Tokenization of Real Estate: SPV, Trust, and Fund Wrapper — Which Legal Structure Fits Which Asset Type

The legal wrapper chosen at day one shapes investor rights, tax, and exit paths. Here is how SPV, trust, and fund structures compare across five real estate asset types.

A $50M mixed-use portfolio in Lisbon — German family offices on the call sheet, Singaporean accredited investors signing NDAs, US qualified purchasers running diligence — failed to close in early 2026. The asset was sound. The sponsor had wrapped the tokenization of real estate inside a single Delaware LLC, which made the offering ineligible for distribution in two of the three target jurisdictions.

The smart contract was already deployed. The marketing site was live. The wrapper was wrong, and rewinding meant dissolving the LLC, refunding subscribers, and starting over with a Luxembourg RAIF. Eight months lost.

Why The Wrapper Decision Comes First In Real Estate Tokenization

The legal wrapper precedes the smart contract, the offering memorandum, and even the final asset selection. It defines what a token actually represents — a share of an entity, a beneficial interest in a trust, or a unit in a fund — and that definition determines investor eligibility before any code is written.

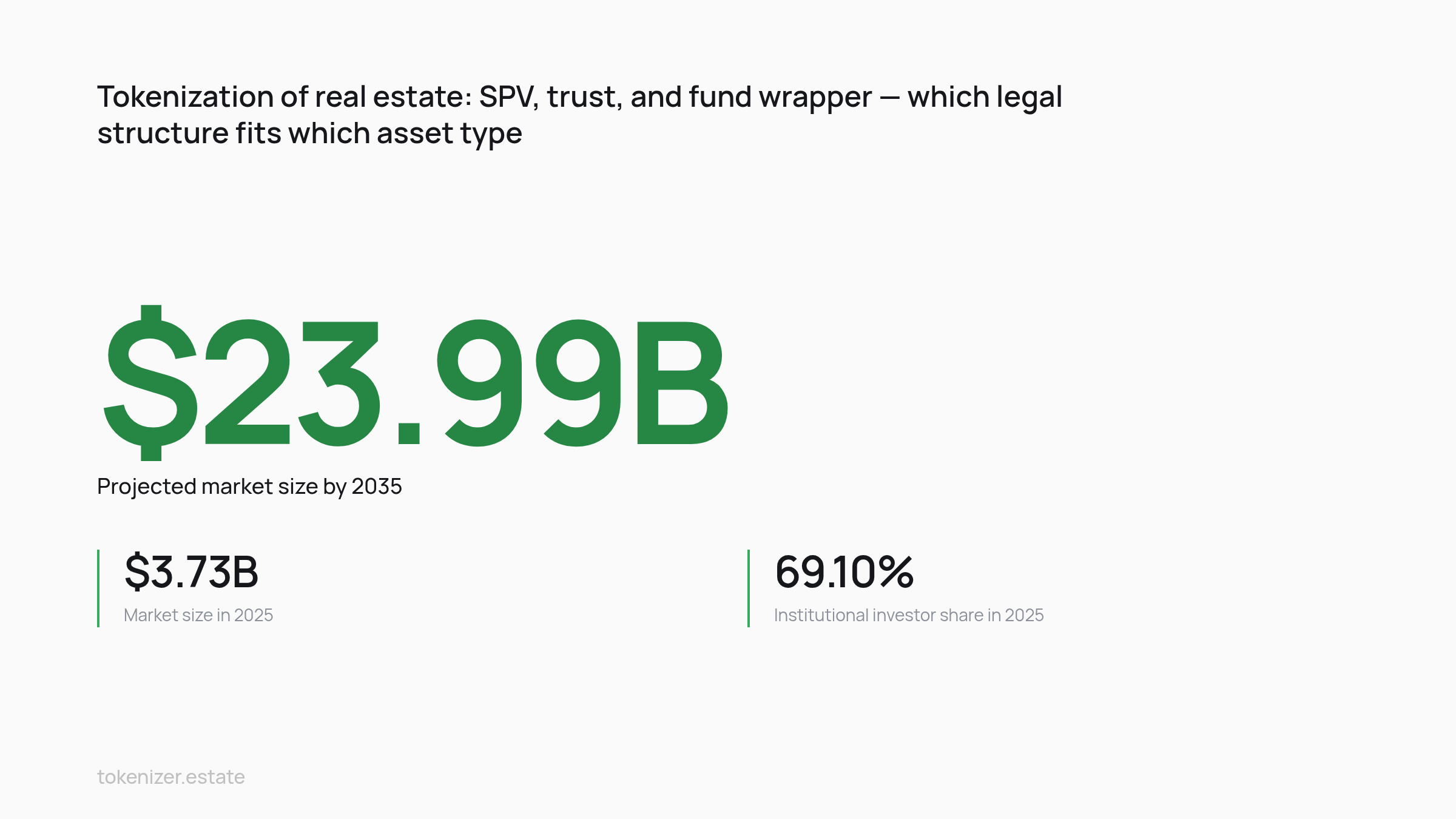

The market is large enough now that the cost of getting this wrong has multiplied. InsightAce Analytics values the real estate tokenization market at USD 3.73 Bn in 2025 and projects USD 23.99 Bn by 2035, a 21.0% CAGR over the 2026–2035 forecast window. The longer-horizon view from Deloitte estimates up to USD 4 trillion in tokenized real estate by 2035, a figure based on a top-down scenario that assumes institutional adoption tracks current pilot volumes.

At the structural level, Gofaizen & Sherle's 2026 legal guide defines real estate tokenization as the issuance of digital tokens representing defined economic or contractual rights linked to a property, most commonly through an SPV that owns the asset. The definition matters because the entity holding title is the wrapper, and the wrapper is what investors actually buy a claim against. The token is a settlement and distribution layer; the wrapper is the legal asset.

