Tokenized Real Estate: How the Legal, Technical, and Distribution Layers Work Together

A practical guide for fund managers and developers on how the three infrastructure layers of tokenized real estate constrain each other, with walkthroughs of a $20M deal and a $100M fund.

A fund manager closes a $20M single-asset tokenized real estate deal in six months. A competitor with a comparable property takes fourteen months and loses two anchor LPs to onboarding friction. The asset quality was nearly identical. The difference sat in how three infrastructure layers — legal wrapper, smart contract logic, and distribution rails — were sequenced and constrained against each other.

Most coverage of property tokenization treats it as a single product choice. For operators running real portfolios, that framing misleads. The decisions at each layer foreclose options at the next, and reversing a layer-one choice after a token is live can cost months and burn investor trust.

Why Tokenized Real Estate Demands Layered Thinking

The operator's problem starts with a market imbalance. JP Morgan Kinexys documented that private equity fund-raising supply ran three times higher than investor demand — the widest gap since the financial crisis. Real estate sponsors feel the same squeeze. Capital is available in theory; the friction of moving it into a fund vehicle keeps it parked.

The standard response has been to raise the minimum ticket. JP Morgan Kinexys notes that alternative asset managers often find it economically attractive to accept only large-ticket investments above $5 million per investor. That math works for sovereign wealth offices and large pensions. It locks out the family office and accredited individual layer that, in aggregate, controls more deployable capital than the institutions above them.

Tokenization is sometimes pitched as the fix. It is more accurate to say tokenization is three sequenced decisions that, taken together, can fix it. The legal wrapper determines what the token legally represents. The smart contract encodes which transfers are allowed. The distribution rails decide who can actually buy. Deloitte's analysis of tokenized real estate asset management treats these as connected, not parallel. The two scenarios at the end of this article — a $20M single asset and a $100M diversified fund — show why getting the order right matters more than the technology brand chosen at any single step.

Layer One: The Legal Wrapper and Jurisdiction Choice

The legal wrapper is the first decision and the hardest to reverse. It defines what the token actually represents — direct fractional ownership, an equity interest in a holding company, a debt instrument secured against the property, or a beneficiary right under a trust. Each form attracts a different regulatory class and a different investor pool.

For most real estate deals the practical wrapper is a Special Purpose Vehicle (SPV) that holds title to the property, with tokens representing equity or economic rights in that SPV. The SPV's jurisdiction then drives everything downstream: which regulator approves the offering, which banking partners will open accounts, and which secondary venues will list the token.

