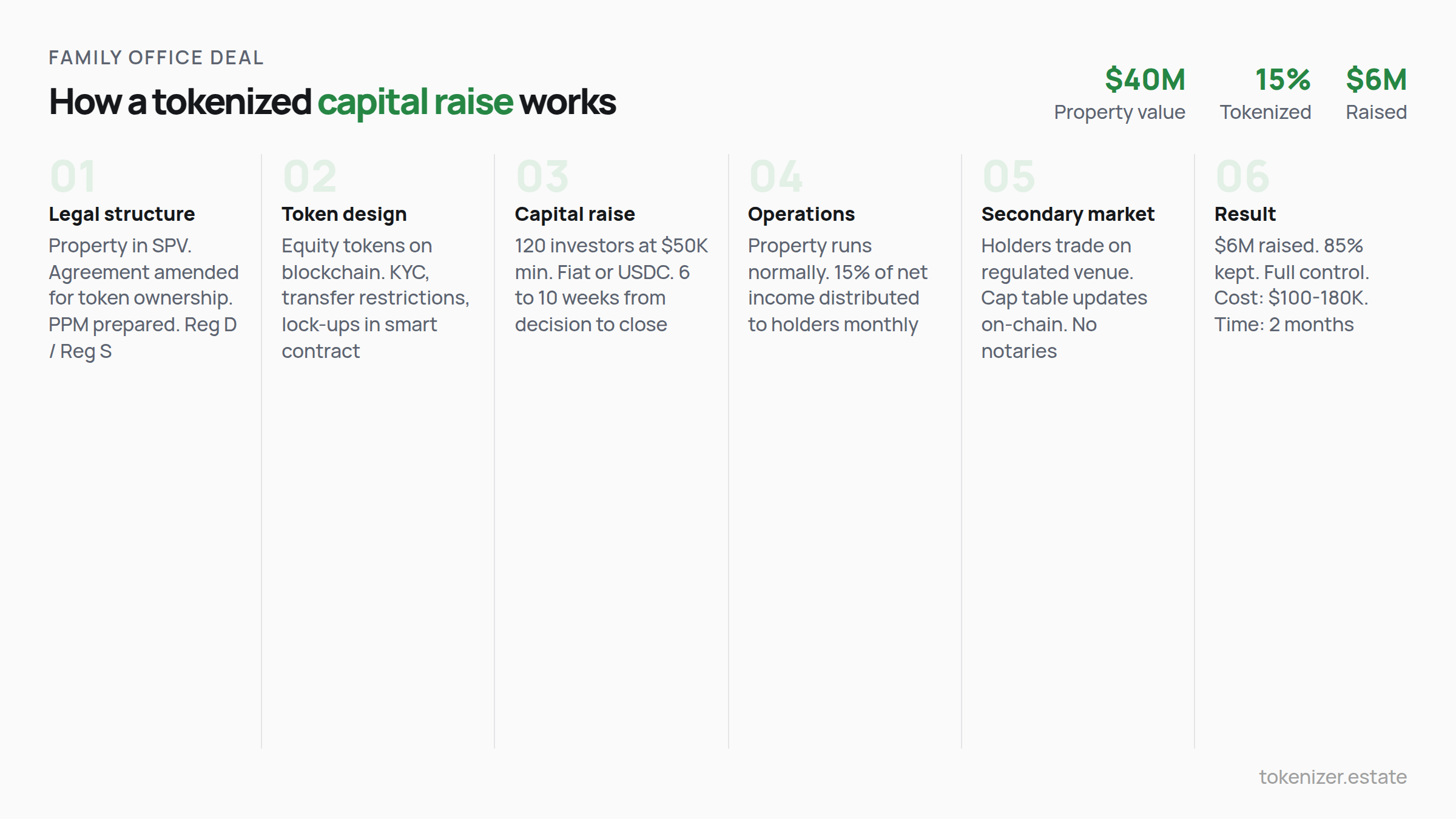

Here is the step-by-step process, using the Zurich example from the intro. The family office wants to tokenize 15% of a logistics park in Lisbon valued at $40 million.

Legal structure. The property already sits inside a Portuguese SPV (Sociedade Unipessoal Lda). The SPV's operating agreement is amended to allow token-based ownership. A Private Placement Memorandum is prepared. The offering is structured as a Reg S deal for non-US investors and a Reg D deal for US accredited investors, if needed.

Token design. The tokens represent equity interests in the SPV. They are created on a blockchain (Ethereum, Polygon, Hedera, or Stellar, depending on the platform and compliance needs). Smart contracts encode transfer restrictions: only KYC-verified investors can hold or trade the tokens. Lock-up periods are enforced automatically.

Capital raise. The family office raises $6 million by selling 15% of the SPV to 120 investors. Minimum investment: $50,000 per investor. Payments are accepted in fiat (wire transfer) or stablecoin (USDC). The process takes 6 to 10 weeks from decision to final investor.

Ongoing operations. The logistics park continues to operate normally. Tenants pay rent. The property manager manages. The smart contract distributes 15% of net rental income to token holders automatically, monthly. The family office receives 85%.

Secondary liquidity. If a token holder wants to exit, they sell on a regulated marketplace or platform. The transfer is verified on-chain: both buyer and seller must be KYC-compliant. The cap table updates instantly. No lawyers, no notaries, no three-month closing.