The remainder of this article maps three wrapper families — SPV, trust, and regulated fund — to five real estate asset types and the jurisdiction overlays that reshape each choice. For mechanics on how cash flows and exit rights flow through these structures, see ownership and exit mechanics.

SPV Real Estate Tokenization: Mechanics And Limits

The single-asset SPV is the default wrapper for commercial single-assets and standalone hospitality properties because the entity boundary matches the asset boundary. A Class A office building in Frankfurt or a 120-key resort in Phuket sits in one company; the tokens represent shares (equity) or notes (debt) issued by that company. Title, financing, insurance, operating contracts — all resolve to one balance sheet.

The mechanics work cleanly when the asset throws off identifiable cash flows. Net rent collected at the SPV level flows to token holders on a defined schedule, usually quarterly. Capital events — refinance, sale — distribute through the same waterfall. The audit trail is straightforward because there is one entity, one set of books, one bank account.

The structural limit is portfolio scale. A Madrid sponsor with 14 multifamily buildings cannot reasonably stand up 14 SPVs and 14 token issuances; the unit economics collapse under repeated legal fees, separate banking, and parallel investor reporting. The same sponsor cannot pool all 14 buildings into a single SPV either, because that turns the wrapper into an unregulated collective investment scheme in most EU jurisdictions — triggering AIFMD authorization that the SPV format was meant to avoid.

Banking onboarding is where the model stalls in practice. Gofaizen & Sherle reports in its 2026 real estate tokenization legal guide that project timelines run 4–8 months end-to-end, with banking onboarding the main bottleneck — the SPV needs an operating account, a subscription escrow, and often a custody arrangement, and each bank runs its own crypto-adjacent risk review. Legal Nodes notes that the SPV jurisdiction choice (BVI, Cayman, Delaware, Liechtenstein) shifts which banking corridors open and which close — BVI business companies in particular have faced narrower banking access following the 2023–2024 FATF grey-listing review and subsequent tightening by correspondent banks, a point flagged in practitioner commentary on SPV market context.