The Three-Way Trade-Off

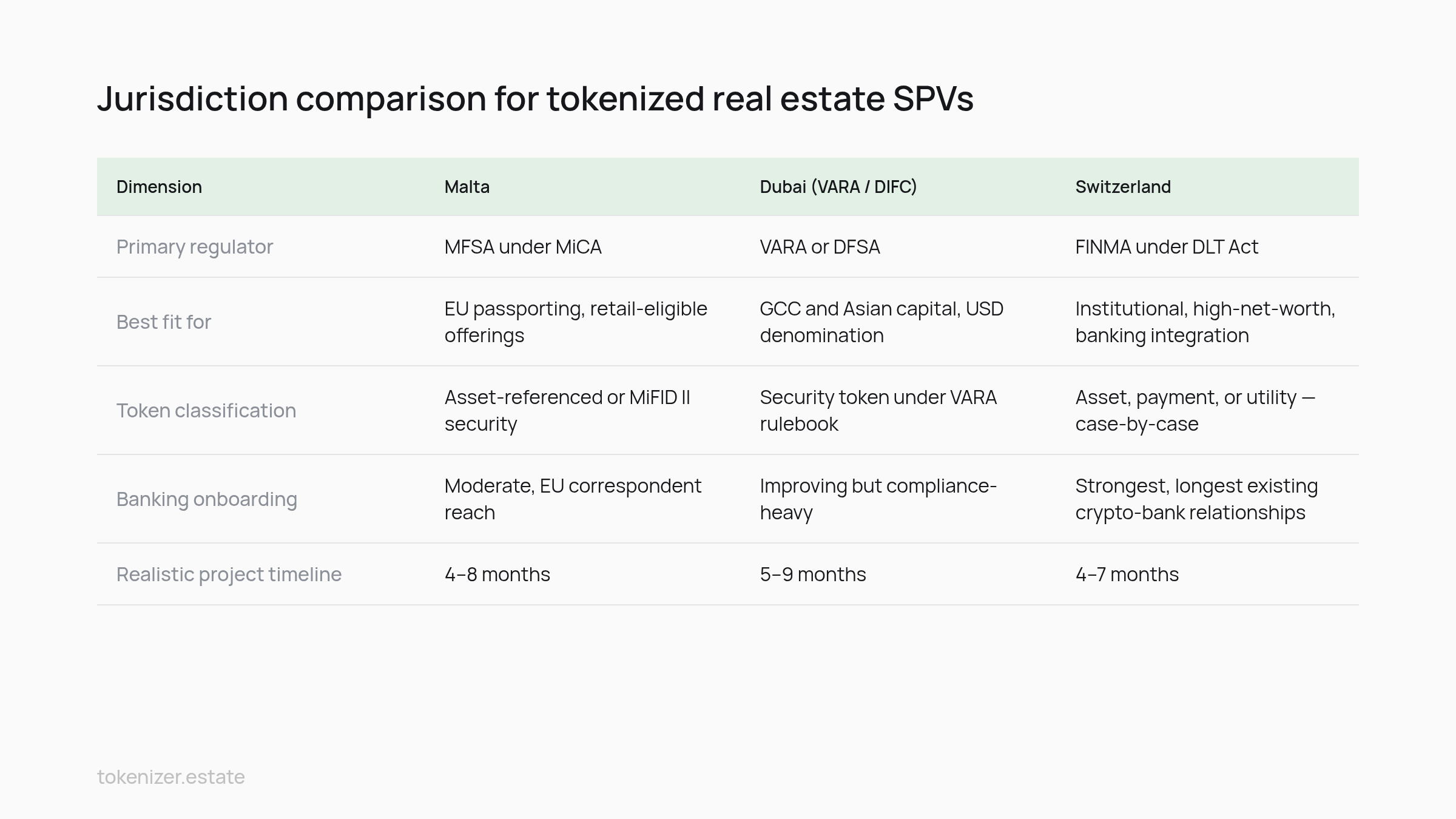

Operator-side guidance from Gofaizen & Sherle, Legalnodes, and EU-focused MiCA analyses converges on three jurisdictions for structure-dependent tokenization: Malta, Dubai, and Switzerland. The right answer depends on the investor base, not on which jurisdiction has the friendliest marketing.

Dimension | Malta | Dubai (VARA / DIFC) | Switzerland |

|---|---|---|---|

Primary regulator | MFSA under MiCA | VARA or DFSA | FINMA under DLT Act |

Best fit for | EU passporting, retail-eligible offerings | GCC and Asian capital, USD denomination | Institutional, high-net-worth, banking integration |

Token classification | Asset-referenced or MiFID II security | Security token under VARA rulebook | Asset, payment, or utility — case-by-case |

Banking onboarding | Moderate, EU correspondent reach | Improving but compliance-heavy | Strongest, longest existing crypto-bank relationships |

Realistic project timeline | 4–8 months | 5–9 months | 4–7 months |

Gofaizen & Sherle put practical project timelines at 4–8 months across the structures they advise on, with banking onboarding usually the binding bottleneck. That figure matters because it sets the floor for any operator promising a six-month close. The smart contract and the website can be ready in weeks. The bank account for the SPV — the one that has to receive subscription wires and pay distributions — runs on a different clock.

The MiCA Effect on EU Offerings

For any offering targeting EU retail or professional investors, the Markets in Crypto-Assets regulation (MiCA) reshapes the calculus. RWA.io's MiCA briefing clarifies that tokens qualifying as financial instruments under MiFID II remain outside MiCA and stay under existing securities law — which is where most real estate equity tokens land. Asset-referenced tokens and e-money tokens fall inside MiCA. The operative classification is therefore the first legal question, not an afterthought, because it determines whether the prospectus regime applies and whether MiCA's white paper requirements apply on top.

The structural implication: a Maltese SPV issuing equity tokens to EU investors lives under MiFID II and the Prospectus Regulation. A Dubai SPV selling the same economic exposure to GCC investors does not. Picking the jurisdiction effectively picks the rulebook the next two layers must obey. For deeper treatment of EU mechanics, see MiCA-regulated markets.