The family's position: they raised $6 million, deployed it into a new opportunity, kept 85% of the logistics park, and now have 120 investors who are aligned with the asset's success. Total cost: roughly $100,000 to $180,000 in legal, smart contract, and platform fees. Time: two months.

For a deeper look at how the legal structure, issuance platforms, custody, and secondary markets connect, the market map on the Tokenizer blog covers the full ecosystem.

Beyond real estate: what else family offices are tokenizing

Real estate is the entry point, but family offices rarely hold only property. The same tokenization structure works for other assets in the portfolio.

Hospitality. A family office that owns hotels can tokenize individual properties or an entire hospitality fund. The St. Regis Aspen raised $18 million through tokenization. RedSwan listed the Carmen Hotel in Playa del Carmen. Token holders receive a share of hotel revenue. The family keeps the management contract and the brand.

Industrial and logistics assets. Factories, warehouses, production equipment with long-term contracts. The cash flow is predictable, the depreciation is known, and the capital is locked. A family office with a portfolio of four factories can tokenize 20% of each and raise growth capital without touching the core operations.

Yachts, aircraft, and luxury assets. A $50 million superyacht that generates charter revenue 40 days a year and costs $5 million annually to maintain is a perfect tokenization candidate. The owner sells 30% to fractional investors who earn from the charter pool. The owner keeps the yacht, keeps using it, and unlocked $15 million. The same model works for private aircraft and luxury marina berths.

Private credit positions. Family offices increasingly allocate to private credit. Tokenizing a portfolio of real estate loans creates a tradable, transparent instrument that other family offices or institutional investors can buy into. Kin Capital launched a $100 million tokenized real estate debt fund through Chintai in 2025.

For the full picture of tokenization across non-real-estate asset classes, our guide to tokenization beyond real estate covers yachts, factories, energy, and marinas.

The governance question: control, transparency, and trust

Family offices care about control more than almost anything. This is the single biggest concern when tokenization comes up: "If I sell 15% of my building to 120 people, do I lose control?"

The short answer: no. The smart contract defines exactly what token holders can and cannot do. In most structures, token holders receive economic rights (income and appreciation) but limited or no governance rights. The family office retains management authority, operating decisions, and the ability to sell the property.

Voting rights, if included, are programmed into the contract. You can give token holders a vote on major decisions (selling the building, taking on new debt above a threshold) while keeping daily operations entirely in the family's hands.

Transparency actually benefits the family office. On-chain records show exactly how income is distributed, when transfers happen, and who holds what. This eliminates the "black box" problem that plagues traditional real estate partnerships. When disputes arise, the blockchain provides an immutable audit trail.

For succession, this is especially powerful. A patriarch who distributes tokens across family members can see the full cap table at any time. No hidden transfers. No disputed valuations. No surprises when the estate is settled.

What to watch out for

Tokenization is a tool. Like any tool, it can be used well or poorly. Here are the real risks for family offices.

Regulatory mismatch. A tokenized deal structured under US Reg D cannot accept non-accredited US investors. A deal structured under MiFID II has different rules. Getting the jurisdiction wrong creates legal exposure that no smart contract can fix. Legal advice comes first, always.

Thin secondary markets. Your investors can sell their tokens, but will there be a buyer at the price they want? Secondary market volumes for tokenized real estate are growing but still thin. Do not promise investors "stock-market liquidity." Promise compliance, transparency, and a path to liquidity.

Operational overhead. 120 investors need reporting. They need tax documents. They need a dashboard. They need responses to questions. The smart contract handles the financial distribution, but investor relations are still a human job. Budget for it.

Key management risk. The wallet that controls the admin functions of the smart contract must be secured. Multi-signature wallets (requiring 3 of 5 authorized parties) are the standard. Losing the admin key is an operational emergency.

Family dynamics. Tokenizing a family asset makes ownership transparent and divisible. That is usually a benefit, but it can surface disagreements that were previously hidden. One sibling wants to sell tokens, another wants to hold. One branch wants income distribution, another wants reinvestment. The smart contract can encode the rules, but the family must agree on the rules first.

Stay current with tokenization developments and regulatory updates at Tokenizer.Estate News.

The decision framework

If you run a family office, here is how to evaluate whether tokenization fits your portfolio.

Start with one asset. Do not tokenize the whole portfolio. Pick one property with strong cash flow, clean legal structure, and a clear investor story. A stabilized logistics park or a well-occupied office building. Not a development project. Not a distressed asset.

Tokenize a minority share. 10% to 25% is the range. Enough to raise meaningful capital. Small enough to keep full control and test the process without high-stakes pressure.

Choose the right platform. You need legal structuring, smart contract development, KYC/AML compliance, and investor management in one place. Assembling five vendors for your first deal creates unnecessary complexity.

Set expectations. The first deal takes 6 to 10 weeks and costs $100,000 to $200,000. The second deal takes less time and costs less. The infrastructure is reusable.

Think in decades. Tokenization is not a one-time capital raise. It is a permanent shift in how your portfolio is structured. Once an asset is tokenized, the cap table lives on-chain forever. The transparency, divisibility, and global accessibility remain. This is infrastructure, not a transaction.

The families who are evaluating this now will have their structures in place when the market scales. The families who wait will build under pressure.

This article is for informational purposes only and does not constitute legal, tax, or investment advice. Family office investment decisions involve complex tax, legal, and regulatory considerations. Always consult qualified professionals before structuring tokenized offerings or making allocation decisions.