The operational implication is direct: for a single asset above roughly USD 10M and below USD 100M, with one clear cash-flow stream and one tax residency, the SPV is the right wrapper. Above that range, or with multiple assets, the SPV stops scaling. For the portfolio case the answer moves to a trust or a fund.

Trust Structures: Fit For Residential And Income-Generating Land

Common-law trust arrangements suit residential portfolios and income-producing land because they separate legal title from beneficial ownership cleanly, without requiring each underlying parcel to sit in its own corporate entity. A trustee holds title to a basket of suburban rental units or a portfolio of agricultural land plots; trust units represent the beneficial interest; tokens are a digital register of those units. The trust is the legal layer, the token is the transfer layer.

This is the securities-wrapper logic. Chainlink defines a securities wrapper as a digital token representing a legal claim to an underlying traditional financial asset — a stock, bond, or ETF — held by a qualified custodian. The same architecture applies to real estate trust units: the underlying interest sits with the trustee, and the token is a derivative or depository receipt that represents a claim on an asset stored elsewhere. The token holder's enforceable right is against the trustee, governed by the trust deed.

The fit with residential portfolios is structural. A trustee can take title to 200 single-family rentals across three US states under one declaration of trust without standing up 200 SPVs, and beneficial interests can be subdivided into transferable units that map one-to-one to tokens. The same logic applies to income-generating land — leased farmland, ground-lease plots, solar-site leaseholds — where the asset is passive and the cash flow is a stream of contractual payments. The trust contains the assets; the token transfers the units.

Trust wrappers also carry tax-transparency advantages in several jurisdictions. A US Delaware statutory trust treated as a grantor trust passes rental income through to token holders without entity-level tax. A Jersey unit trust elected as transparent does the same for European institutional investors. The wrapper choice here is partly a tax-residency choice for the underlying income stream.

The macro context is that trust-wrapped tokens now move inside a market with real depth. Buzko Krasnov's 2026 legal guide to RWA tokenization notes the global on-chain real-world asset market has quintupled from around $5 billion in 2022 to about $24 billion by mid-2025 — the secondary aggregation tracks underlying figures reported by industry trackers. The depth matters because trust-wrapped property tokens compete for the same institutional allocation as tokenized treasuries and private credit; the wrapper has to satisfy the same custody and transferability standards. For the underlying mechanics, see how smart contracts handle the unit-to-token mapping.

Fund Wrapper Tokenization For Multi-Asset And Mixed-Use Portfolios

The regulated fund wrapper is the only structure that handles diversified portfolios and mixed-use developments at institutional scale, because it absorbs the legal, regulatory, and operational complexity that breaks SPVs and stretches trusts. A Luxembourg Reserved Alternative Investment Fund (RAIF), a Cayman Segregated Portfolio Company (SPC), or a Liechtenstein Alternative Investment Fund (AIF) can hold a basket of assets across jurisdictions, segregate them by sub-portfolio, and issue tokenized units that qualify as fund interests under the relevant securities regime.

The market data explains why this matters now. Mordor Intelligence reports that institutional investors held 69.10% of the asset tokenization market share in 2025, while the retail segment is advancing at 50.20% CAGR through 2031. Institutional capital does not buy SPV tokens at portfolio scale; it buys fund interests, because that is the wrapper its mandates and risk frameworks already understand.

Why The Fund Wrapper Suits Mixed-Use Developments

A mixed-use project — ground-floor retail, mid-floor offices, upper-floor residential, basement parking — has four distinct income streams, four distinct risk profiles, and often four distinct tenant regimes. Wrapping the project in a single SPV obscures the segmentation. A fund wrapper with sub-portfolios (segregated cells in a Cayman SPC, compartments in a Luxembourg RAIF) lets each income stream sit in its own ring-fenced pocket while token holders subscribe to the fund as a whole or to specific compartments. The operative classification is the fund's regulatory status under the home regulator, which then governs marketing, custody, and reporting downstream.