Layer Two: Smart Contract Logic and the ERC-3643 Standard

Once the legal wrapper is fixed, the smart contract has a defined job: enforce the wrapper's constraints on every transfer, automatically. A token that represents equity in a regulated SPV cannot trade like a fungible cryptocurrency. It has to check, before every transfer, whether the receiver is whitelisted, accredited where required, not on a sanctions list, and within any holding-period or jurisdictional limit set in the offering documents.

The protocol that has consolidated this logic is ERC-3643. According to ERC-3643's official documentation, the protocol is an open-source suite of smart contracts that enables the issuance, management, and transfer of permissioned tokens. The same documentation positions the addressable market at over 100 trillion dollars in global securities — a figure that signals the standard was designed for institutional issuance, not retail experiments.

What ERC-3643 actually does, in operator terms, is split the token into two layers. The token contract handles balances and transfers. A separate on-chain identity registry — built on the ONCHAINID standard — holds verified claims about each holder: KYC status, accreditation, country of residence, lock-up flags. A transfer only completes if the identity registry approves both sides. Chainalysis describes this as the on-chain enforcement of compliance rules that previously lived in transfer agent databases and Excel sheets.

The benefit for a real estate issuer is concrete. If the SPV is in Malta and the offering is restricted to EU professional investors plus a small accredited-US tranche under Regulation D, those rules live inside the contract. A US retail investor who somehow acquires the token in a peer-to-peer transfer cannot complete the trade. The contract rejects it. The compliance officer does not need to chase it down after the fact.

This is also where custom logic is still required. ERC-3643 handles transfer permissioning well. It does not handle distribution waterfalls, capital calls, or property-level events like a refinancing that triggers a partial redemption. Those need custom modules layered on top, usually as separate contracts that read from the token's holder registry. The Finextra coverage of institutional adoption emphasizes the same point: the standard is the floor, not the ceiling.

The binding limit on layer two is that smart contracts cannot validate facts they do not have. If the legal wrapper requires that no single holder exceed 9.9% of the SPV (a common cap to avoid disclosure thresholds), the contract enforces the cap on the token. If the same investor holds another economic interest off-chain, the contract cannot see it. Coordination with the transfer agent and the SPV's company secretary stays mandatory. For more on the technical layer specifically, see smart contracts for real estate.

Layer Three: Distribution Rails and Investor Onboarding

Distribution is the layer that decides whether tokenization actually expands the investor base or just relabels the existing one. JP Morgan Kinexys estimates that unlocking the distribution benefits of tokenization represents potentially $400 billion in additional annual revenue for the alternatives industry. That number assumes the rails actually function — onboarding, qualification, and settlement working end-to-end without the manual reconciliation that defines current private placements.

The KYC/AML Pipeline

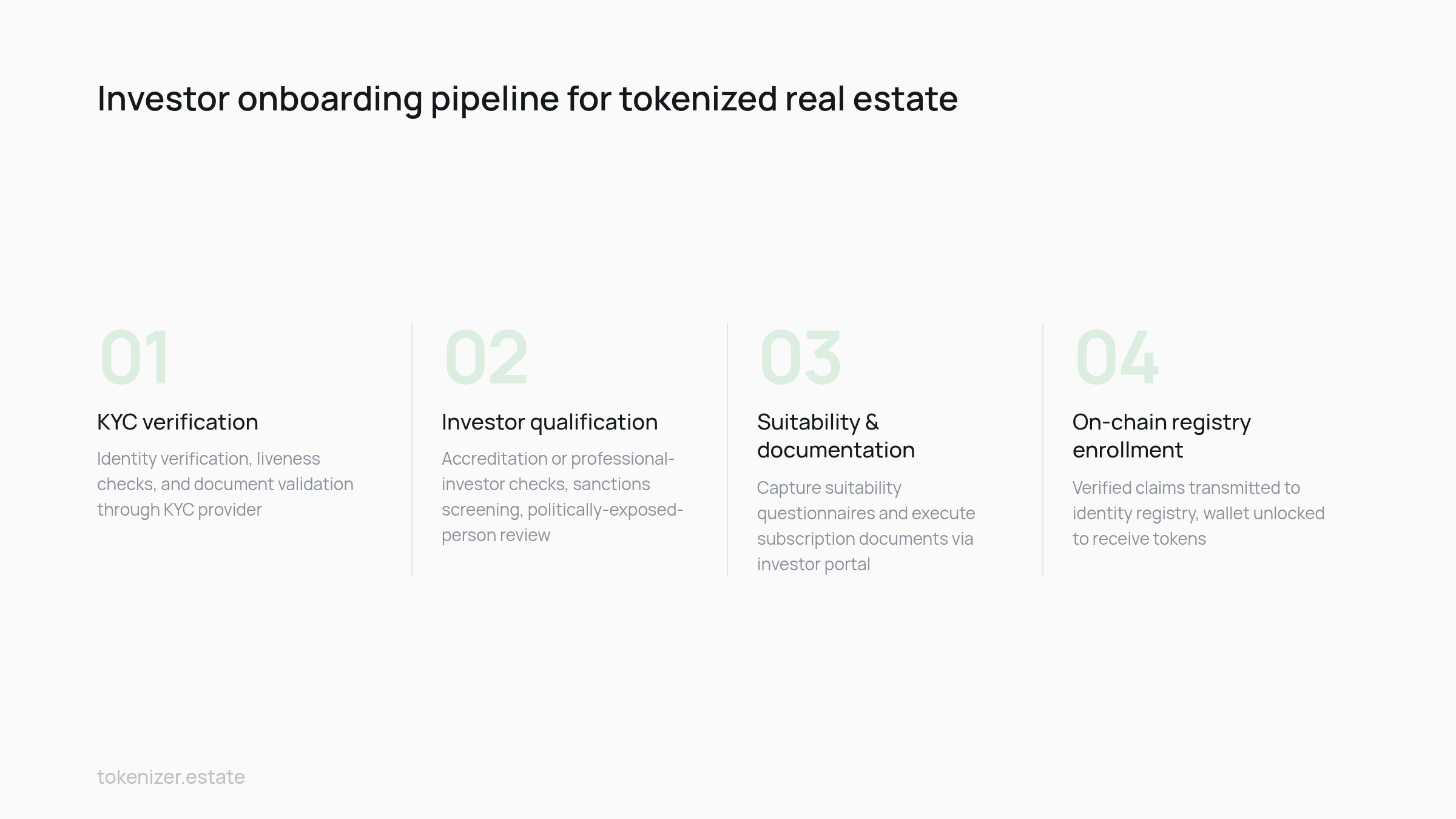

Onboarding is where most timelines die. Each investor has to pass identity verification, accreditation or professional-investor checks where applicable, sanctions and politically-exposed-person screening, and source-of-funds review for larger tickets. Quill Audits notes that fractional entry points as low as $25 open the market to retail investors — but only if the onboarding pipeline can process those investors at unit economics that survive the smaller ticket size.

In practice, the pipeline runs through three components: a KYC provider that handles document checks and liveness; an investor portal that captures suitability questionnaires and signs subscription documents; and the identity registry on-chain that receives the verified claim and unlocks the wallet to receive tokens. InvestaX describes this stack as the operational core of any fund tokenization workflow.

Banking, Settlement, and Secondary Venues

The bottleneck is not the technology stack. It is the bank account that has to receive subscription wires from twenty different jurisdictions and pay distributions back out. Banks underwrite SPV accounts on the strength of the underlying business, the directors, the AML procedures, and the source of funds. None of that moves faster because the equity is tokenized.

Secondary trading venues are the second-half question. A token can only trade where a venue is licensed to list it and where the issuer has signed a listing agreement. Most real estate tokens currently trade on a small number of regulated alternative trading systems or multilateral trading facilities, and most operate with low volume relative to the issuance size. The realistic posture for an issuer is that primary distribution drives the deal; secondary liquidity is a benefit that compounds over years. For practical onboarding mechanics, see KYC/AML for tokenized securities.

Scenario: A $20M Single-Asset Tokenized Real Estate Deal

Consider a sponsor with a stabilized $20M multifamily property in Lisbon. The goal: replace a single institutional LP with a broader pool of family offices and high-net-worth individuals across the EU and the Middle East, at a valuation premium of up to 20% above the comparable institutional bid.