Asset-class concentration reinforces the case. Mordor Intelligence puts real estate at 30.12% of the asset tokenization market in 2025, with commodities projected to expand at 48.35% CAGR through 2031 — a forecast that draws on a top-down model and should be read with that methodology caveat. The point is that real estate remains the dominant tokenized asset class, and within it the diversified vehicle is where the institutional flow concentrates.

Operating Cost And Distribution Reach

Fund wrappers carry real overhead. Practitioner estimates from Luxembourg and Liechtenstein fund administrators put annual operating cost — AIFM fee, depositary, audit, regulatory reporting — at roughly EUR 250–350k for a small RAIF or AIF; the figure is a practitioner range, not a regulatory disclosure, and varies by AIFM, asset complexity, and investor count. Below a portfolio of about USD 30M, the math does not work. Above that threshold, the wrapper unlocks EU-wide distribution under AIFMD passporting and parallel access to non-EU institutional channels, which the SPV cannot match.

The institutional infrastructure is consolidating quickly. Recent 2024–2025 entrants include Coinbase seeking SEC approval to trade tokenized stocks 24/7 and Backed Finance launching xStocks tokenized equities via Kraken and on Solana — adjacent moves that signal the rails fund-wrapped real estate tokens will trade on. For a deeper read on when the fund route beats the single-asset route, see the single-asset versus diversified fund framework.