Layer one decision: a Maltese SPV holds the property's holding company shares, with tokens representing equity in the SPV. Maltese law gives EU passporting under MiFID II for the security offering, and the SPV qualifies for double-taxation treaty benefits on Portuguese property income. This choice is effectively irreversible. Re-domiciling the SPV after issuance would require a holder vote, regulatory consent in both jurisdictions, and a token swap.

Layer two decision: an ERC-3643 token deployed on a permissioned chain, with the identity registry restricted to professional investors under MiFID II plus a Regulation S tranche for non-US investors elsewhere. Tokeny documents this configuration as standard for European-domiciled real estate equity tokens. This decision is partially reversible — the issuer can later expand to a Regulation D tranche, but adding US investors triggers a new disclosure package and a new transfer-agent relationship.

Layer three decision: distribution through a regulated placement agent plus direct subscription via the issuer's investor portal. The portal handles KYC, suitability, and subscription documents. The placement agent brings the family-office channel that the direct portal cannot reach. DigiShares and Innreg both describe this dual-channel pattern as the practical default for deals in the $10–30M band.

The market context for a deal this size: with over $18 billion in total value locked across real-world-asset protocols and projections from Quill Audits citing $4 trillion in tokenized real estate by 2035, a $20M deal is a routine issuance, not an experiment. The single-asset format also keeps the scope narrow — one property, one valuation report, one tax opinion — which is why six-month timelines are realistic when the layers are sequenced. For deeper treatment of the single-asset format, see the single-asset vs fund decision framework.

Scenario: A $100M Diversified Tokenized Real Estate Fund

A $100M diversified fund changes the math at every layer. The sponsor is now assembling six to twelve properties across two or three jurisdictions, targeting a broader cross-border investor pool, and committing to a multi-year hold with quarterly distributions and a possible follow-on raise.

Master-Feeder and Multi-Jurisdiction Structuring

The legal wrapper here is rarely a single SPV. The standard shape is a master fund — often Luxembourg, Cayman, or Dubai International Financial Centre (DIFC) — with feeder vehicles in each investor jurisdiction and property-level holding companies in each asset jurisdiction. CBIZ's analysis of tokenization in fund management treats this master-feeder pattern as the default for cross-border tokenized funds, because it preserves tax treaty access while concentrating fund accounting in one place.

The token is then issued at the master fund level, representing limited partnership or shareholder interests in the master. Property-level events flow up through the holding chain to the master, and distributions flow down through the token to the holders. The structure is more expensive to set up than a single SPV — typically $200–400K versus $50–80K in legal and structuring fees — but it scales without renegotiation when assets are added.

How Distribution Forces Earlier Legal Decisions

The diversified fund scenario inverts the layer order in one important way. Because the sponsor wants to raise from at least three regions simultaneously, the distribution decision has to be made first: which investor pools, which marketing rules, which secondary venue. Only then does the legal wrapper get designed to satisfy all three regimes at once.

This is where Deloitte's projection that the global market for commercial real estate tokenization is expected to expand dramatically by 2035 becomes operationally relevant. The fund-format deals are what drive the projected expansion, because they scale better than single-asset deals once the master vehicle is built. Gofaizen & Sherle's estimate aligns with Deloitte's outlook under base-case adoption assumptions.

Layer two for a fund of this scale typically uses ERC-3643 with extended compliance modules: lock-up enforcement during the investment period, redemption gates tied to fund liquidity, and a transfer module that recognizes feeder-level holders distinctly from direct master-level holders. Polymesh's infrastructure documentation and InvestaX's fund tokenization guide both treat these extensions as fund-tier requirements rather than asset-tier ones. For the broader portfolio operational view, see tokenizing a real estate portfolio.

Operators who treat tokenization as three interlocking infrastructure decisions — not as a single technology purchase — keep control of timeline, compliance exposure, and investor reach. Those who pick the smart contract platform first, the jurisdiction second, and worry about distribution last inherit constraints they cannot later unwind without a full restructuring. The sequencing is the work.

Fund managers and developers mapping the three layers against an actual portfolio can review jurisdiction, smart contract, and distribution configurations at Tokenizer.Estate.

Share this post

Build your own tokenization business with Tokenizer.Estate

Tokenizer.Estate provides a full end-to-end solution — from legal setup to blockchain infrastructure — to help you launch your project with confidence

Book a Free Demo