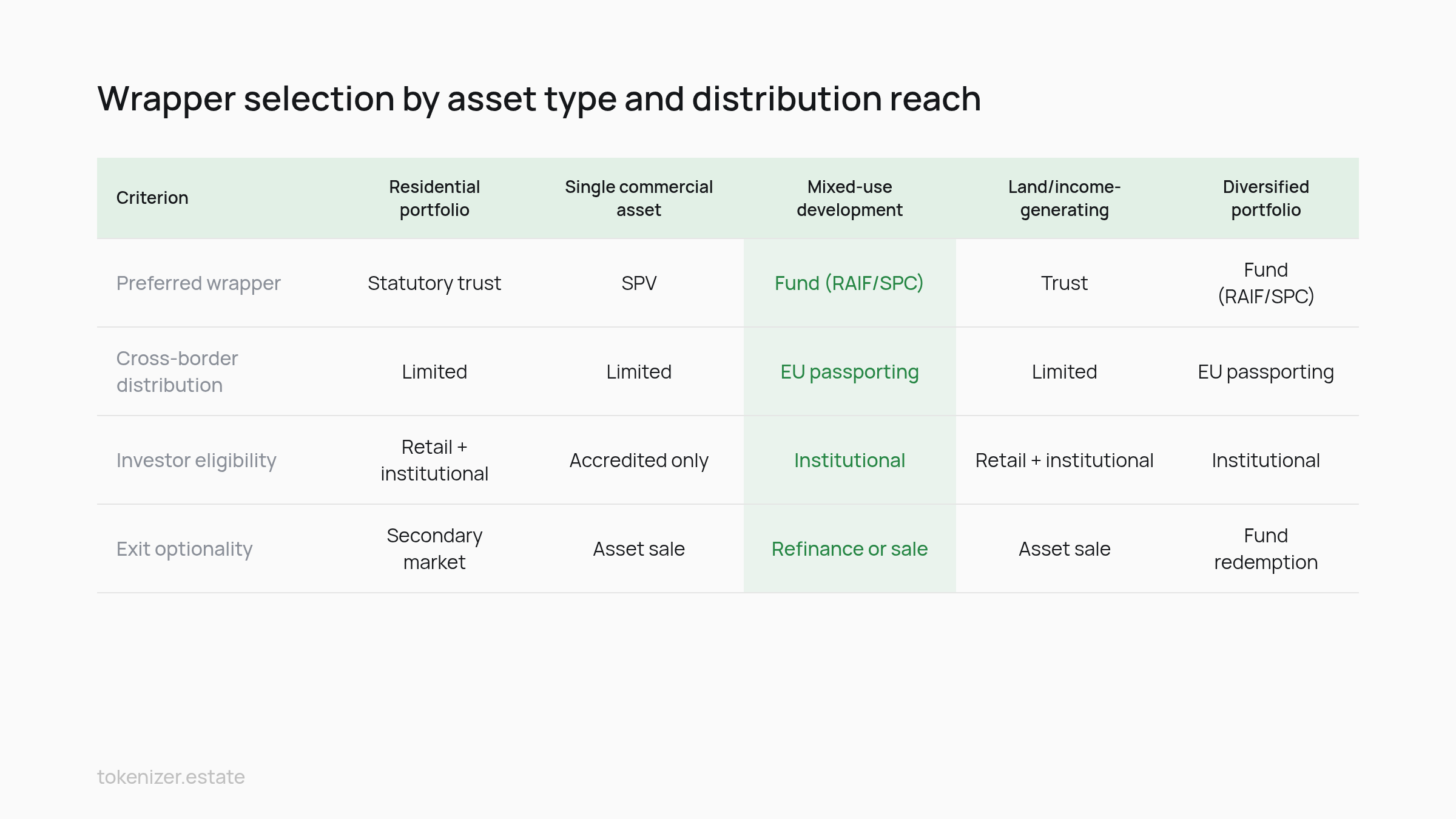

Decision Matrix: Real Estate Token Legal Structure By Asset Type

The matrix below maps five asset types against the three wrapper families on the four dimensions that determine viability: investor rights, cross-border distribution, tax treatment, and exit optionality. The asset tokenization market is large enough that the matrix governs real capital allocation — Mordor Intelligence values it at USD 2.08 trillion in 2025, growing from USD 3.01 trillion in 2026 to USD 18.74 trillion by 2031 at a 44.25% CAGR, with the forecast built on adoption modeling that compounds enterprise pilots into base-case volumes.

Wrapper-To-Asset Mapping

Asset Type | Preferred Wrapper | Investor Rights | Cross-Border Distribution | Exit Path |

|---|---|---|---|---|

Residential portfolio (multifamily, SFR) | Statutory trust or unit trust | Beneficial interest in trust units | Reg D + Reg S; private placement in EU | Trustee-mediated sale, secondary market |

Commercial single-asset (office, logistics) | Single-asset SPV | Equity or debt in the SPV | Direct subscription; jurisdiction-bound | SPV sale, refinance, token buyback |

Mixed-use development | Fund wrapper with compartments (RAIF, SPC) | Fund units, optionally per compartment | AIFMD passport in EU; private placement elsewhere | Compartment liquidation, fund-level exit |

Income-generating land (farm, leased plots) | Unit trust or grantor trust | Pass-through beneficial interest | Trust-deed governed; transparent for tax | Trust termination, unit redemption |

Hospitality (single hotel or resort) | Single-asset SPV; fund wrapper if portfolio | SPV equity with operating-agreement rights | Reg D + Reg S; offshore feeder common | Sale of SPV, operator exit, refinance |

How Two Cases Resolve

Consider a EUR 65M mixed-use development in Porto with ground-floor retail, 40 serviced apartments, and a co-working floor. A single-asset SPV would force the sponsor to commingle three income streams in one balance sheet, blocking institutional subscribers that need ring-fencing. A Luxembourg RAIF with three compartments separates the streams and opens EU passporting. The SPV would be undersized for the structure required.

Now take a USD 12M Class B logistics asset in Memphis with one triple-net lease to an investment-grade tenant. A Delaware SPV issuing tokenized equity under Reg D and Reg S handles distribution to US accredited investors and offshore subscribers without further wrapping. The fund wrapper would be overkill. The cash flow is single-stream, the tax position is clean, the exit is a sale of the SPV.

Why Permissioned Rails Still Dominate

Wrapper choice interacts with rail choice. Mordor Intelligence reports that permissioned blockchains captured 50.60% of the asset tokenization market size in 2025, even as permissionless networks are forecast to grow at 51.60% CAGR. For real estate, the permissioned share reflects institutional preference for KYC-gated transfer rules baked into the token, which fund wrappers and trust structures require for compliance with AIFMD and securities-law transfer restrictions. Shamla Tech notes that US-domiciled tokenized real estate offerings under Reg D rely on transfer-agent integration that permissioned environments support natively; practitioner mapping of asset to wrapper to chain is the standard pre-issuance workflow.

Jurisdiction Overlays: US FinCEN, EU MiCA, And Offshore Hubs

Jurisdiction overlays reshape the wrapper choice after the asset and investor base are set. The US residential SPV calculus shifted sharply in early 2026, the EU now layers MiCA on top of AIFMD for token issuance, and offshore hubs compete on speed and cost rather than on regulatory depth.

On the US side, FinCEN confirms that on March 19, 2026, the U.S. District Court for the Eastern District of Texas issued an order vacating the Residential Real Estate Rule. Reporting persons are not currently required to file Real Estate Reports with FinCEN and are not subject to liability if they fail to do so while the court's order remains in force. The practical effect for tokenized residential SPVs is that the compliance overhead the rule would have imposed on non-financed cash purchases through legal entities is suspended; sponsors structuring trust-wrapped residential portfolios face a lower friction profile than they did six months ago. Greenberg Traurig's February 2026 client alert tracked the compliance-deadline backdrop that preceded the vacatur.

The US market matters disproportionately to wrapper selection because of its concentration. Prophecy Market Insights values the US Real Estate Tokenization Market at USD 0.96 Billion in 2024 and projects USD 6.6 Billion by 2034 at a 2.90% CAGR — the forecast is conservative relative to global projections and reflects the regulatory drag that the US has historically applied. InsightAce Analytics confirms that the North American region leads the real estate tokenization market, which means US wrapper rules effectively set the de facto standard for cross-border offerings targeting US qualified purchasers.

On the EU side, MiCA applies to asset-referenced and e-money tokens but excludes financial instruments, which means tokenized fund units and tokenized SPV equity remain governed by MiFID II, AIFMD, and the Prospectus Regulation — not MiCA. The wrapper choice still has to answer to the existing securities framework; MiCA matters mostly for the payment-token side of the platform, not for the property-token itself. For the EU-specific framework, see the MiCA framework analysis.

Offshore hubs — BVI, Cayman, DIFC, ADGM — compete on time-to-launch and operating cost. Their use is rational for the SPV-and-feeder model that pools international subscribers into a US or EU master vehicle. The risk is correspondent-banking access, which has narrowed for some BVI business companies and tightened for Cayman SPCs without a substantive presence. The wrapper that looks cheapest on paper can become the wrapper that cannot open a bank account, which returns the analysis to the same point as Section 2.

The wrapper decision sits at the intersection of asset type, investor domicile, and regulatory overlay, and changes to any one variable can reset the optimal structure. The vacatur of the FinCEN rule is one such reset; the AIFMD passporting regime is another standing variable; the MiCA delineation between financial instruments and crypto-assets is a third. Sponsors who treat the wrapper as fixed at the start of a project will find the project's distribution reach fixed at the same moment.

The wrapper decision is the architectural choice that locks in investor eligibility, cross-border distribution, tax treatment, and exit optionality before a single token is minted. Sponsors who select the wrapper after the smart contract specification has been written are sequencing the project backwards, and the cost of correction — refunding subscribers, dissolving entities, re-papering distribution agreements — exceeds the cost of the original legal work by an order of magnitude.

Fund managers and developers mapping a specific portfolio to a wrapper can review the jurisdiction configuration options and request a structure-mapping session at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo